“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

For a full dive into the latest intelligence around pricing, quality, and demand trends, check our comprehensive State of Carbon Credits report.

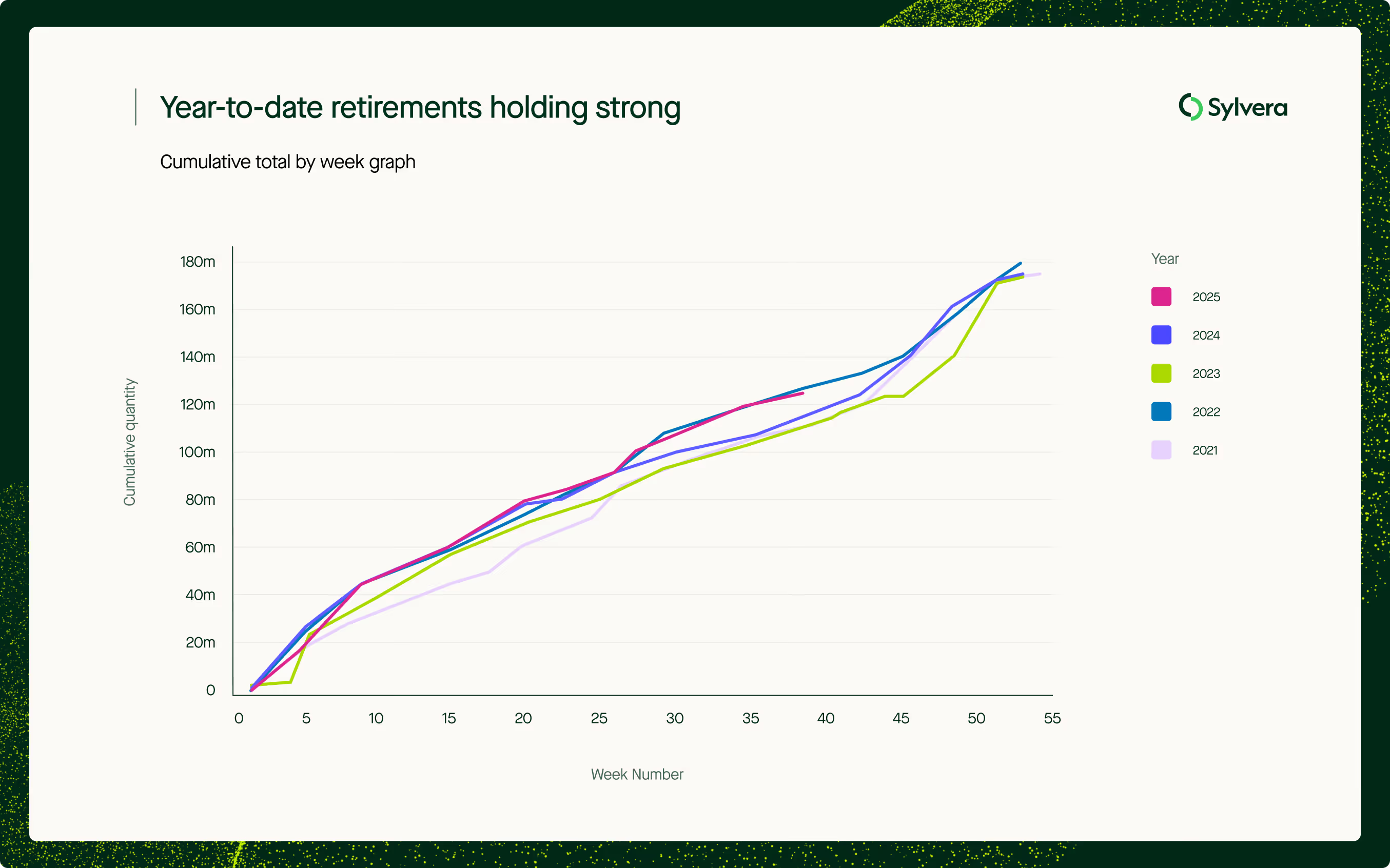

High-quality carbon credit prices hit new highs as retirements hold firm

The voluntary carbon market remained stable in Q3 2025, with retirements holding steady and issuances showing a slight decline compared to the previous quarter. Alongside this, our enhanced pricing and buyer insights point to a growing focus on quality and evolving patterns in corporate demand.

