.png)

“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

Japan is the world's fourth-largest economy and one of its most emissions-intensive — anchored by automotive, iron and steel, chemicals, power, oil and gas, and shipping. It is also one of the most consequential carbon markets to understand in 2026.

In April 2026, Japan's GX-ETS officially launched. Registration and transition plans are due in September 2026. The first allowances will be allocated in April 2027, with trading opening in Q3 of the same year. Layered on top, Japanese corporates are navigating two domestic crediting schemes — J-Credit and JCM — alongside the global voluntary carbon market (VCM).

It's a lot to absorb, especially for buyers who haven't yet built a procurement function. This article unpacks how Japan's carbon market actually works today, where the supply and demand sit, and the practical steps corporate teams should be taking before mandatory pressure arrives.

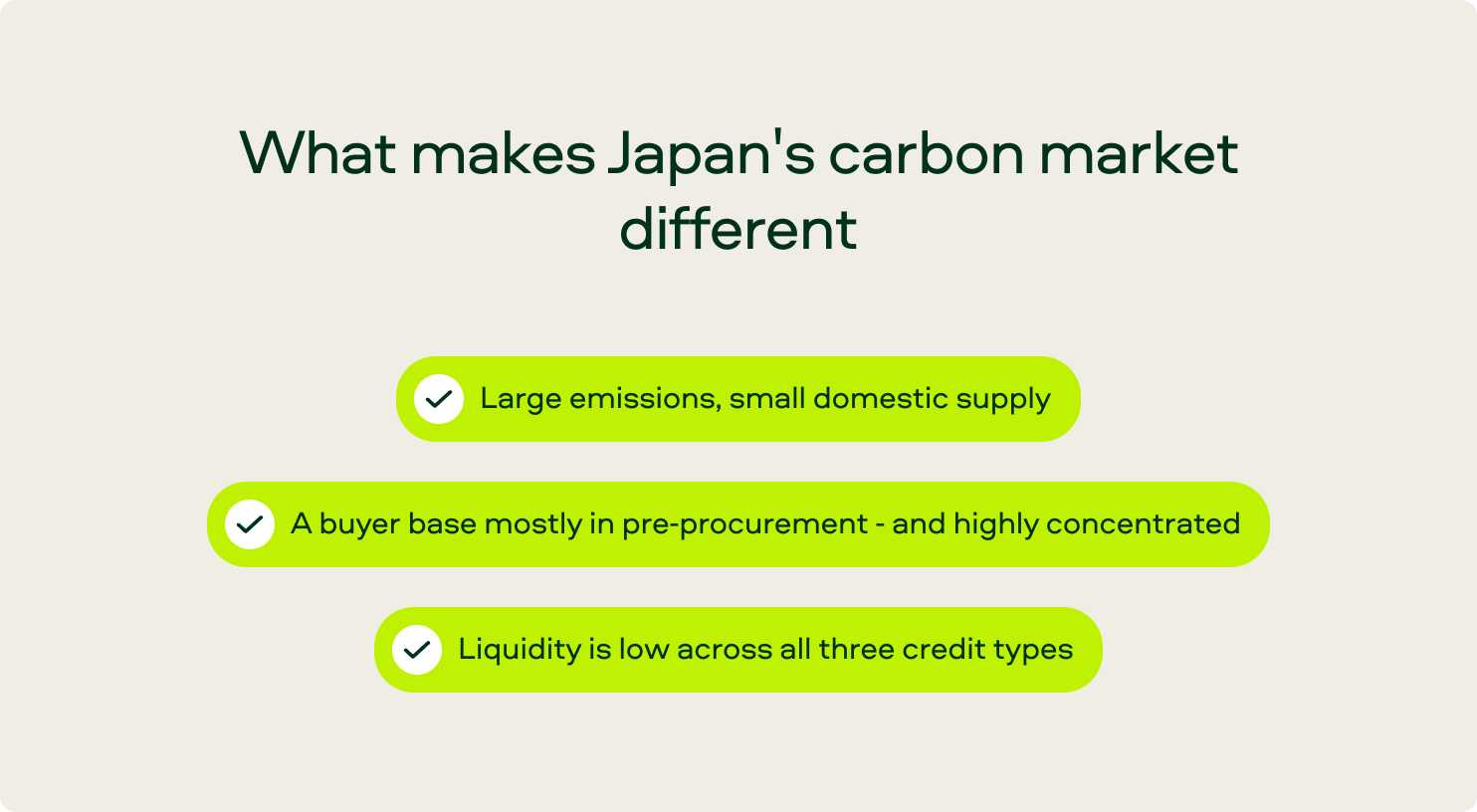

What makes Japan's carbon market different

Most APAC carbon market analyses lump the region into a single bucket. That misses the specific shape of Japan — and the shape is what drives every procurement decision worth making.

