“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

Convergence beyond Carbon Credits

For years, carbon markets operated in distinct silos. Voluntary buyers purchased credits. Compliance schemes ran separately. Article 6 mechanisms took shape slowly. Physical commodity markets were separate.

That world is gone.

Consider these real-world examples happening today:

- Tech companies are actively choosing between buying voluntary carbon removal credits (including engineered CDR) or paying premiums for low-carbon steel and cement in their supply chains for data center construction.

- ADNOC and Mitsui have pioneered a collaboration where low-carbon ammonia production is effectively subsidized through Japan's domestic carbon credit market – creating a direct bridge between Article 6 mechanisms and physical commodity trade.

- Airlines must now balance CORSIA-eligible carbon credits, sustainable aviation fuel costs, and emerging low carbon aviation fuel (LCAF) premiums in their compliance strategies.

- Producers of commodities such as cement, ammonia, and hydrogen face a fundamental choice about how to monetise their low-carbon attributes. From generating carbon credits from their lower-emission process, to selling at a price premium for lower carbon intensity, or getting certified under specific compliance schemes.

This convergence is being driven by powerful, accelerating forces:

CBAM and compliance schemes are growing, with carbon pricing being utilised more and more. The "penalty net" is tightening – what was once a voluntary choice is increasingly becoming a cost of doing business.

Sectoral schemes like CORSIA (aviation) and FuelEU Maritime create formal, quantitative links between emission intensity and both carbon credits and carbon pricing. These aren't parallel systems anymore; they're integrated mechanisms.

Net-zero transition plans are moving from voluntary commitments to mandated requirements, creating sustained demand for carbon-differentiated products.

Moving from energy transition to energy expansion. Global energy demand isn't static, it's growing. The question isn't simply how to replace existing energy systems, but how to meet expanding demand with progressively lower carbon intensity.

This has become a hot topic, and was a focus at Abu Dhabi Sustainability Week 2026, as Sylvera’s CEO, Allister Furey, presented a panel discussion with ADNOC and S&P Global, highlighting key opportunities and challenges in the space.

The Data Challenge

Here's where the data problem becomes critical.

The diversity of carbon accounting systems creates enormous challenges for reconciliation and potential double-counting. You can't have well functioning markets when:

- EU ETS uses one methodology, China's carbon market another, and CORSIA yet another

- German low-carbon steel standards differ fundamentally from Indian production metrics

- Japanese domestic carbon credits operate under different rules than Article 6 mechanisms

- Each scheme defines "carbon intensity" slightly differently

Without a way of being able to compare carbon intensity across facilities and transparent data, buyers can't make informed decisions. Producers can't reliably price their carbon-intensity related premium. Capital can't flow to the best decarbonization opportunities.

This fragmentation isn't just inconvenient, it's actively harmful. It creates arbitrage opportunities for the unscrupulous, penalizes honest producers who can't prove their performance, and slows down the entire transition.

The good news? We're seeing early infrastructure emerge. But for carbon-differentiated commodities, we're still in the early innings.

Beyond Color Categories: Why Carbon Intensity Matters

One of our key discussion points challenged how markets currently think about low-carbon commodities: Should we price on continuous carbon intensity curves rather than arbitrary color thresholds?