Retirements, the process of using a credit to offset emissions and making it permanently unavailable for trading, reached 33.54 million in Q3. While this represents a drop from the record 40.45 million credits retired in Q2, it closely matches Q3 2024 levels of 31.49 million, with 2025 total retirement volume nearing a record high. Year-to-date retirements in 2025 are holding strong at 128.15 million credits, up from 120.61 million at end of Q3 2024 and tracking marginally behind record retirement year 2022, which showed 132.42 million at this point.

On the supply side, issuances – the creation of new credits – totalled 70.4 million for the quarter, down from 76.9 million in Q2 and 68.8 million for the same period last year.

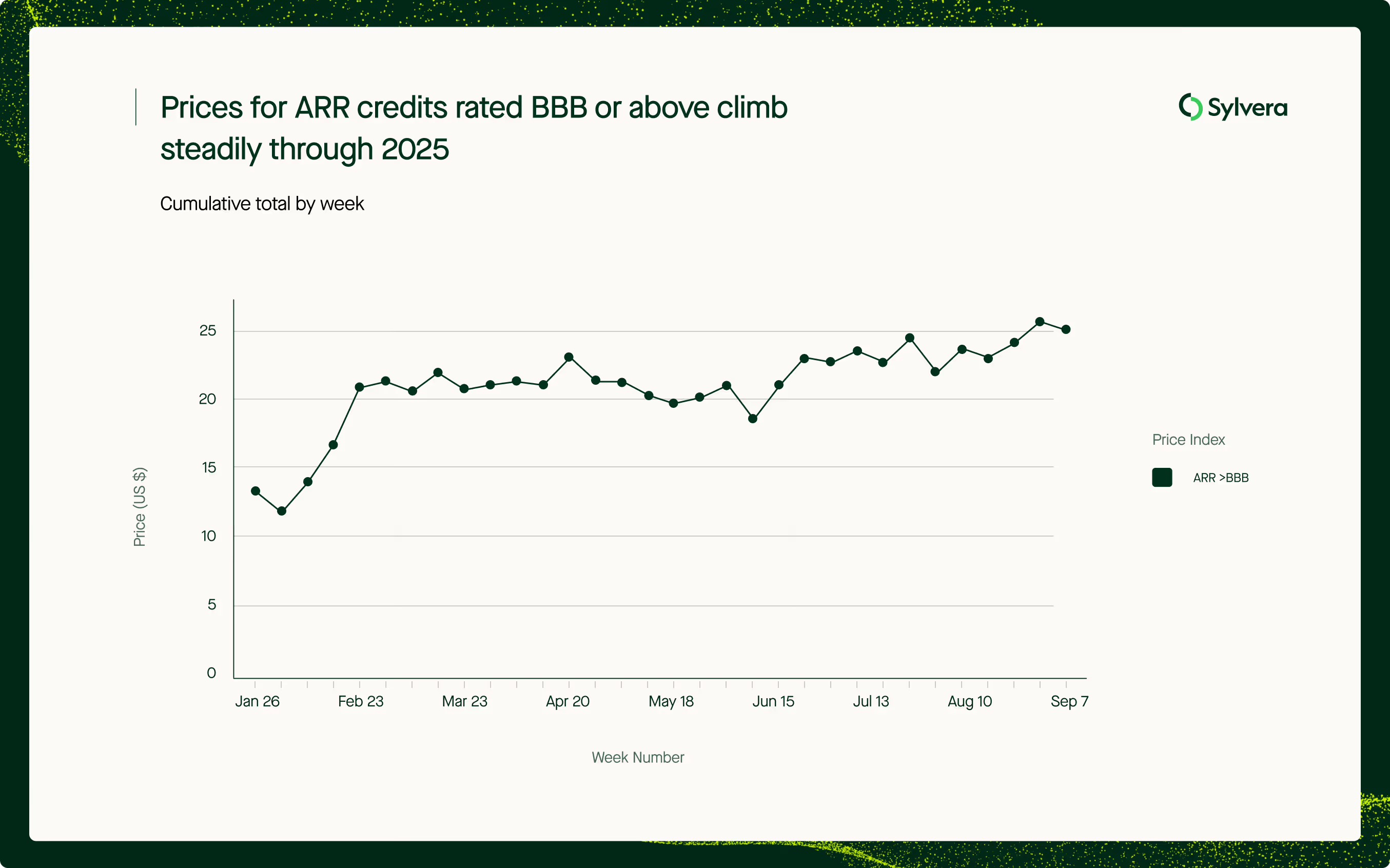

Pricing signals show premium for quality

Our new Quality-Weighted Price Index reveals a clear premium emerging for higher-quality ARR (Afforestation, Reforestation and Revegetation) credits. Prices for ARR credits rated BBB or above have climbed steadily throughout 2025, reaching US$24 in September, up $10 since the start of the year.

Aaron Tam, Product Director at Sylvera, explained: “The increase in ARR prices reflects a clear shift in buyer priorities. We are seeing a larger share of high-quality projects, such as TIST projects and projects with new, stricter methodologies, entering the market, which is driving up average prices. The level of demand we’ve seen at these prices suggests that buyers are increasingly willing to pay a premium for integrity and proven climate impact, viewing these projects as a more secure, long-term investment.”

Looking beyond spot prices in the market today, future pricing for ARR credits also shows strength, some developers are seen quoting forward prices for upcoming vintages as high as US$50 or more, indicating robust demand for nature-based removals projects.