Large emissions, small domestic supply. Japan's economy is dominated by hard-to-abate sectors with serious 2030 and 2050 carbon neutrality commitments, many tied to SBTi targets. But the country's land base is small and densely used, which means the domestic developer ecosystem is limited. There are no global-scale VCM developers headquartered in Japan, and J-Credit projects tend to be small in size and high in count.

"Japan is having lots of manufacturing companies, big oil companies, energy companies, electric companies — hard-to-abate companies. So they are considering carbon neutrality seriously in their business plans. On the other hand, the developer count is very limited, because Japan itself is a small country with small land." — Yuki Katsumura, Head of Japan and Korea Business, Sylvera

A buyer base mostly in pre-procurement - and highly concentrated. This is the single most important pattern. Of the ~27 million credits retired by Japanese buyers in Sylvera's dataset, just two companies — Takeda Pharmaceutical (11.1M) and Yamato Transport (6.9M) — account for the majority. The top seven buyers collectively represent the overwhelming bulk of all Japanese retirement volume.

The majority of Japanese corporate buyers do not yet have a defined carbon credit procurement plan. They are researching, comparing, and trying to understand the process — not yet transacting at scale. Only a small number of fast-moving companies have started buying proactively, and only a few have disclosed procurement activity without retirement timing.

Liquidity is low across all three credit types. Because there's no mandatory trigger to retire credits today, J-Credit, JCM, and VCM all see thin trading from Japanese buyers. That changes once GX-ETS allowance allocations land in 2027 and a compliance charge mechanism kicks in for high-emission firms.

Put together, these three patterns explain the rest of the article. The Japanese market is growing relatively fast, but remains thin. Sylvera data shows Japanese buyer retirements surged from just ~58,000 credits in 2018 to 6.4 million in 2023 — a more than 100-fold increase in five years. Yet the number of unique buyers active in 2024 was only 38.

Demand is real but latent. Supply is constrained and quality-variable. And the window to prepare without competing for inventory is shorter than most buyers assume.

The three types of carbon credits Japanese companies can use

Understanding Japan's market starts with separating the three credit categories Japanese buyers can transact in. They sit in different parts of the system and behave differently.

J-Credit

J-Credit is Japan's domestic crediting scheme. Only Japanese companies can develop J-Credit projects, and only within Japan. The most common project type is forestry — primarily improved forest management (IFM) equivalents — alongside renewable energy and energy efficiency.

Project sizes are small, but there are many of them. That makes J-Credit a useful monetization route for unused forestry, agricultural land, and small renewables, and it has become a standard tool for corporate offset narratives inside Japan. It isn't a globally interoperable credit, but it is the most accessible domestic option.

JCM (Joint Crediting Mechanism)

JCM is Japan's bilateral mechanism for generating credits in partner countries. With the closure of the Kyoto-era Clean Development Mechanism (CDM) confirmed at COP30, JCM is increasingly treated as Japan's Article 6.2 vehicle — a way to source international mitigation outcomes with corresponding adjustments.

In practice, JCM is still in an early-issuance phase. Developers and investors are building project pipelines, but very few credits have actually been issued. Among projects in development, agricultural waste destruction (AWD) and renewables are the most common types. Availability is limited, and that constraint is likely to persist for the next 18–24 months.

VCM (Voluntary Carbon Market) credits

Japanese buyers also use credits from the global VCM — Verra, Gold Standard, Puro, Isometric, and others. Renewables have historically been the most common VCM purchase type from Japanese buyers - with wind, hydro, and other renewables accounting for approximately 13 million of Japanese retirements in Sylvera's dataset — roughly half of all volume. hat mix is shifting as compliance pressure and SBTi guidance push companies toward removals and higher-integrity nature-based projects. REDD+ is the single largest individual project type at 7.0 million credits, followed by industrial and commercial projects at 4.2 million and ARR at 1.5 million — a meaningful signal of growing nature-based interest.

And geographically, Japanese buyers source overwhelmingly from Asia. India is the top supply country by volume at 7.1 million credits across 103 projects, followed closely by China at 5.5 million across 76 projects. Together, India and China account for approximately 46% of all credits bought by Japanese companies — a distinctive feature of Japanese procurement compared to European or North American buyer bases. is currently no mandatory reason for Japanese corporates to procure VCM credits, which is the central structural fact about voluntary demand in Japan today.

