「私たちは長年にわたり、信頼できる格付けの提供に注力し、現地データチームへの投資を重ねてきました。これにより当社の格付けの正確性は確保されていますが、購入者が検討している数千のプロジェクトにわたるスケールを実現することはできません。」

カーボンクレジット調達の最新動向について詳しくは、当社の記事「Key Takeaways for 2025」をご覧ください。調達戦略を改善するための、データに基づく5つのヒントをご紹介しています。

加えて:Connect to Supplyをご利用のお客様は、Sylveraのその他のツールもご利用いただけます。プロジェクトの格付け確認や強みの評価、高品質なカーボンクレジットの調達に加え、プロジェクトの進捗状況のモニタリング(特に発行前段階で投資している場合)も可能です。

Sylveraの無料デモを予約して、調達機能やレポーティング機能を体験しましょう。

価格、品質、需要動向に関する最新情報を詳しくご確認いただくには、当社の包括的な カーボンクレジットの現状レポートをご覧ください。

高級カーボンクレジット 価格が最高値を更新、退職者が堅調に推移

自主的な炭素市場は2025年第3四半期も安定的に推移し、償還は堅調に推移、発行は前四半期に比べ若干減少しました。これと並行して、当社の価格設定と買い手の洞察は、品質への注目の高まりと企業需要の進化パターンを指摘しています。