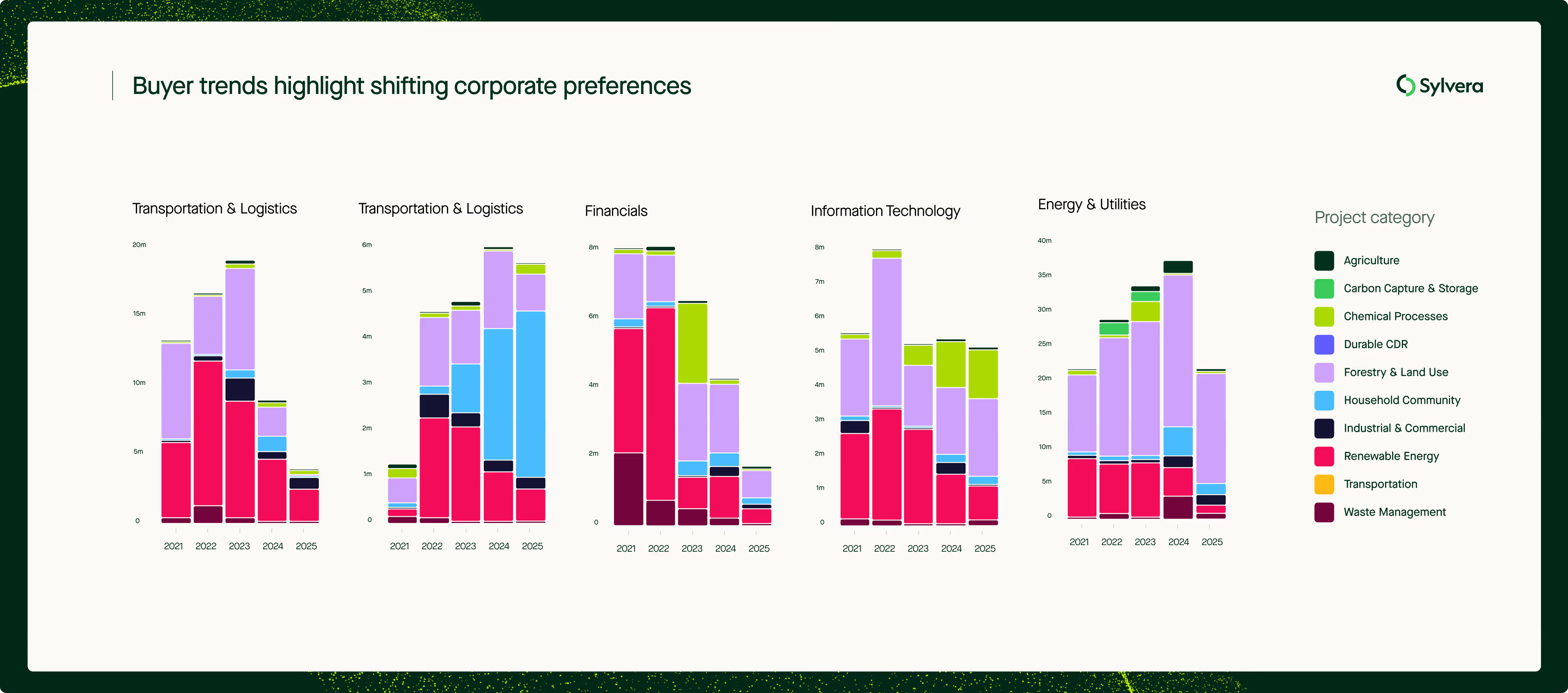

Buyer trends highlight shifting corporate preferences

Meanwhile, Sylvera’s Buyer Directory reveals notable shifts in how different sectors approach carbon credit purchasing. Latest retirements in 2025 indicate that professional services firms accelerated their use of carbon credits from cookstove projects, which now represent around 70% of known retirements by the sector. The use of renewable energy carbon credits continued a steady decline in most sectors, and fell most significantly amongst technology, financial, and professional services firms. Transportation and logistics firms stood out as an exception to this trend, with renewable energy credits still representing 60% of their demand.

Despite perceptions of a retreat in corporate climate commitments, energy and utility firms continue to dominate demand in carbon credits, representing close to 40% of non-anonymous retirements in 2025, comparable to last year.

