“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

From compliance moves that could reshape demand overnight to the financing breakthroughs that will determine which carbon removal technologies scale, the next twelve months will set the trajectory for the decade ahead in carbon markets.

The fragmented landscape of previous years is giving way to more structured segments, clearer price signals, and the early stages of genuine market maturity.

Drawing on insights from our platform, policy analysis, and conversations with hundreds of market participants, we asked four Sylvera experts to identify the critical trends they’re predicting to shape carbon markets in 2026.

For all the latest intelligence around pricing, quality, and demand trends, check our comprehensive State of Carbon Credits report.

Prediction 1: The New Shape of Carbon Credit Markets

Aaron Tam, Product Director

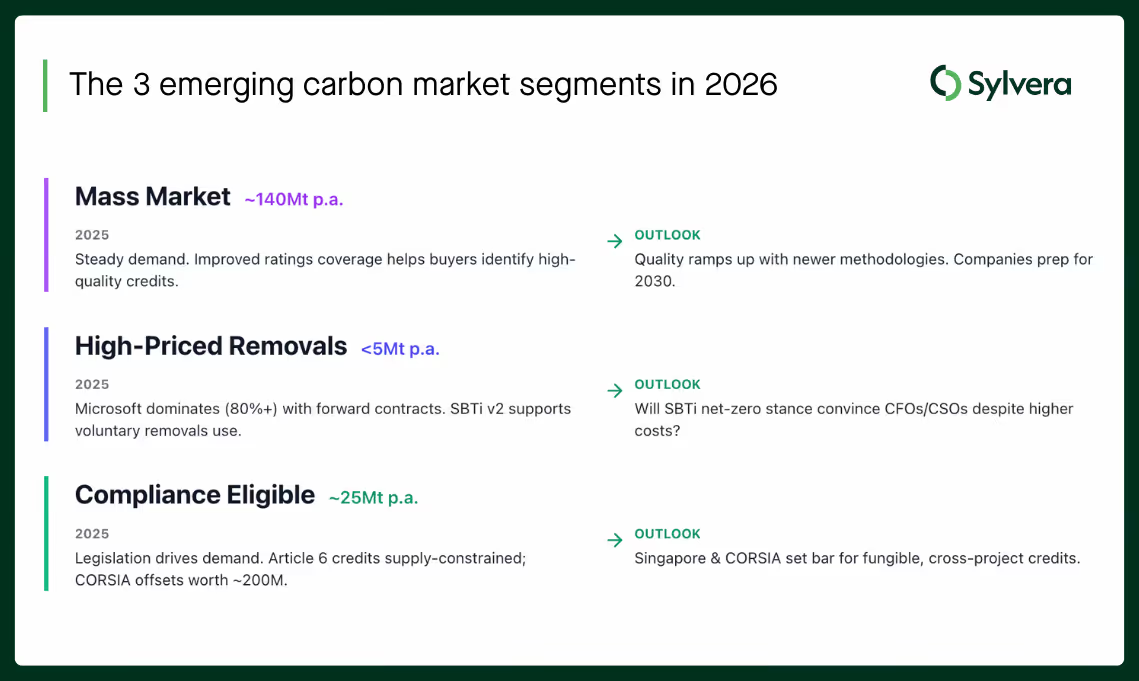

In 2026, carbon credit markets will accelerate its convergence towards three broad clusters: compliance-eligible, high-priced removals, and the mass market. This movement will drive distinct price and demand expectations.

Why will this happen?

Across 2025, market behaviour signalled a shift away from a fragmented project-by-project universe toward three emerging segments, each moving under its own structural forces:

- Mass market (~140 Mt/year): Buyer behaviour stabilised as improved ratings coverage and clearer guidance (incl. CCPs) made it easier to identify high-quality credits. As more methodologies issue credits in 2026, this segment will continue drifting toward quality-filtered procurement, especially as companies prepare for 2030 milestones.

- High-price removals (<5 Mt/year): A small but influential group of buyers (dominated by Microsoft at >80% of forward purchases) continued setting the tone for high-durability, high-cost removals. The new SBTi Net-Zero Standard v2 supports voluntary removals use — but it remains unclear whether this unlocks broader corporate participation given corporate price sensitivity.

- Compliance-Eligible (~25 Mt/year): Rapid expansion of legislation integrating project-based credits into compliance systems is already pushing demand up. The most constrained segment is Article 6, with CORSIA facing ~200M tCO₂ of offsetting demand due by Jan 2028 — far above currently available eligible supply.

Taken together, these dynamics mean that investors and project developers traditionally used to a wide and fragmented VCM need to take a more strategic approach on how to serve different market segments.

What’s the predicted impact of this?

For developers and investors:

There are opportunities everywhere, but the strategy will differ depending on the market focus.

- For compliance: locate the low-cost credits that meet the eligibility/quality criteria, and could be delivered to market in time for key compliance timelines.

- For high-priced removals: identify and focus on the defining features that justify the price premium.

- For mass market: produce high quality credits to position well in an increasingly competitive market.

For buyers:

Procurement strategy should diverge across buyers. Buyers in the mass market now benefit from more transparent quality signals and can make reasonable tradeoffs against spot market prices. Meanwhile, buyers of high-priced removals continue to move upstream, seeking to secure future volumes by signing offtakes today. Compliance-aligned buyers, especially CORSIA, could increasingly look to rely on intermediaries who could secure larger volumes and manage delivery risks more effectively.