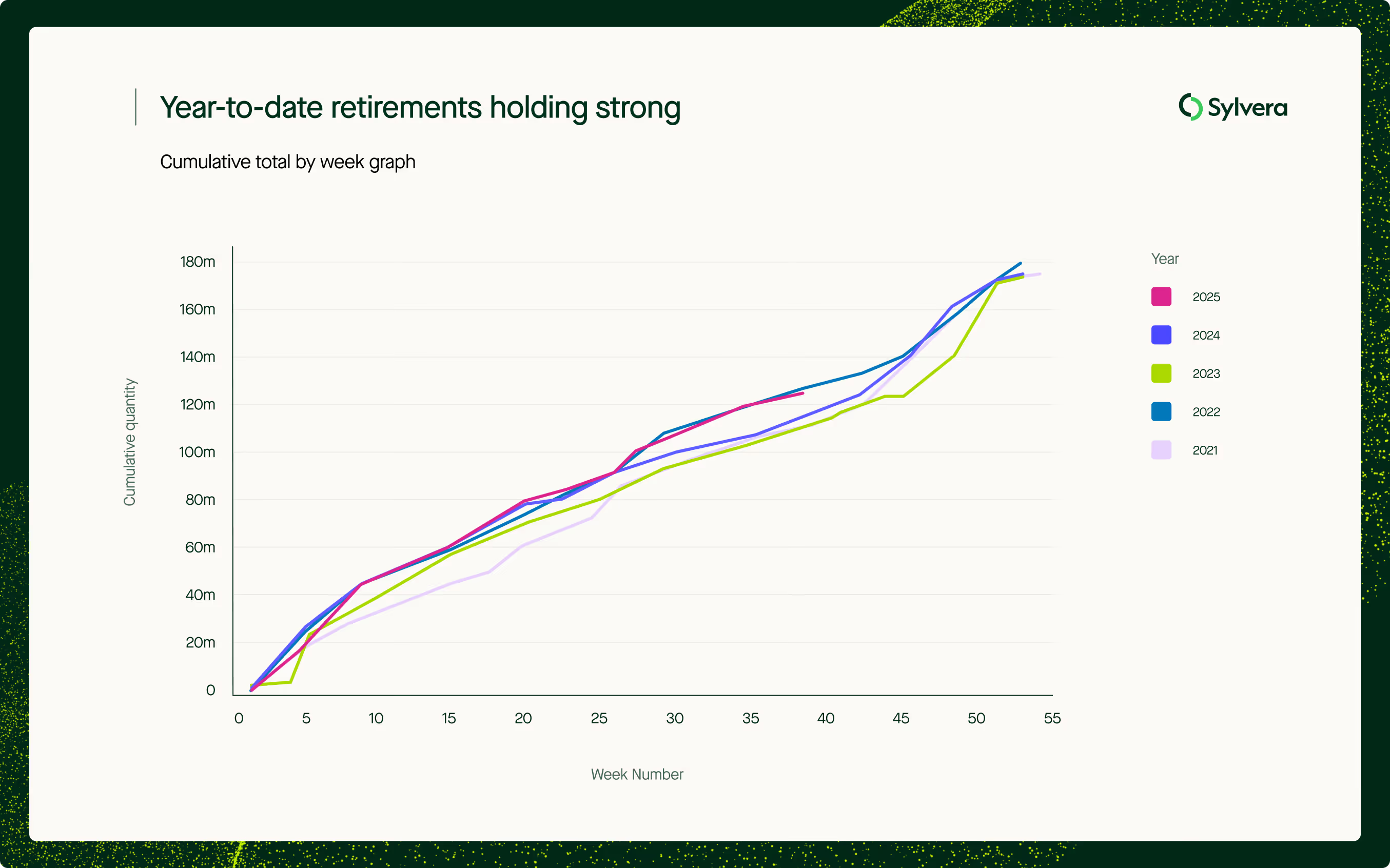

クレジットを使用して排出量をオフセットし、永久に取引できなくするプロセスである償却は、第3四半期に3,354万件に達しました。これは、過去最高を記録した第2四半期の4,045万クレジットから減少したものの、2024年第3四半期の3,149万クレジットとほぼ同水準であり、2025年の総消却量は過去最高に近づいています。2025年通年の退役は1億2,815万クレジットで、2024年第3四半期末の1億2,061万クレジットから増加し、この時点で1億3,242万クレジットを示した記録的な退役年である2022年に僅かに遅れをとっています。