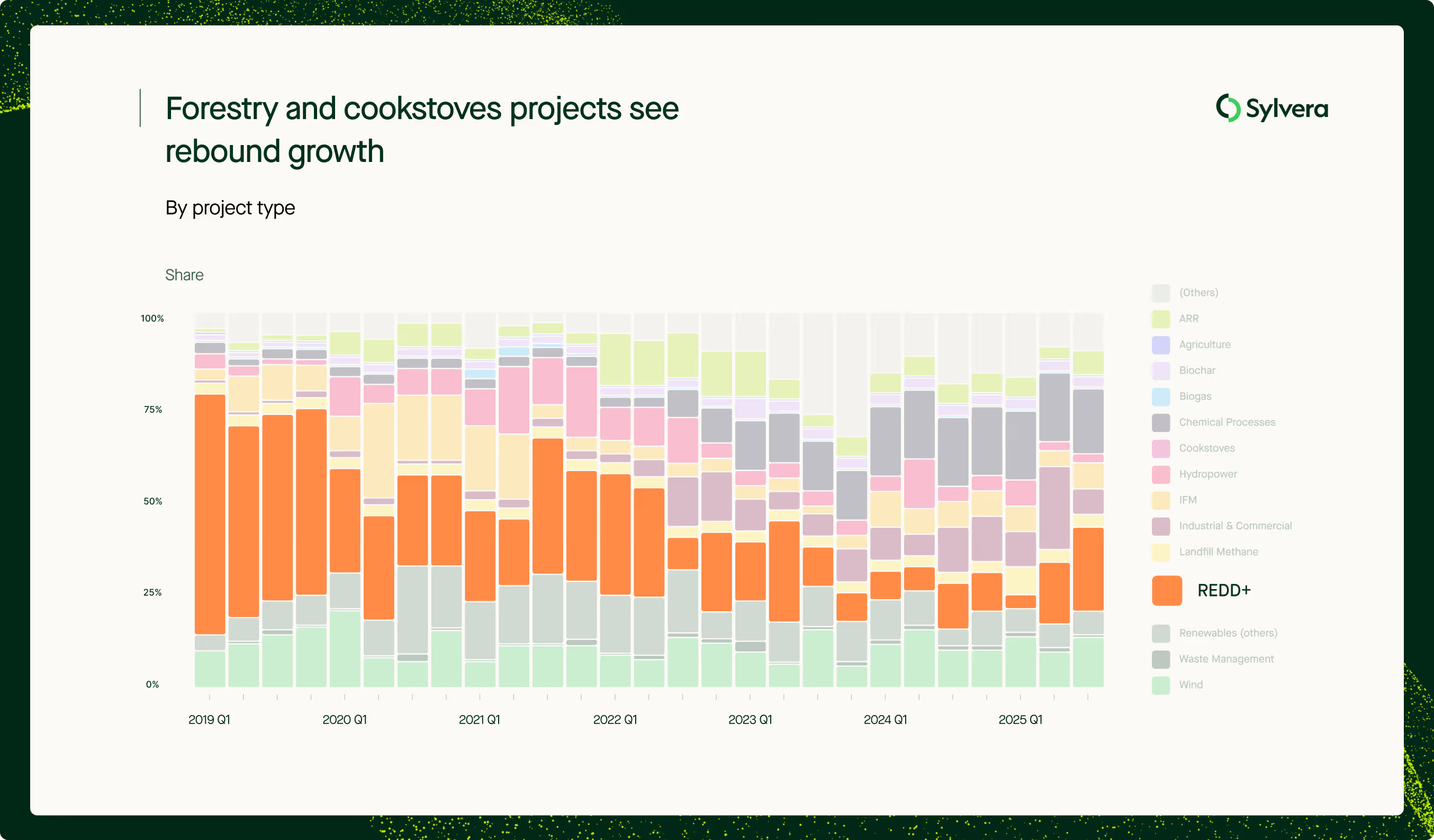

Registries and project types see rebalancing

Verra’s share of new issuances continues its long-term decline, dropping to 28.09% in Q3 2025 compared to 39.2% for the same period two years ago, reflecting a continued slowdown ever since Verra REDD+ project issuances peaked in 2021. In contrast, BioCarbon Standard has reached a record high share of 21.16%, driven by the issuances of several large REDD+ projects in Latin America supported by regional demand.

Issuances from forestry projects performed strongly in Q3. REDD+ projects saw a significant rebound in particular, making up 26.05% of issuances compared to 16% in Q2 and just 10% in Q3 last year. This suggests improving buyer trust in the project type, which has seen improvements in overall quality driven by enhanced methodologies, better monitoring, and more stringent standards addressing previous concerns around accounting and additionality.

Compliance-ready credits gain traction

The volume of CCP-labelled credits – those aligned with the Integrity Council for the Voluntary Carbon Market’s Core Carbon Principles – continues to grow. So far in 2025, 16.63 million credits have been issued with CCP-approved labels, highlighting a shift towards recognised standards of quality and integrity.

Meanwhile, compliance markets are becoming increasingly integrated with voluntary systems. A total of 67.17 million credits issued this year belong to standards and methodologies that have been approved for use in the first phase of CORSIA, subject to receiving host country authorizations. Notably, this represents one third (33.3%) of total credits issued this quarter, up from 27.1% for the same period two years ago.

