“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

Reports emerged last week that Microsoft would pause all CDR purchases. The company has since responded, saying that its carbon removal program will continue to form part of its strategy to achieve its climate goals, but it may adjust the pace or volume of carbon removal procurement.

For a CDR market already navigating fragile demand dynamics and unproven commercial models at scale, this would be a major development, and the consequences of a pause or reduction would be felt across the industry.

Our analysis aims to break down Microsoft’s commitments to date, and the potential impact of this move - if true - on the market.

The scale of Microsoft's CDR commitments

Microsoft accounts for 74% of all known CDR offtake commitments - $14.8bn out of a total $20bn committed globally.

In terms of volume, Sylvera estimates that Microsoft's existing offtake agreements were due to deliver around 85 million CDR credits, each representing 1 tonne of CO2, through 2040, at an average price of approximately $130 per tonne. This is equivalent to the average annual emissions of around 21 million people in the UK, almost a third of the total population.

See a deeper breakdown of the offtake market in Sylvera's State of Carbon Credits report here.

In the broader durable CDR market, Microsoft is responsible for all ten of the deals exceeding one million tonnes contracted: 100% of the mega-deal segment.

At the other end of the scale, it accounts for just 17% of deals under 500 tonnes.

This is important. Change in Microsoft's activity would likely hit the large-scale, capital-intensive end of the CDR market hardest. Those are precisely the projects that were counting on long-term offtake certainty to access project finance.

Why this, and why now?

Though surprising in its abruptness, a pause or slowdown would not be, in the broader sweep, difficult to understand.

Microsoft has been by far the CDR market's most ambitious participant. And the conditions that justified the position have shifted considerably.

Microsoft committed in 2020 to halving its absolute emissions by 2030, and achieving net negative status by offsetting the remainder through CDR purchases. At the time, this was a bold and credible strategy.

But three things have happened since.

- The company's emissions have not fallen. They have risen significantly, driven by the explosive growth in AI infrastructure and the energy-hungry data centres required to support it.

- As a consequence, the cost of the CDR portfolio required to deliver on the original ambition has become very large, material even by the standards of a company of Microsoft's scale, especially as capital expenditure is already squeezing margins.

- The US went from being one of the most pro-CDR markets under President Biden to being much more sceptical of climate action in general under President Trump, curtailing investor confidence and hence increasing the likely cost of future CDR credits.

Immediate market implications

The short-term implications for the CDR market would be major. CDR developers that have not yet secured offtakes could find themselves competing for buyers in a weaker demand environment than they had been planning for.

The pipeline of willing, large-scale buyers is thin, and a Microsoft pause or reduction removes both capital and confidence from the market simultaneously.

Prices are likely to soften — particularly in technology-based CDR, where Microsoft is especially prominent relative to other buyers. Projects in the early stages of fundraising or at final investment decision that were counting on Microsoft's participation face the sharpest near-term risk.

BECCS (bioenergy with carbon capture and storage) projects face disproportionate exposure. With 100% of all Microsoft contracted deals exceeding one million tonnes — data from CDR.fyi published in April 2026 shows how this segment that maps closely to large-scale BECCS. Smaller-format project types, including biochar and DACCS, will face pressure, but are less reliant on single mega-offtakers.

.avif)

Would other major buyers follow?

This is the question that matters most for the market's trajectory. Microsoft is the most prominent CDR buyer, but it is not the only one facing mounting pressure between net zero commitments and rising emissions baselines.

Meta, Alphabet, JPMorgan Chase, and Amazon all appear in the top twenty CDR offtakers. Several operate in industries where the tension between operational growth and stated climate targets is intensifying.

Top 20 CDR offtakers:

It would be premature to conclude that any Microsoft change would signal an industry-wide retreat. Many other buyers have significantly smaller and more manageable portfolios, and just last week JPMorgan announced a sizeable new CDR deal. But it would highlight how voluntary CDR commitments are subject to commercial and strategic review in a way that regulated compliance obligations are not.

It suggests developers would be wise to consider diversifying across buyer types, including compliance buyers and government programmes, rather than relying on a small number of large voluntary commitments from the technology sector.