供給面では、新規クレジットの発行は、 第2四半期の7,690万件、前年同期の6,880万件から減少し、当四半期は7,040万件となりました。

品質に対するプレミアムを示す価格シグナル

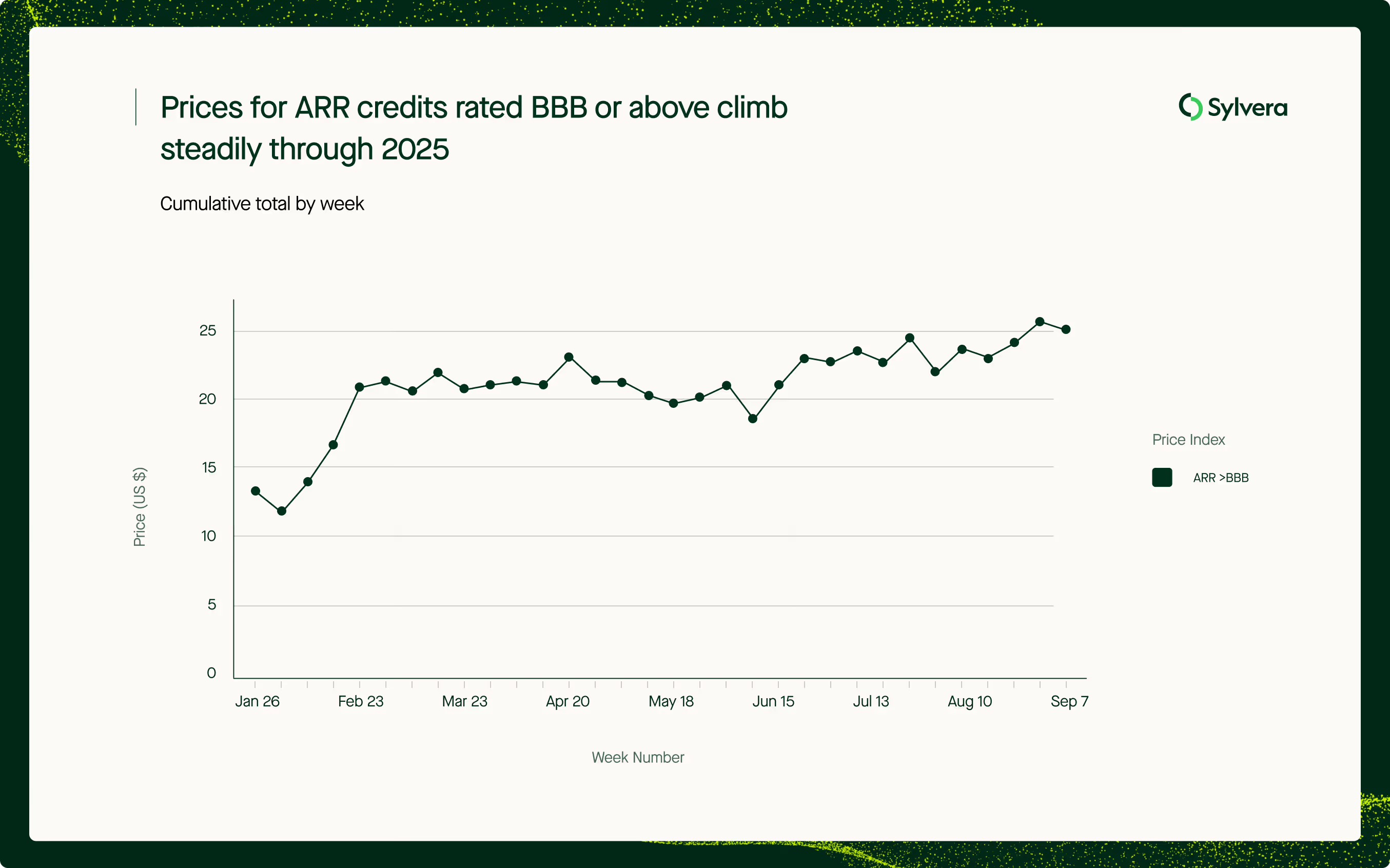

当社の新しい品質加重価格指数は、より品質の高いARR(植林、森林再生、緑化)クレジットに明確なプレミアムが生じていることを明らかにしています。BBB格以上のARRクレジットの価格は2025年を通して着実に上昇し、9月には年初から10ドル上昇して24ドルに達しました。

Sylveraプロダクト・ディレクター、Aaron Tamこう説明:「ARR価格の上昇は、買い手の優先順位の明確な変化を反映しています。TISTプロジェクトや、より厳格な新しい方法論を採用したプロジェクトなど、質の高いプロジェクトの市場参入が増え、平均価格が上昇しています。このような価格での需要が見られるということは、買い手が、完全性と実証済みの気候変動への影響にプレミアムを支払うことを望むようになり、これらのプロジェクトをより確実で長期的な投資と見なすようになっていることを示唆しています。

現在の市場のスポット価格だけでなく、ARRクレジットの将来価格も堅調で、一部のデベロッパーは次期ヴィンテージのフォワード価格を50米ドル以上と見積もっており、自然ベースの除去プロジェクトに対する旺盛な需要を示しています。

