“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

- The voluntary carbon market is in transition. Issuance volumes have dipped, but retirements and spending for high-quality credits remain resilient.

- A clear quality premium is now structural: top-rated credits (especially high-integrity ARR, some CDR) trade at multiples of low-quality avoidance.

- Integrity frameworks and policy (ICVCM, VCMI Scope 3 Code, Article 6, CRCF, CORSIA) are pulling voluntary and compliance markets closer together.

- Removals, data, and forecasts move center stage: buyers want decision-grade intelligence, not just registry labels or one-off price quotes.

- Sylvera's Ratings, analytics, and Market Intelligence help corporates, investors, and traders navigate this complexity with evidence, not guesswork.

Where the Carbon Market Stands Heading into 2026

While there has been talk about the "collapse" of the global carbon credit market, that narrative doesn't match the data or true direction of the market in terms of total value. According to Sylvera's data, retirements marginally declined 4.5% to 168 million in 2025, while total market spending reached $1.04 billion, up 6% from $954 million in 2024. The truth? Demand for credits is selective and increasing in quality and price, not disappearing.

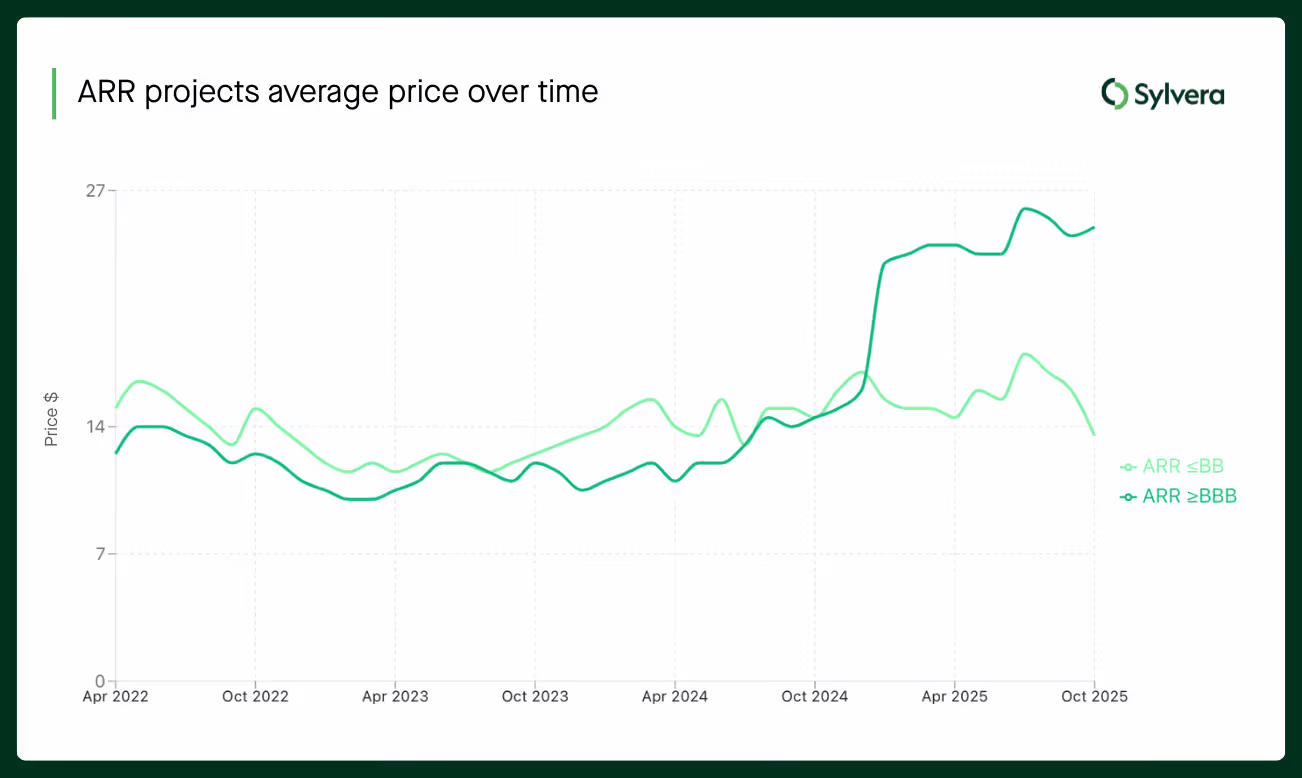

This begs the question, what do buyers want? The answer is quality. Retirements of high-quality credits currently outpace issuances in certain parts of the market. This is because modern buyers are focused on integrity, and they're willing to pay more for it. In fact, the average spot price for high-quality ARR credits rose to $26 per tCO2e in December 2025 compared to $14 at the start of the year.