The long-term case remains intact

Regardless of any Microsoft pause or slowdown, the structural case for CDR demand remains: many companies see a clear role for carbon removals to address remaining emissions as they progress towards net zero targets.

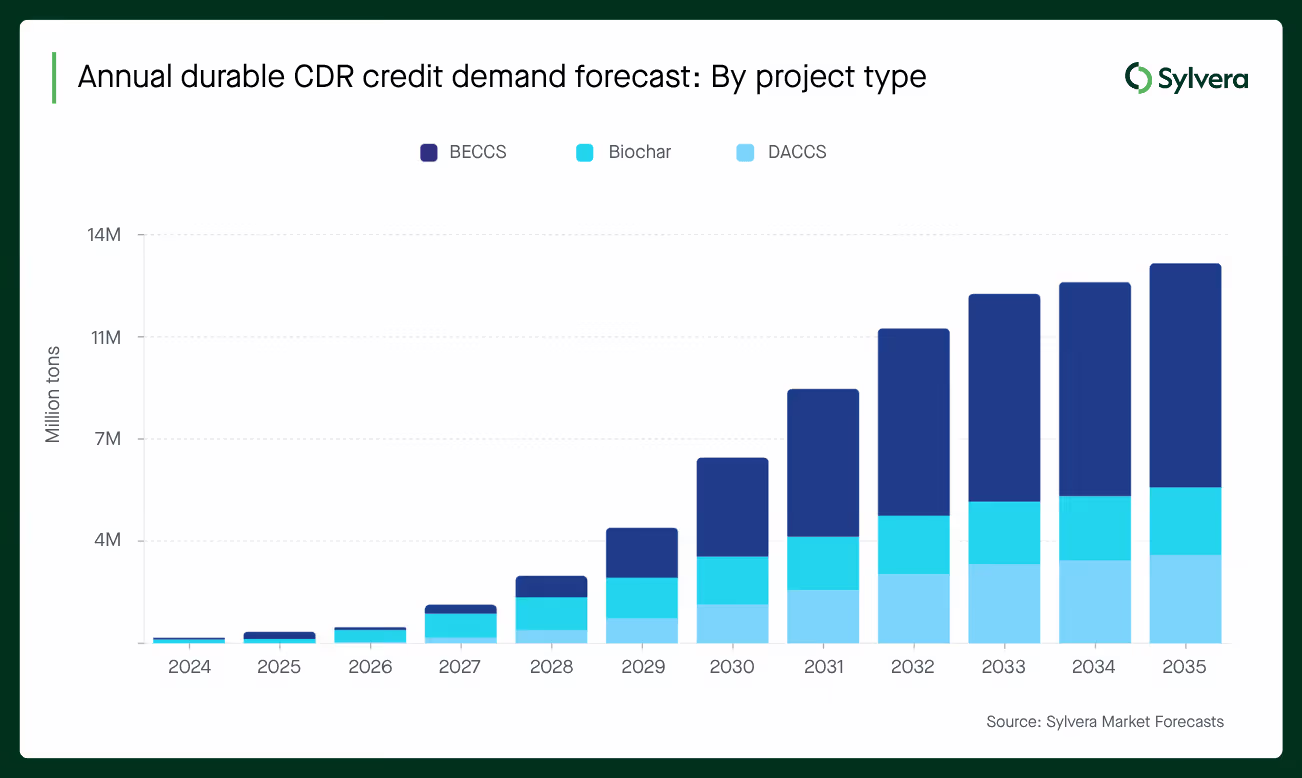

Sylvera's Market Forecasts show that demand volumes for durable CDR will continue to grow through 2035. Although Microsoft’s offtakes represent a large part of that demand, there is still room for growth as other buyers step in with further purchases.

For developers with robust projects and credible delivery records, any change in activity by Microsoft may ultimately accelerate rather than delay revenue diversification.

The need for high-quality carbon markets continues to grow, as corporates and governments alike seek to decarbonise at least cost. CDR will play a growing role in that mix. But the market is learning an important lesson about concentration risk.

Sylvera will continue to track pricing, volume, and buyer activity across CDR segments as this situation develops.