企業の嗜好の変化を浮き彫りにするバイヤーの動向

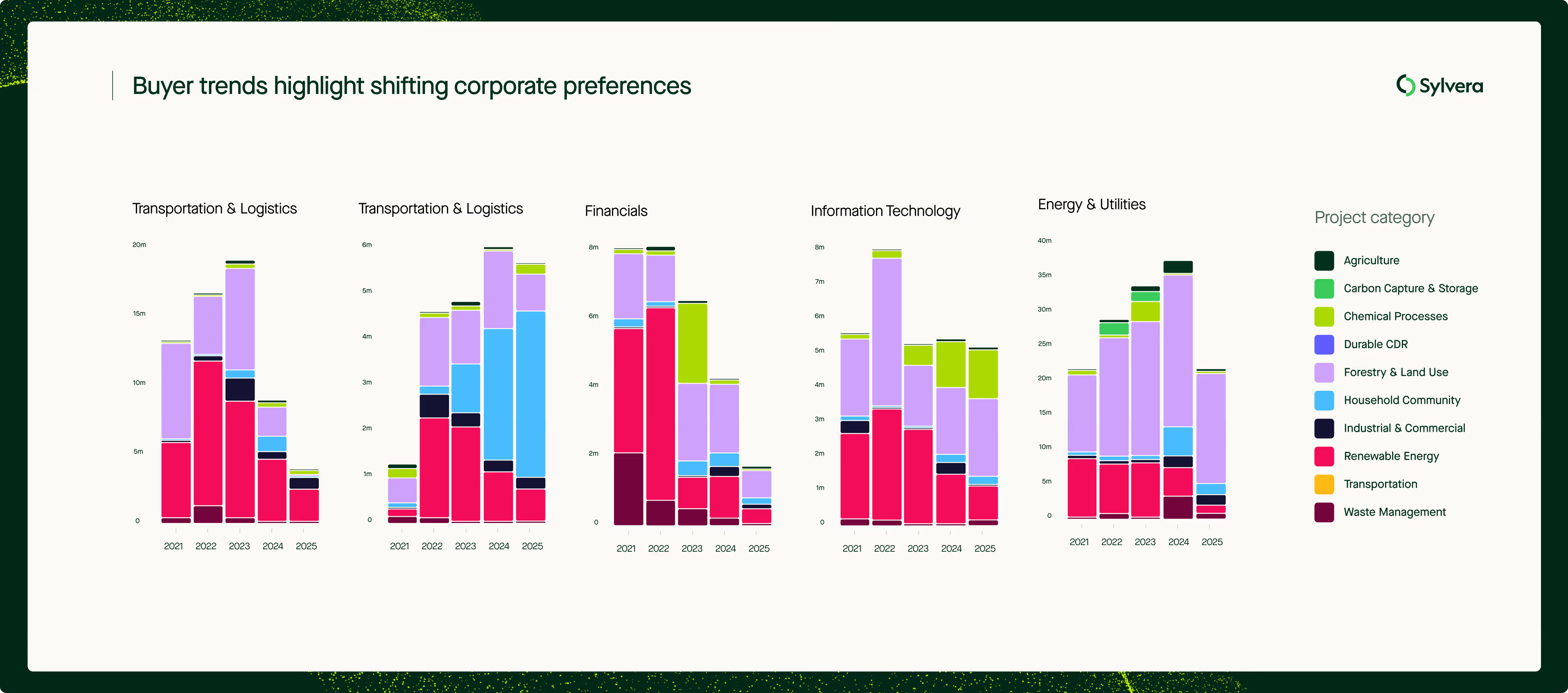

一方、Sylvera バイヤー・ディレクトリーでは、さまざまなセクターがカーボンクレジット 購入にどのように取り組んでいるか、顕著なシフトが見られます。2025年における最新の償却状況を見ると、専門サービス企業は調理用ストーブプロジェクトからのカーボン・クレジットの利用を加速させており、現在ではこのセクターの既知の償却状況の約70%を占めています。再生可能エネルギー炭素クレジットの利用は、ほとんどのセクターで着実に減少を続け、テクノロジー、金融、専門サービス企業で最も大きく減少。運輸・ロジスティクス企業は、この傾向の例外として際立っており、再生可能エネルギー炭素クレジットは依然として需要の60%を占めています。

企業の気候変動に対するコミットメントが後退しているとの認識にもかかわらず、エネルギーおよび公益事業会社は引き続き炭素クレジットの需要を支配しており、2025年の非匿名退職の40%近くを占め、昨年と同程度です。