"As a voluntary perspective, there is no reason to buy and purchase credits now. Companies are setting carbon neutrality goals proactively, but they don't have a concrete plan for how to fill the hard-to-abate part. So lots of buy-side clients are still at the early stage — market research, not procurement." — Yuki Katsumura

GX-ETS: the compliance trigger that changes the picture

Everything described so far runs on voluntary motivation. GX-ETS changes that. It's the most significant structural shift to Japan's carbon market in a decade — and it moves the country from a purely voluntary system to a hybrid model with real compliance demand.

How it works

GX-ETS is a cap-and-trade system. Companies receive allowances for permitted emissions. If a company emits less than its limit, it can sell the surplus. If it emits more, it must buy additional allowances or pay a compliance charge. It's the same logic as the EU ETS, but designed around Japan's preferred policy framing of "growth-oriented carbon pricing" — the government wants to support transition spending, not simply penalize emissions from day one.

The timeline that matters

- April 2026: GX-ETS officially launches.

- September 2026: Registration and transition plan submission deadline for in-scope companies.

- April 2027: First allowance allocations published.

- Q3 2027: Trading opens.

Who is in scope

GX-ETS becomes mandatory for large emitters — companies with annual direct emissions above 100,000 tonnes of CO₂. That includes the bulk of Japan's hard-to-abate base: automotive, iron and steel, cement, oil refining, chemicals, power, and large manufacturing. If you're a sustainability or finance lead at a Japanese corporate with material direct emissions, the question isn't whether GX-ETS affects you, but how much.

How domestic credits interact with GX-ETS

J-Credit and JCM credits are expected to be usable within GX-ETS compliance, subject to qualitative requirements that haven't yet been finalized. The direction of travel is clear, though: as the scheme matures, quality requirements will tighten, and credits without robust documentation, additionality evidence, or eligibility against frameworks like CORSIA and CCP will face increasing scrutiny.

The "wait for the cap" trap

There's a logic that's become common in Japanese corporate sustainability teams in 2026:

- Specific allowance caps won't be published until April 2027.

- Without a cap, we can't model our exposure.

- Without modeled exposure, we can't build a procurement plan.

- Without a procurement plan, we can't get a budget approved.

- So we'll wait.

It's understandable logic, but it carries real risk. Three forces are tightening the high-quality credit market regardless of when individual Japanese caps are set:

.png)

1. Quality premiums are widening, not stabilizing

In Sylvera's State of Carbon Credits data, high-quality (BB+ and above) credits grew from 44% to 50% of retirements globally — and from 61% to 70% of total spend. High-rated ARR projects are trading above $35 per tonne while lower-rated equivalents sit below $20. Companies that lock in quality early lock in better prices.

2. Compliance demand is converging with voluntary supply

Compliance programs already accounted for 24% of 2025 retirements globally, and Sylvera modeling projects they will exceed voluntary demand by 2027 — driven by CORSIA Phase 1 and expanding domestic systems including GX-ETS. Compliance and voluntary buyers will be competing for the same high-quality inventory.

3. CORSIA Phase 1 is becoming a de facto quality floor

Japan Airlines retired 235,000 CORSIA-eligible credits in Q1 2026 — an early signal of compliance activity from a Japanese major. As aviation demand scales globally, CORSIA-eligible inventory will face sustained drawdown.

Waiting for the GX-ETS cap to land is, in effect, betting that the market will be cheaper and better-supplied in 18 months than it is today. The data points the other way.