Overall, the carbon market is valued at approximately $1 billion based on actual retirements, with compliance programs now accounting for 24% of total demand—up from negligible shares just years ago. Projections suggest compliance demand could match or exceed voluntary purchases by 2030. Though it should be noted, projected growth won't be evenly distributed. Capital will continue to flow to projects that meet rising integrity standards and align with emerging policy frameworks. In other words, low-quality credits will get left behind.

So, is the carbon market about to crash? No, it's just changing. Think of it this way: 2021-2023 was all about hype and backlash. 2024-2025 was the integrity reset. And 2026 will be the professionalization phase—more data, more regulation, and clearer segmentation between high- and low-quality assets.

For all the latest intelligence around pricing, quality, and demand trends, check our comprehensive State of Carbon Credits report.

6 Carbon Market Trends to Watch in 2026

Trend 1: The "Flight to Quality" Becomes Structural

The quality premium is no longer rhetorical. It's priced in, backed by data, and widening.

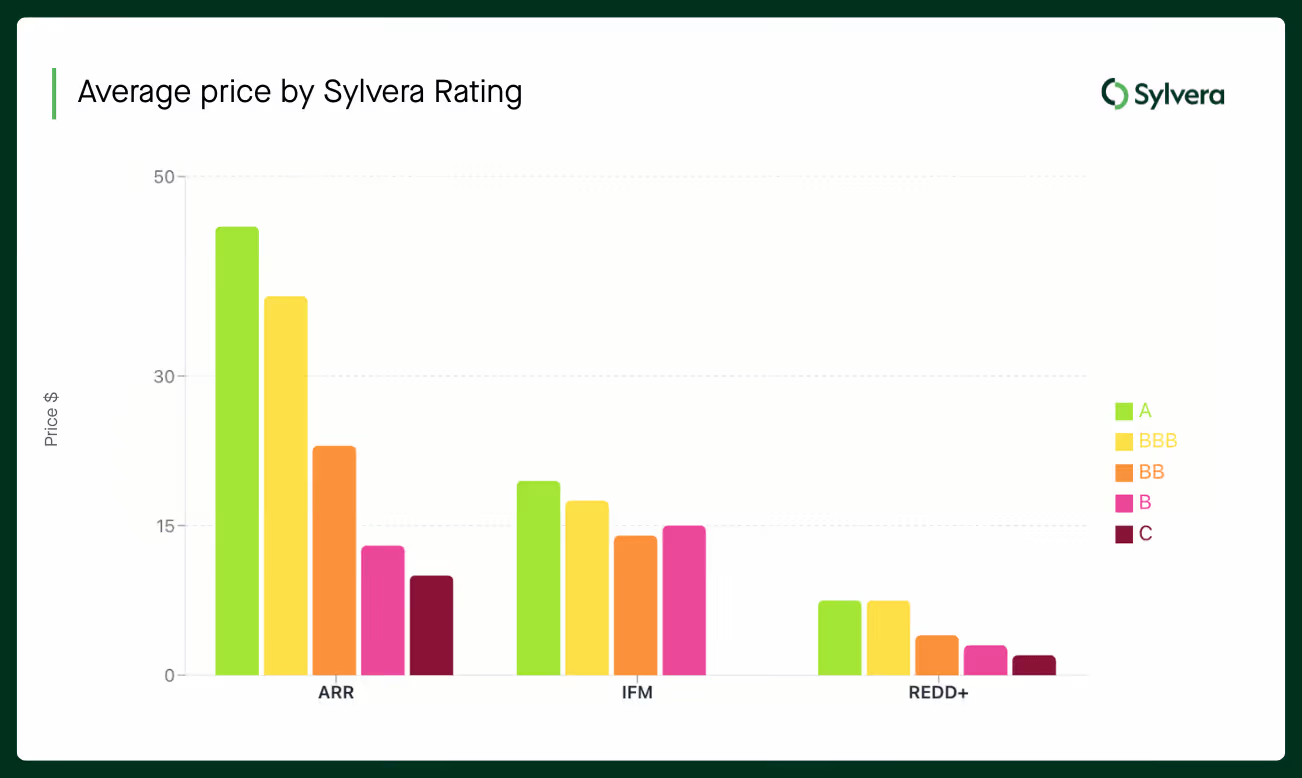

Sylvera data shows BBB+ rated ARR projects now command median prices above $35, while lower-rated equivalents trade below $20—a spread that continues widening. For REDD+ projects, the quality premium is similarly pronounced, with highly-rated projects maintaining resilient pricing while legacy projects struggle to find buyers at any price.