Market outlook for the final quarter

The Q3 data signals a market moving towards greater maturity and sophistication. Quality is increasingly rewarded, both through higher prices and corporate demand for trusted projects. Registries are diversifying as buyers seek assurance and integrity, while compliance schemes like CORSIA are narrowing the gap between voluntary and regulatory markets.

Allister Furey, CEO at Sylvera, said: “The growing premium for high-quality credits demonstrates that integrity is now a key driver of value. Buyers are becoming more selective and project developers are responding by meeting higher standards.

This alignment between quality expectations and market demand is critical for scaling carbon markets to deliver genuine climate impact at lower economic cost.”

As 2025 enters its final quarter, these trends indicate a market maturing beyond quantity alone, with transparency, trust and compliance readiness at its core.

Want to explore these market dynamics yourself?

Our Market Intelligence suite provides transparency across the market with real-time pricing, supply and demand data.

💲 Pricing Data – Project-level spot estimates, with 20,000+ estimates powered by ~300,000 transactions.

📈 Market Data – Weekly issuances and retirements, filterable average prices, and known supply integration.

🏢 Buyer Directory – See who’s retiring what by sector, type, vintage, and geography to validate demand.

Find out more about Market Intelligence here, or request your free demo now.

For a full dive into the latest intelligence around pricing, quality, and demand trends, check our comprehensive State of Carbon Credits report.