“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

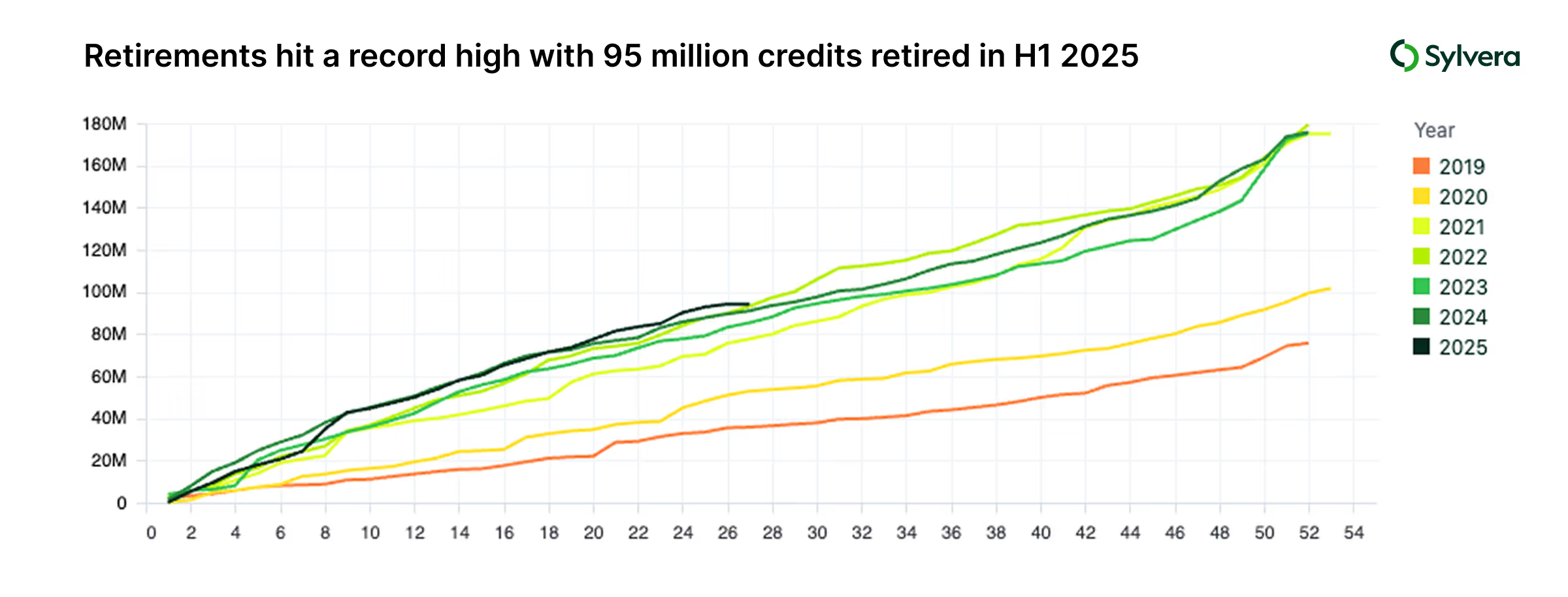

Carbon credit retirements hit all-time high, quality drives market evolution

Carbon credit retirements have hit a record high with 95 million credits being retired in H1 2025