For policymakers & regulators:

Policy and regulatory certainty will make or break compliance markets like CORSIA - both in terms of the supply of corresponding adjustments and the enforcement of compliance obligations. Meanwhile, early Article 6 buyers like Singapore will have an outsized impact as it begins to shape expectations for 'what good looks like' in the context of sovereigns using international credits for their NDCs.

Prediction 2: CORSIA phase 1 futures prices will rise as the market begins to recognise a structural shortfall in eligible supply

Ben Rattenbury, VP Policy

Why will this happen?

CORSIA Phase 1 futures for Dec-2026 and Dec-2027 delivery are trading around $16, notably below the current spot prices for the very limited supply of credits that are actually eligible today. The futures curve implies the market expects Phase 1 eligible supply to expand rapidly enough to outpace rising compliance demand.

However, our modelling indicates the opposite is more likely.

- Eligible supply growth remains constrained by the lack of material progress among host governments to apply corresponding adjustments to eligible projects

- Meanwhile, ICAO’s adoption of the 2024 baseline and continued post-COVID recovery in aviation suggest compliance demand will rise faster than previously assumed.

- Few new activities are on track to issue significant volumes before 2026–27, which tightens the supply–demand balance precisely in the years these futures settle.

As the market internalises these dynamics, futures prices will need to adjust upward to reflect a more realistic scarcity premium.

What’s the predicted impact of this?

CORSIA Phase 1 faces a structural supply gap that is not yet fully priced in. This mispricing sends an artificially weak demand signal to:

- Project developers, who could bring forward CORSIA-eligible volumes if price signals justified investment; and

- Governments, who can approve or adjust activities that determine eligibility.

A stronger, more accurate price signal is essential to mobilise supply ahead of peak compliance years and the market will increasingly recognise this as 2026 approaches.

Read our CORSIA First Phase Scenario Modeling Report here.

–

Prediction 3: CDR - The Year Engineered CDR Becomes Financeable at Scale

Paul Budin, Head of Framework

In 2026, engineered carbon removal (CDR) will see its first meaningful drop in effective levelized cost, as projects move beyond the “first-of-a-kind” (FOAK) financing premium. The catalyst won’t be new breakthroughs — it will be better bankability: improved contract structures, clearer performance data, and lower perceived project risk.

Why will this happen?

Today, a significant share of CDR costs is driven by the cost of capital, not the underlying technology. FOAK DAC and BECCS plants are still financed like high-risk ventures. But the market is shifting. Multi-year offtake agreements from initiatives like Frontier and NextGen, early government procurement signals (including U.S. DAC Hubs), and more transparent performance data from pilot facilities are all reducing uncertainty. Many developers’ next-generation designs are explicitly targeting commercial readiness, enabling more infrastructure-style financing. Sylvera’s modelling shows that even modest reductions in WACC can materially lower delivered $/tCO₂.

What’s the predicted impact of this?

For developers:

Lower financing costs mean previously marginal projects can now move to FID. Developers should reassess stalled projects, update financial models with lower WACC scenarios, and begin preparing NOAK-standard documentation (bank models, performance data, long-term offtake structures) to capitalise on the shift.

For investors:

As engineered removals move toward an infrastructure-like risk profile, investors should start building sector theses now, identify developers approaching commercial readiness, and explore longer-tenor structures that were previously too risky.

For buyers:

Buyers should revisit multi-year removal strategies, evaluate whether emerging contract structures (e.g., fixed-price, volume-forward, portfolio offtakes) could lock in value sooner, and strengthen due diligence frameworks to differentiate credible projects from speculative ones.

Prediction 4: CDR - And 2026 will be the year new CDR buyers enter the market at scale

Hugo Lakin, CDR Lead

Why will this happen?

While 2025 didn't deliver anticipated CDR market growth, it established crucial groundwork for 2026. Policy mechanisms are moving to implementation (CRCF standards, UK procurement, Canada's tax credits), new technologies are issuing credits (10+ ERW projects, a dozen BECCS and DAC facilities expected by year-end), and quality ratings are giving non-specialist buyers confidence. Early evidence is already visible: financial institutions like Barclays and trading firms like IMC are purchasing novel credits like ERW and DAC, while industrial companies like Schneider Electric are starting to build serious SBTi aligned CDR programs.

What’s the predicted impact of this?

For developers:

New buyers bring new scrutiny. Developers who can clearly explain project risks and align with emerging standards will win this wave of demand. Competition is likely to be fierce in the biochar markets, as new developers flood in at the same pace as new buyers.

For buyers and investors:

This growth will be crucial for moving CDR projects down the cost of capital curve, as demand increases and developers prove consistent delivery, project finance risk premiums will decline, unlocking the next phase of scale.

Looking ahead

These aren't isolated trends, but show connected signals of a market maturing. The fragmented, project-by-project world of early voluntary carbon markets is being replaced by something more structured.

Project developers who understand and strategically target the market segment they're serving; buyers who can differentiate quality and manage delivery risk; and investors who recognise the shift from venture risk to infrastructure returns - will be best positioned to capitalise on these dynamics.

Meanwhile, for policymakers, the decisions made in 2026 will shape market functionality for years to come.

As 2026 unfolds, the ability to move quickly, make informed decisions, and adapt to rapidly changing market conditions will separate leaders from followers. Sylvera's platform and expertise are designed to help you do exactly that.

Get started with your own 1-2-1 demo

Want to get started with using the Sylvera platform in your strategic decision-making? We’d love to help. Request a demo to see our market-leading carbon data platform in action for your business. Or try the free access version right now.

For all the latest intelligence around pricing, quality, and demand trends, check our comprehensive State of Carbon Credits report.