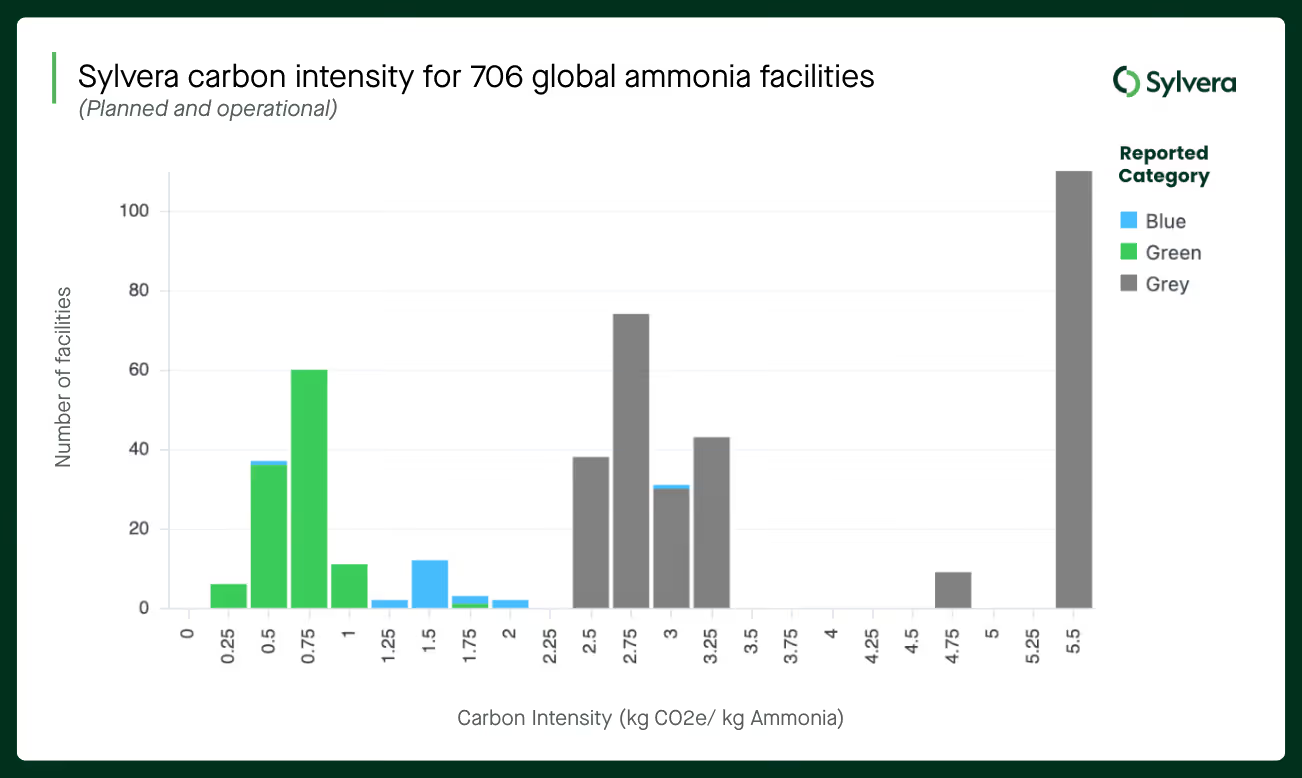

The ammonia market illustrates the problem. Today, we use rigid color categories of green, blue and grey. However, different schemes have different definitions for each of these, and this categorical thinking misses crucial opportunities.

The emissions spread between the worst and best performers for a commodity can be significant. For example, for ammonia facilities, you can see a spread in carbon intensity calculated using Sylvera’s framework from 0.25 to 5.5 kgCO2e/kg ammonia. If we disadvantage marginal worst emitters enough to drive improvement or closure, we trigger rapid, system-wide decarbonization.

ETS and CBAM schemes already price every kilogram of CO2e. It makes far more sense to extend that logic to commodity pricing than to create artificial thresholds that create gaming incentives and cliff effects.

Without predictable, continuous premium curves, investment decisions become binary gambles: hit the threshold or don't invest. With granular Carbon Intensity-based pricing, every improvement has commercial value, making the investment case much clearer.

What's Next?

For carbon-differentiated commodity markets to scale with credibility, liquidity, and trust, several critical pieces must fall into place:

- We need comparable carbon intensity data that enables market participants to make informed decisions. Complete harmonization of data and measurements of carbon intensity across all jurisdictions may be unrealistic given national interests. But we can achieve interoperability – common data standards that allow translation between systems, registries that prevent double counting, and transparent benchmarking that reveals true performance distributions.

- Markets should move beyond color categories to pricing on a continuous carbon intensity, where every tonne of CO2e improvement carries commercial value, and incremental improvement is rewarded.

- Enable producers to understand and navigate different mechanisms available to them to monetise their lower carbon intensity products and the potential value they can generate.

How Sylvera Is Supporting This Transition

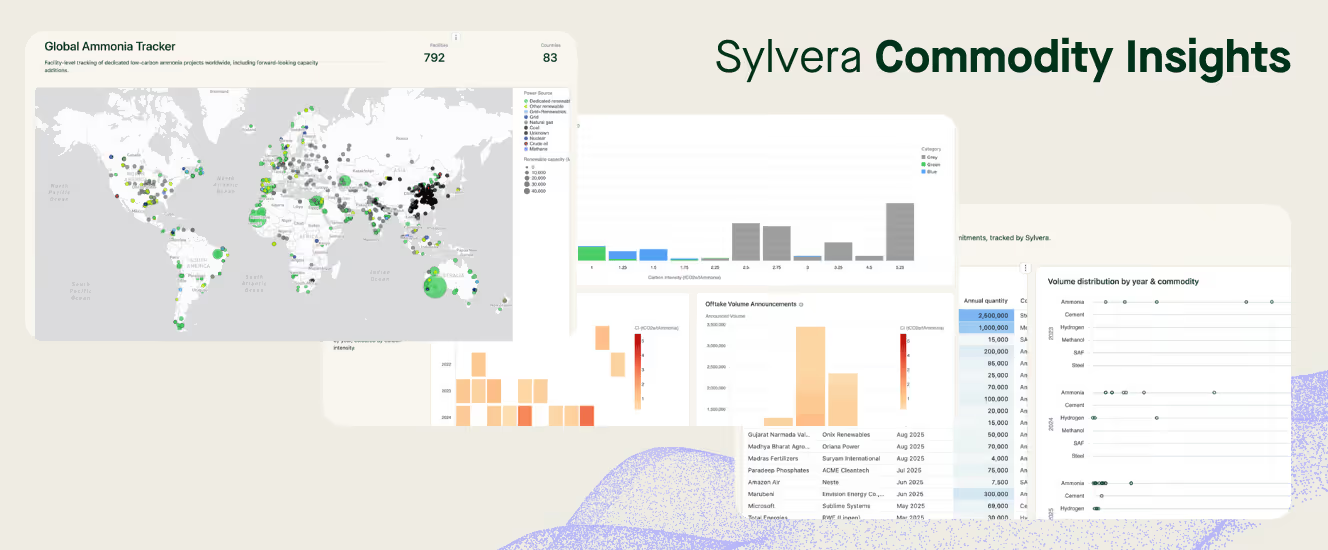

Sylvera works with producers, buyers, and investors to unlock the carbon-differentiated commodity market by providing:

- Commodity insights and market data to understand offtake dynamics, capacity, and strategic positioning.

- Standardised, facility-level carbon intensity assessments so producers can benchmark and showcase performance, and buyers can optimise procurement.

- Mechanism Eligibility & Value Assessment helping producers understand exactly which schemes their facility qualifies for, and what that's worth commercially. Get a clear, auditable answer across CBAM, LCFS, EACs, and more, with a market-priced value estimate per mechanism.

Carbon-differentiated commodities are no longer a niche concept. They are becoming the backbone of how decarbonisation is financed across the real economy.

If you’d like to explore this data in more detail, you can create a free account here.

.png)