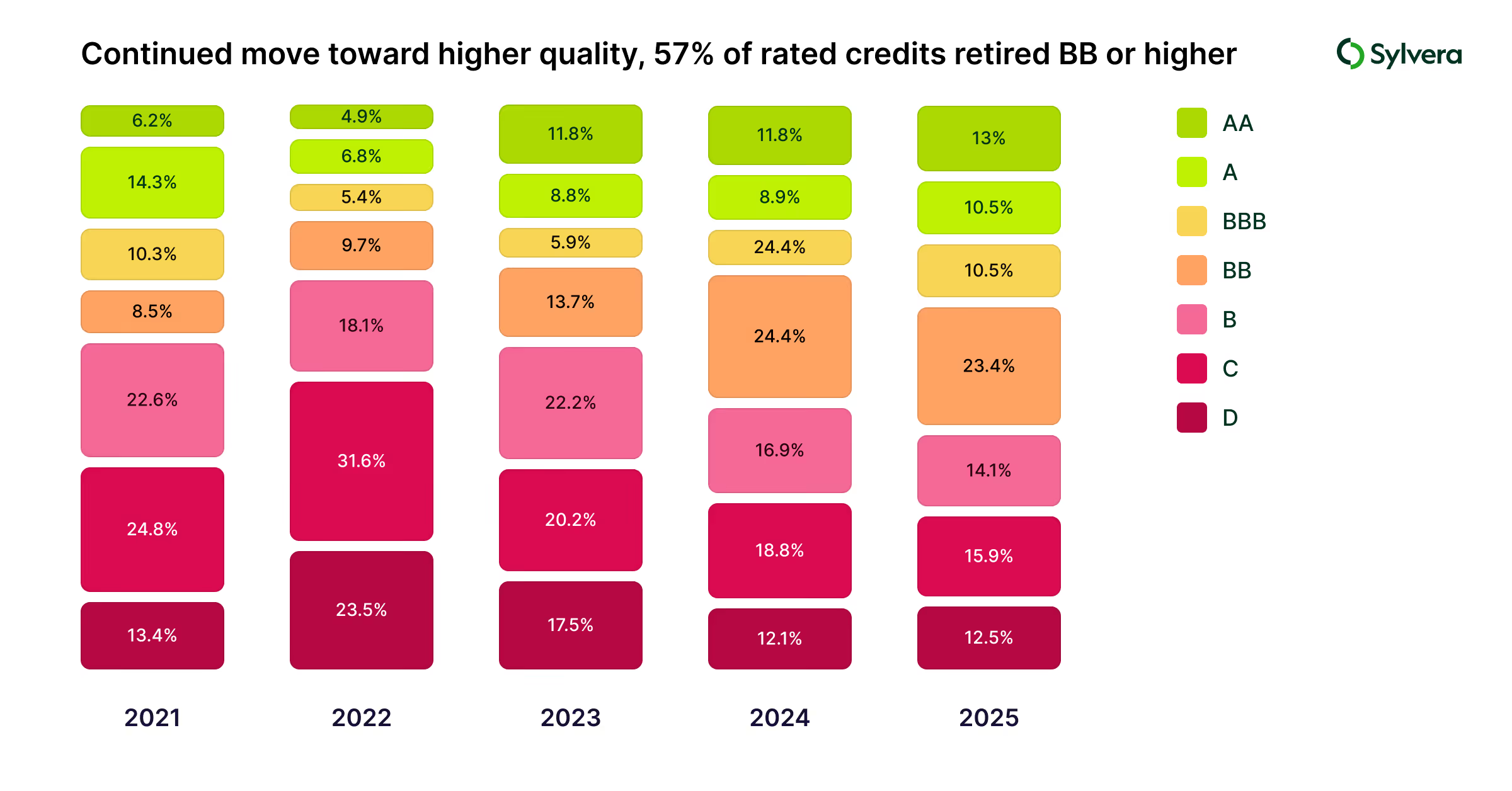

Higher-quality credits dominate with a majority (57%) of Sylvera-rated credits retired in H1 2025 holding BB ratings or above, demonstrating the impact of enhanced standards and a greater focus on integrity

Issuances of credits jumped to 77 million in Q2 2025, up 39% from the prior quarter

Over a third (37%) of credits issued this quarter are potentially eligible towards Phase 1 of CORSIA, subject to host country authorizations under Article 6 of the Paris Agreement.

For a full dive into the latest intelligence around pricing, quality, and demand trends, check our comprehensive State of Carbon Credits report.

Carbon credit retirements surged to 95 million in H1 2025, the highest half-year figure ever recorded, according to an analysis by carbon data provider Sylvera. In carbon markets, retirement is the process of using a credit to offset emissions and making it no longer tradable.

On the supply side of the market, Sylvera has recorded a flurry of issuances - the process of newly creating credits that are available for trading - with 77 million credits being issued, an increase of 39% from the first quarter of the year, and up 14% when compared to Q2 2024.

Quality standards drive market evolution

The data reveals a shift toward higher quality, with 57% of Sylvera-rated credits retired in H1 2025 holding BB ratings or above - up from 52% throughout 2024. This trend reflects the market's increasing sophistication as buyers are better-informed of integrity considerations of carbon credits, in part due to clearer guidance from ICVCM’s Core Carbon Principles, as well as the growth of carbon credit ratings and other due diligence services in the market.

As we mark the halfway point of the first phase of CORSIA, the UN’s global carbon offsetting scheme for international aviation, over a third (37%) of credits issued belong to projects that are potentially under standards and methodologies that have been approved by ICAO towards towards Phase 1 of the scheme. This is a significant increase from the same period in 2024, where only 28% qualified.

The scheme would require airlines from participating states to offset the growth in their international aviation emissions above 2019 levels using eligible carbon credits, with the Phase 1 cancellation deadline due by January 2028. However, it remains uncertain to what extent these projects will secure host country authorizations that are required for CORSIA compliance.