What changed? Both buyers and sellers now anchor on integrity frameworks, like the Integrity Council for the Voluntary Carbon Market's "Core Carbon Principles," the Voluntary Carbon Market Integrity Initiative's claims guidance, and the Science Based Targets Initiative's standards. Said standards have reshaped what corporations consider "acceptable" when it comes to offsetting carbon footprints.

Also worth mentioning, quality signals are now more granular. It's not just "nature-based solutions vs. carbon dioxide removal" anymore. Buyers examine project-level ratings, MRV robustness, permanence mechanisms, and community safeguards to empower their carbon offsetting strategies.

As seen in the Sylvera State of Carbon Credits report, there's a strong correlation between higher ratings and more resilient pricing—and for the third consecutive year, highly-rated credits experienced market deficits as demand outpaced new issuances, while lower-rated credits accumulated in oversupplied inventories.

Trend 2: Voluntary and Compliance Markets Converge

The line between voluntary and compliance markets is blurred thanks to Article 6 of the Paris Agreement, international aviation offsets, and the EU's Carbon Removal Certification Framework (CRCF).

The COP30 event in November 2025 brought clarity to Article 6.4 mechanisms, removal standards, host-country readiness, and ITMO pipelines. Because of CORSIA Phase I, airlines now need CORSIA-eligible credits for emissions above 85% of 2019 levels, turning them into anchor buyers for high-integrity reductions and removals. And to top it off, the EU and UK are building pathways to integrate durable removals into their emissions trading systems within the second half of the 2020s.

Put simply, corporate strategies can't treat "voluntary" and "compliance" as separate universes anymore. To plan an effective reduction scheme for 2026, you need to consider compliance eligibility (or future eligibility) of credit types, host-country policy risk and corresponding adjustments, and the interaction between internal decarbonization pathways and market purchases.

Sylvera's Article 6 Intelligence Report and policy tracking efforts help organizations understand jurisdictional risk and compliance potential, not just credit-level quality.

Trend 3: Corporate Use of Credits Shifts Under New Integrity Rules

The way companies use carbon credits is changing due to market developments and new regulations.

For example, the VCMI Scope 3 Action Code allows the use of high-quality credits for a defined share of Scope 3 emissions gaps, with strict disclosure requirements. Meanwhile, the SBTi continues to refine its stance on credits, acknowledging that Scope 3 reductions are falling behind targets industry-wide. The global Scope 3 emissions gap is estimated at 1.4 billion tonnes and could grow fivefold by 2030.

In addition, CSRD and similar disclosure regimes push companies to show how credits fit within their overall decarbonization plans, not as a substitute for real-world action.

The message is clear: Climate strategies must lead with decarbonization and only use credits to address residual emissions gaps. They must also document claims and use-cases, and build an audit-ready narrative that explains why projects are chosen, the integrity checks used to confirm high integrity credits, and how performance will be monitored to ensure future supply.

Trend 4: Carbon Removals Markets Mature (But Stay Constrained)

Carbon dioxide removal isn't a bubble, but it's not scaling as fast as some predicted.

The question is why? It's not complicated: CDR projects are constrained by high costs, heavy policy dependencies, and difficult financing paths. For example, novel CDR technologies cost more than $100 per tonne—with sustained premiums—when compared to avoidance and nature-based removals.