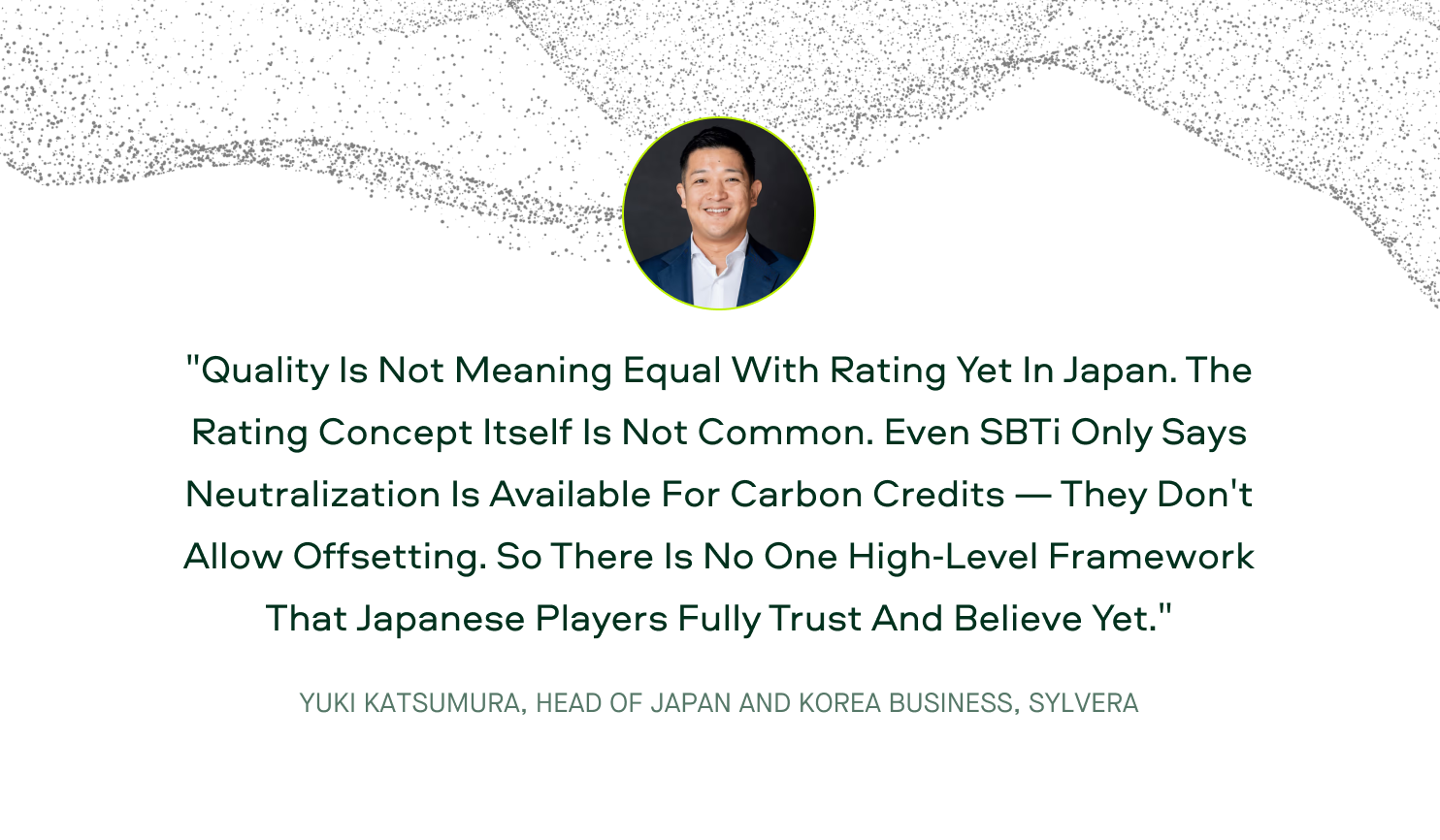

Why quality is the unfinished conversation in Japan

In financial markets, ratings are anchored in law. Credit ratings, ESG ratings, and structured-product ratings have well-established roles in accounting, disclosure, and regulatory frameworks. That's why they're trusted by default.

Carbon credit ratings don't yet have that institutional gravity in Japan. The result is a buyer base that often defaults to a mix of high-level guidelines — ISO 14064, the Core Carbon Principles (CCP), CORSIA eligibility, SBTi guidance, the Act on Promotion of Global Warming Countermeasures — without a single internal framework for deciding what "good" looks like.

"Quality is not meaning equal with rating yet in Japan. The rating concept itself is not common. Even SBTi only says neutralization is available for carbon credits — they don't allow offsetting. So there is no one high-level framework that Japanese players fully trust and believe yet." — Yuki Katsumura

Sylvera’s data shows this pattern. Of approximately 27 million credits retired by Japanese buyers, around 45% comes from unrated projects. Of the rated volume, the largest buckets sit at the bottom of the quality spectrum: 4.8 million credits at D-rating and 3.6 million credits at C-rating. Credits rated BBB or above - widely acknowledged as investment-grade - account for only around 13% of total retired volume. The AA bucket, at 3 million tCO₂, is driven almost entirely by just four projects, large-scale purchases by a single buyer.