Allister Furey, CEO at Sylvera, said: “Demand for credits and, in particular, high-quality credits is at an all-time high. At the same time, increasing use of project-based credits in compliance schemes is narrowing the gap between voluntary and compliance markets. Meeting both higher climate integrity standards, as evidenced by ratings, and eligibility criteria for schemes, like CORSIA, is being seen as essential for new projects in development. Market alignment with both integrity and regulatory expectations is starting to unlock the potential of carbon markets to deliver genuine climate impact at lower economic costs.”

Industrial and commercial breakthrough diversifies project landscape

Forestry and Land Use projects, such as REDD+, ARR and IFM, remained the largest category of issued credits at 31%. ARR projects in particular, which has seen increased activity in the primary market, saw an average of $24 per credit, reflecting both the relatively higher costs of implementing such projects, as well as greater willingness to pay amongst buyers seeking to procure nature-based removals credits. The price premium of ~$27 for BBB+ rated projects is fuelled by constrained supply, with ARR credits making up only 3.7% of retirements in H1 2025.

One of the quarter's more notable developments was the growth in Industrial and Commercial projects, which represented 19% of issuances so far this year, up from 7.9% in H1 2024. This category includes projects such as reclaiming refrigerants, switching to advanced blowing agents, coal mine methane capture, and other industrial energy efficiency improvements. REDD+ projects also rebounded, jumping from 3% in Q1 to 16% in Q2 - the highest level since Q2 2023's 33% peak.

Geographic rebalancing mirrors market dynamics

The North American region more than doubled its market share of issuances this quarter, with 43% of issuances originating from the continent, up from 21% in Q1. This led the American Carbon Registry to become the dominant registry for quarterly new issuances for the first time ever at 33%, followed by Gold Standard (25%) and Verra (21%).

Market outlook: convergence and growth

The Q2 surge positions the carbon market for significant evolution as voluntary and compliance mechanisms increasingly align. With leaders having agreed on high standards for project methodologies and integrity at COP29, detailed guidelines across various geographies and industries are being put in place throughout 2025, and PACM credits are likely entering the market by late 2025. This regulatory clarity, combined with CORSIA's approaching Phase 1 implementation, is driving the quality improvements evident in Q2 data.

The combination of supply growth, quality elevation, and compliance readiness suggests the carbon market is entering a new phase of institutional maturity - one where integrity and scalability converge to support genuine climate impact.

METHODOLOGY

Market data includes retirements and issuances between 1st April and 30th June 2025. The data is aggregated across major registries in the voluntary carbon market, including Verra, Gold Standard, American Carbon Registry, Climate Action Reserve, Puro, EcoRegistry, and BioCarbon Standard.

Sylvera's Market Data

Sylvera's Market Data - used to bring the insights above - has been designed to address the critical challenges faced by carbon market participants, tansforming complex market information into actionable intelligence.

Designed for all market participants

Our Market Data serves the specialized needs of various stakeholders:

- For corporate buyers: Streamline procurement decisions with fair price benchmarks and quality insights

- For investors: Identify market opportunities and perform thorough due diligence

- For project developers: Understand market demand patterns and optimize project design and pricing

- For traders and intermediaries: Real-time intelligence and pricing signals facilitate transactions and identify trading opportunities fast

Comprehensive and thoughtfully curated

Get a complete view of the carbon market while focusing on what matters most for your specific needs:

- Big picture overview: Track total market volumes, retirement trends, and supply-demand dynamics across the entire voluntary carbon market

- Weekly market movements: Monitor short-term shifts in pricing, project performance, and buyer activity

- Specialized drill-downs: Focus on specific project types, geographies, registries, or quality ratings

Interactive exploration

Our platform puts you in control of your market analysis:

- Customizable dashboards: Create personalized views that highlight the metrics most relevant to your strategy

- Multi-dimensional filtering: Segment data across multiple parameters simultaneously to uncover hidden insights

- Comparative analysis: Benchmark project types, quality levels, and pricing against each other

Proprietary data advantage

Our Market Data combines publicly available information with our exclusive proprietary data that can't be found elsewhere:

- Sylvera Ratings distribution: See how our Ratings are distributed across the market

- Pricing intelligence: Access insights from 100,000+ price points aggregated across 40+ sources covering over 1,000+ projects

- Premium analysis: Quantify the price premiums associated with higher quality ratings

Have you read our full State of Carbon Credits report?

Interested in a full year view of carbon market data? Our annual State of Carbon Credits report reveals the most important trends impacting buyers and investors across the calendar year.

The report focuses on key areas such as retirements, registry market share, project types, transparency, buyer preferences, quality and price. Read it here.