レジストリとプロジェクト・タイプはリバランシングを参照

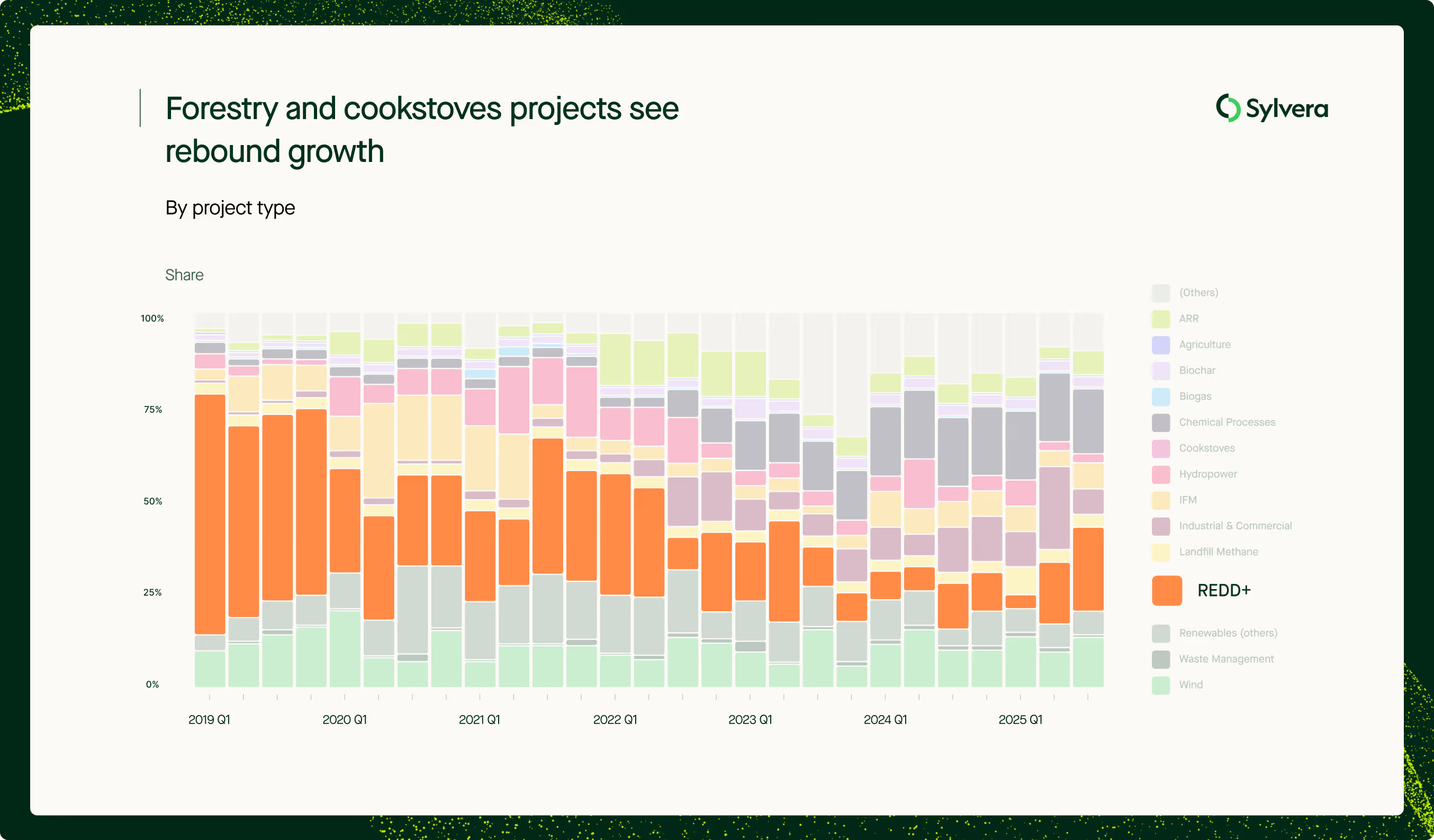

新規発行に占めるVerraのシェアは長期的に低下し続けており、2025年第3四半期には28.09%に低下しました(2年前の同期間は39.2%)。これはVerraのREDD+プロジェクト発行が2021年にピークを迎えて以来、減速が続いていることを反映しています。これとは対照的に、バイオカーボンスタンダードのシェアは21.16%と過去最高を記録しました。

第 3 四半期は林業プロジェクトからの発行が好調。特にREDD+プロジェクトは大きく回復し、発行額の26.05%を占めました(第2四半期は16%、昨年第3四半期はわずか10%)。これは、方法論の強化、モニタリングの改善、会計や追加性に関する以前の懸念に対応したより厳格な基準により、全体的な品質が向上しているこのプロジェクトタイプに対する買い手の信頼が向上していることを示唆しています。

コンプライアンス対応クレジットの普及

CCPラベル付きクレジット(ボランタリーカーボン市場整合性協議会のコア・カーボン原則に沿ったクレジット)の発行量は増加の一途をたどっています。2025年現在、1,663万クレジットがCCP承認ラベル付きで発行されており、品質と完全性の公認基準へのシフトを浮き彫りにしています。

一方、コンプライアンス市場とボランタリーシステムとの統合はますます進んでいます。今年発行された合計6,717万クレジットは、ホスト国の認可を受けることを条件として、 CORSIA第1フェーズで使用が承認された規格および方法論に属するものです。これは今期発行されたクレジット総数の3分の1(33.3%)に相当し、2年前の同時期の27.1%から増加しています。

最終四半期の市場見通し

第3四半期のデータは、市場がより成熟し洗練されたものに移行していることを示唆しています。価格の上昇と信頼できるプロジェクトに対する企業の需要の両方を通じて、品質はますます報われるようになっています。CORSIA ようなコンプライアンス制度が自主市場と規制市場のギャップを縮める一方で、買い手は保証と完全性を求めるため、レジストリは多様化しています。

SylveraAllister Furey最高経営責任者(CEO)は、次のように述べています:「高品質なクレジットに対するプレミアムの高まりは、誠実さが今や価値の重要な原動力となっていることを示しています。バイヤーはより選択的になり、プロジェクト開発者はより高い基準を満たすことで対応しています。

このように、品質に対する期待と市場の需要が一致することは、炭素市場を拡大し、より低い経済コストで真の気候変動効果を実現するために不可欠です。

2025年が最終四半期を迎えるにあたり、これらの傾向は、透明性、信頼性、コンプライアンス態勢を中核として、量だけでなく、市場が成熟しつつあることを示しています。

このような市場力学をご自身で調査したいとお考えですか?

当社のマーケット・インテリジェンス・スイートは、リアルタイムの価格、需給データにより、市場全体の透明性を提供します。

💲価格データ -~300,000件の取引による20,000件以上の見積もりからなる、プロジェクトレベルのスポット見積もり。

📈市場データ - 毎週の発行と償還、フィルタリング可能な平均価格、既知の供給統合。

🏢 バイヤー・ディレクトリー- 需要を検証するために、セクター、タイプ、ヴィンテージ、地域別に誰が何を引退させているかを確認できます。

マーケットインテリジェンスの詳細については、こちらをご覧ください。

価格、品質、需要動向に関する最新情報を詳しくご確認いただくには、当社の包括的な カーボンクレジットの現状レポートをご覧ください。