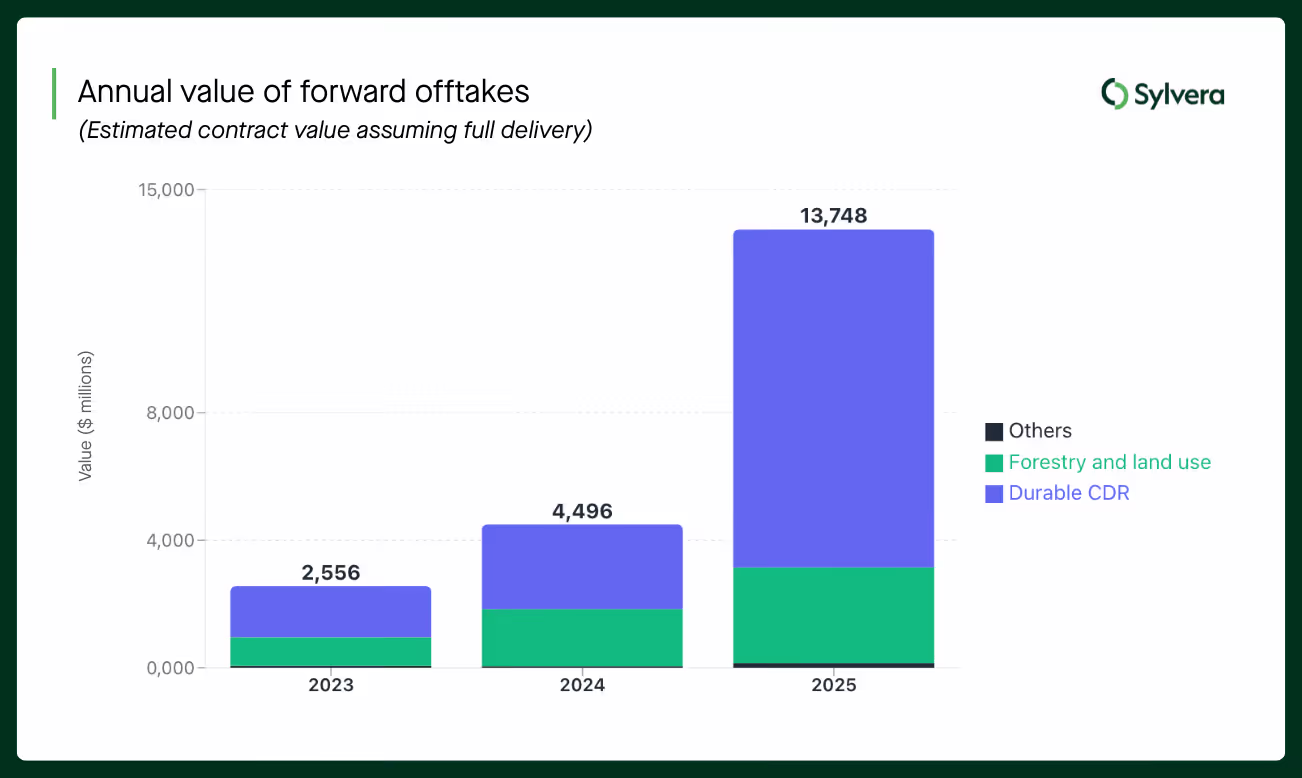

But there's both progress and reality checks. Offtake agreements announced in 2025 totaled $13.7 billion—more than 14 times the value of credits actually retired—though these commitments will deliver just 78 million credits spread across the next decade at an average price of $180 per credit. Meanwhile, actual durable CDR retirements remained under 200,000 credits in 2025, representing just 0.11% of total retirements.

This dramatic gap between forward commitments and actual deliveries reflects the nascent state of the market. Corporate buyers are building portfolios that mix nature-based removals and engineered CDR for long-term net-zero alignment, but the concentration among roughly 100-200 buyers (with Microsoft alone accounting for 58% of tracked offtake volumes) underscores the challenges in broadening appeal beyond early adopters.

Still, bankability challenges remain. Project financing is complex; offtake agreements require 45Q tax credits, GGR business models, and/or the EU Innovation Fund; and capital is scarce.

In 2026, expect durability and cost curves to face more scrutiny than ever. Anticipate limited supply of truly durable and high-integrity removals, and plan early via offtakes. Also, only invest in future projects that include independent validation of economics and quality. To learn about other key trends in the world of carbon dioxide removal, download our CDR Market Survey report.

Trend 5: Pricing Fragmentation Makes Market Intelligence Non-Optional

Here's the uncomfortable truth: there is no "carbon price." There are hundreds of micro-markets, and each project type has its own average price based on growing demand in the voluntary market.

ARR trades differently than IFM, which trades differently than REDD+, which trades differently than tech-based removals. Spot prices diverge from offtakes, which diverge from forward curves, and all depend heavily on quality, counterparty, and compliance potential.