This isn't a criticism — it's a market maturity observation that Japanese sustainability leads will recognize. But it creates a specific procurement risk: credits that look acceptable today may not meet tomorrow's compliance requirements, audit standards under tightening disclosure frameworks (ISSB, CSRD equivalents), or SBTi's evolving removal-based criteria for net zero claims.

What quality actually means

Independent of any rating provider, four dimensions matter:

- Carbon accounting: Is the tonne actually a tonne? Are baselines defensible and measurement methods accurate?

- Additionality: Would the climate benefit have happened anyway without the credit revenue?

- Permanence: How long will the carbon stay out of the atmosphere? What are the reversal risks?

- Co-benefits: What's the broader environmental and social impact beyond the tonne?

.png)

These dimensions are the basis for most serious quality assessments, including Sylvera's Ratings, CCP labelling, and ICVCM assessment. The translation to Japanese projects is direct: a J-Credit forestry project, a JCM cookstove project, and a VCM REDD+ credit can all be evaluated against the same underlying pillars.

What Japanese buyers actually care about

From Sylvera's work with corporate buyers in Japan, three preferences come up consistently in product demos and procurement conversations. They explain why the quality conversation moves slowly — and what does land.

1. Market data is the strongest hook

Japanese corporates tend to trust market data — issuance volumes, retirement patterns, pricing curves — more readily than quality scores. The reason is straightforward: data is data, and it's verifiable against multiple sources. Quality frameworks require additional context to interpret.

.png)

"Japanese companies tend to believe market data more than rating quality. That's why the strongest hook for us is market intelligence — and price forecasting in particular. The data is data, so they can trust it as a real data source." — Yuki Katsumura

2. Price forecasting is the second hook

Both buy-side and sell-side teams in Japan use forward pricing data. Buyers use it to justify procurement decisions internally — proving that a transaction was executed in a defensible price range. Sellers use it to argue that prices for high-quality project types are moving upward, supporting today's pricing in commercial conversations.

3. Quality understanding is still being built

Quality conversations happen, but they are often shallow on the first pass. Japanese buyers will engage with explanations of how Sylvera assesses additionality, permanence, carbon accounting, and co-benefits — but many haven't yet built the internal context to evaluate why those pillars matter for their specific procurement decisions. This is the educational gap the market needs to close.

.png)

A useful pattern to watch: when ratings and market data are presented together, ratings start to register as a real signal rather than an abstract score. Buyers see what a high rating costs versus a low one, and the financial case for quality becomes concrete.

Three things Japanese buyers should be doing now

None of this requires waiting for GX-ETS caps. All three actions are feasible in the next 90 days, and each one compounds over time.

1. Map your likely emissions exposure

If your company is in the 100kt+ direct emissions range, identify the facilities and processes that will fall under GX-ETS scope. Estimate a likely allowance position even without final caps — most companies can build a directionally accurate model from internal emissions inventory data. The point isn't precision; it's having a number to plan against.

2. Build a market data baseline before you need to transact

Track pricing across J-Credit, JCM (as it begins to issue), and the global VCM credit categories relevant to your sector. Watch the quality premium — the gap between high-rated and low-rated credits in the same project type. Sylvera’s data shows this gap is already meaningful and widening, with high-rated ARR trades above $35/tonne while lower-rated equivalents sit below $20. Understanding price movement for 18 months before you procure is the cheapest insurance available.

3. Engage sell-side suppliers early

Supply pipelines for high-quality credits are tightening globally. Building relationships with developers and intermediaries now — while competition is lower and conversations are exploratory — is dramatically easier than scrambling for inventory under compliance pressure. Sylvera's coverage of the Japanese sell-side suggests the supply community is more mature than the buyer community; that asymmetry favors buyers who engage early.

.png)