The weighted average spot market price of $5.6 per credit masks major variation. For example, 50% of ARR projects trade between $5 and $25, with outliers ranging from $2 to over $50. The forward market shows even wider spreads, with durable CDR offtakes averaging $180—more than 30 times the spot market average.

Because of these things, buyers can't rely on single benchmark indices, ad-hoc broker quotes, or market anecdotes. They need a full-fledged solution to stay on top of pricing details.

Enter Sylvera's Market Intelligence. Our platform integrates spot price estimates for over 20,000 credits, powered by 300,000 price transactions and seven price indices, and includes live data on issuances, retirements, and trends across 19 registries. In other words, it's a full-fledged solution.

Whatever tool or methodology you use, planning for 2026 will require scenario-based budget models using forward curves, not point estimates. You'll also need the ability to benchmark prices against quality and project characteristics. Without this intelligence layer, you're flying blind.

Trend 6: Data, Ratings, and Transparency Become Market Infrastructure

Carbon intelligence is the name of the game in 2026.

Independent ratings, digital MRV, and analytics platforms are now core infrastructure for buyers during budgeting and procurement processes, investors during due diligence and risk pricing tasks, traders to assess relative value and liquidity, and developers to ensure bankability and minimize cost of capital.

Sylvera combines ratings, real-time pricing, Article 6 and compliance insights, and retirement analytics to create a carbon intelligence platform that supports everyday decisions across the carbon lifecycle. Whether you want to invest in nature based projects or technological innovations, you can do it better with Sylvera. That's why some of the biggest brands in the world use our tools.

What 2026 Carbon Markets Trends Mean for You

Are you a corporate buyer, investor, or project developer? Your answer will determine how these voluntary carbon market trends impact your efforts. Here's what you need to know:

For Corporate Buyers and Sustainability Teams

Don't budget with flat "price per tonne" assumptions. Instead, plan multi-year budgets using scenarios that account for quality premiums, policy shifts, and supply constraints. Then, build quality-first procurement policies that reference standards, ratings, and internal thresholds. Finally, design portfolio approaches that mix geographies, methodologies, and durability to manage risk.

For Investors and Financial Institutions

Integrate credit quality ratings and policy risk assessments into investment committee processes. Then, use a market intelligence tool like Sylvera to spot mispriced assets, i.e. quality credits that should command higher prices but don't because of category overhang. Finally, stress-test CDR and nature-based solution strategies against policy and price volatility scenarios.

For Project Developers

Treat integrity, co-benefits, and bankable economics as a legitimate revenue strategy, not nice-to-haves perks. Then, use ratings and market data to make the case for remedial actions and capex that improve ratings and pricing. Finally, position projects for future compliance eligibility. Doing so will help you meet increasing demand, build a strong reputation, and drive more revenue.

How Sylvera Helps You Navigate 2026 Carbon Credit Market Trends

Sylvera provides the carbon intelligence infrastructure needed to power effective strategies in 2026:

- Ratings and Quality Analytics: Access independent project-level assessments for buyers and investors so you can quantify integrity and delivery risk rather than rely on registry labels.

- Market Intelligence and Pricing Data: Enjoy real-time and historical price data, spreads by project type and quality, retirement details, and supply-demand analytics across more than 20,000 credits on the voluntary carbon market.

- Market Forecasts: View scenario-based price and demand curves that extend out to 2050 to help your team budget and sequence procurement effectively.

- Policy and Article 6 Insights: Assess country readiness, CORSIA and COP30 outcomes, and compliance eligibility trends to connect voluntary decisions to regulatory futures.

If you need to set a 2026 carbon credit strategy, you need a single source of truth on quality, price, and policy. Sylvera was designed to provide these things. Book a demo to see for yourself.

Build a Rock-Solid Climate Strategy for 2026

2026 is the year carbon markets get professionalized.

The global carbon market trends are clear: quality focus, compliance convergence, pricing fragmentation, and data-driven decision-making. Those who succeed in this environment will treat carbon as a strategic asset class to reduce emissions and build brand, supported by robust carbon intelligence. They will NOT treat it as another procurement line item.

At the end of the day, the market has moved beyond registry labels and broker quotes. It demands evidence, transparency, and actionable intelligence that deliver key insights, which Sylvera provides.

Get the latest carbon credit trends and data

For all the latest intelligence around pricing, quality, and demand trends, check our comprehensive State of Carbon Credits report.