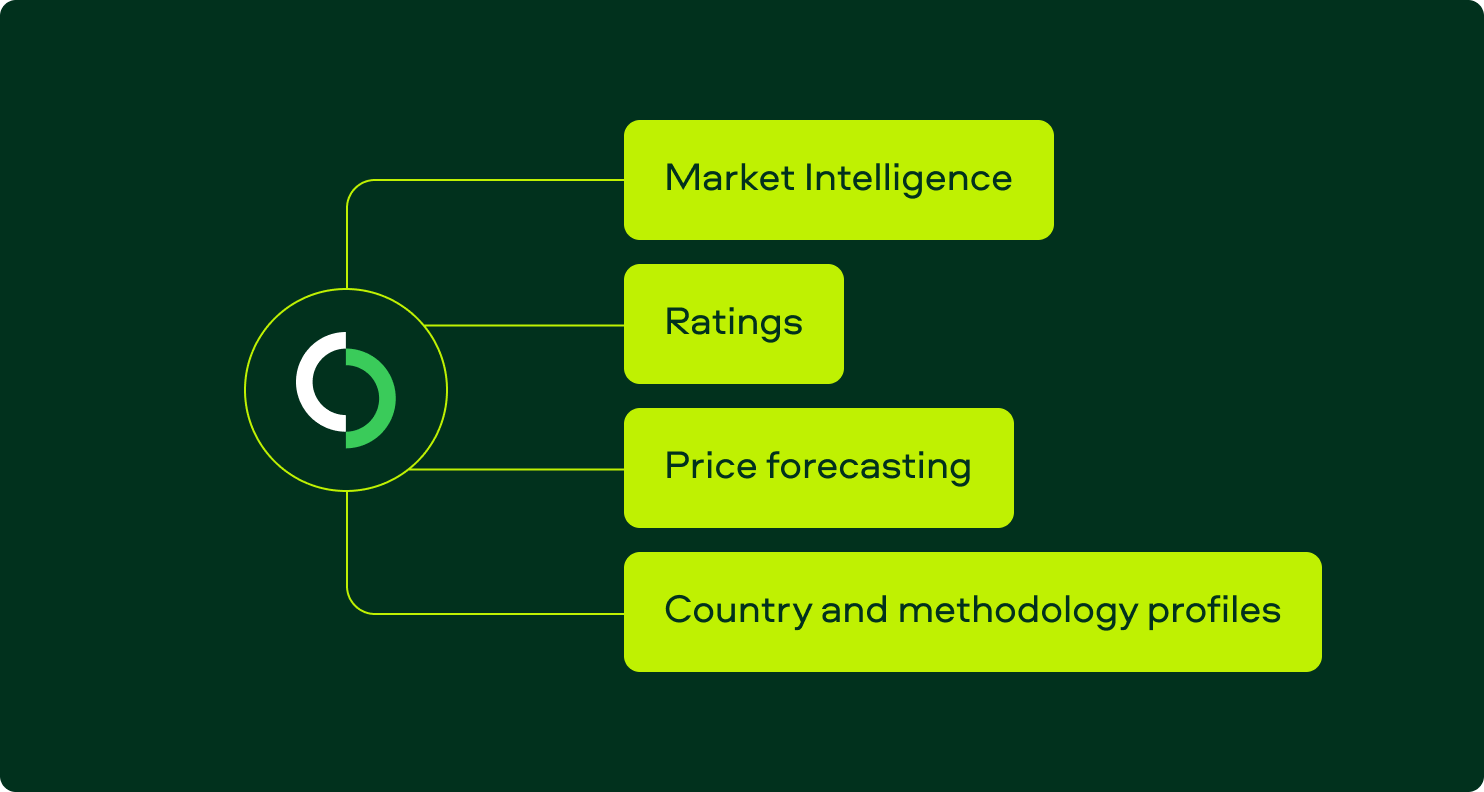

How Sylvera supports Japanese buyers

Sylvera's role in the Japan market is to provide the data infrastructure that makes carbon credit decisions defensible — internally to finance and audit teams, and externally to regulators, customers, and investors. Specifically:

Market Intelligence: Pricing, issuance, and retirement data across J-Credit, JCM, and global VCM categories, with Japan-specific buyer pattern analysis.

Ratings: Independent quality assessments across carbon accounting, additionality, permanence, and co-benefits — applicable to projects in any registry Japanese buyers transact in.

Price forecasting: Forward-looking models on credit pricing by project type, supporting procurement decisions and internal budget defenses.

Country and methodology profiles: Risk, regulatory, and supply context for the geographies Japanese buyers procure from.

To see how this applies to your portfolio, book a demo with the Sylvera team.

The next 12 months

Japan's carbon market is at the point where structure starts catching up with intent. Corporate carbon neutrality commitments have been in place for years. The infrastructure to act on them — compliance trading, domestic crediting, integrated quality frameworks — is now arriving.

The buyers who move first won't necessarily be the largest. They'll be the ones who build a market data baseline, an internal quality framework, and supplier relationships before GX-ETS forces the conversation. That preparation is genuinely cheap today and meaningfully expensive a year from now.

For Japan-specific market data, ratings, and pricing forecasts, request a Sylvera demo.