“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

Transportation electrification projects generate carbon credits by claiming the emissions avoided when vehicles switch from fossil fuels (diesel, petrol/gasoline, natural gas) to electricity - either through deploying electric vehicles (EVs) or building charging infrastructure.

Transport remains a major source of global CO2 emissions. In 2022, global transportation CO2 emissions reached 8.14 Gt CO2e - excluding aviation and shipping (an additional 1.14 Gt CO2e) - representing 14.2% of global emissions.

Meanwhile, EVs and lithium-ion batteries have gotten cheaper. BloombergNEF reports global battery pack prices fell to $115/kWh in 2024, from $715/kWh in 2014.

Many markets still face challenges to broad EV adoption. Carbon finance has become an attractive option to overcome hurdles, such as high upfront costs and limited charger availability, to improve global EV adoption.

This post excludes modal shift projects (i.e., shifting passengers from one form of transport to another), which raise different baseline and demand questions.

EV Projects Market Outlook

Electrification is emerging as a popular type of carbon project. Common methodologies include:

- EV charging infrastructure (e.g., Verra VM0038)

- EV deployment (CDM AMS-III.C, and Verra’s VMR0014 revision published July 2025)

Recent years have seen a small but significant increase in the registration of electrification projects: of 77 currently registered projects, over 80% are yet to issue credits. Numerous projects have been registered in Asia, North America, and Africa, illustrating how developers are balancing implementation in markets with low EV adoption rates, but sufficient infrastructure capacity for future adoption.

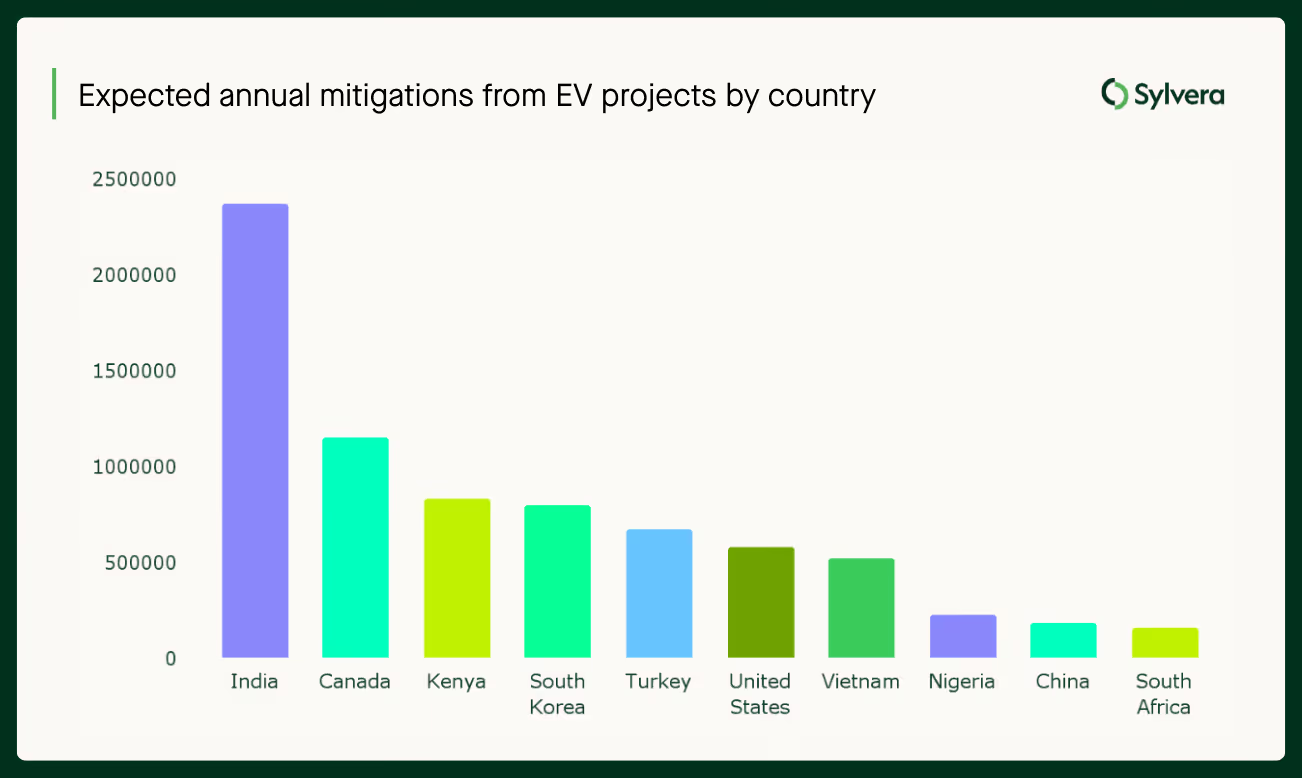

Locations of EV Projects

EV projects are also popular across Asia, Africa, and North America. India dominates the EV project landscape in terms of countries, with over double the expected annual issuance of Canada.

A milestone moment: the first-ever Article 6 ITMO issuance for NDC use

The biggest signal that electrification is becoming a serious carbon asset emerged in early January 2024, when Switzerland and Thailand completed the first transfer of Article 6.2 ITMOs for use toward a nationally determined contribution (NDC).

Read our latest Article 6 guidance here.

The mitigation activity behind that first transfer was the Bangkok E-Bus Programme, a joint charger installation and E-bus deployment programme in the Bangkok Metropolitan Area. Although the initial transaction of 1,916 ITMOs may have been insignificant when compared to national climate goals, it paves the way for electrification projects to participate in economically significant compliance markets.

While this milestone is an exciting step forward, ensuring the integrity of electrification carbon projects remains critical. The following highlights the key quality differentiators that such projects should pay close attention to.

EV Project Quality Differentiator 1 – Additionality

Transport electrification is a “moving target” for additionality: EVs are getting cheaper, and many governments actively support them through subsidies, mandates, and public procurement. That makes EV adoption genuinely impactful in some contexts, but also makes it easy for projects to look additional on paper, when the same shift would likely have happened anyway.

Methodologies often use automatic additionality thresholds based on EV penetration or sales shares. Those thresholds can quickly become outdated in fast-growing markets, creating a risk that projects continue to issue credits even after electrification has become close to business-as-usual within the crediting period.

Projects can differentiate themselves in additionality by targeting underaddressed transport markets in both sector and area, implementing cutting-edge technologies with prohibitive CAPEX, or replacing full systems rather than components. The Bangkok E-Bus Programme implements both buses and chargers, and was responsible for ~90% of e-buses in Thailand by December 2024, illustrating the ability for electrification projects to act as disruptors when implemented intelligently.

EV Project Quality Differentiator 2 – Life Cycle Assessments

Most electrification crediting focuses on tailpipe/fuel-switch emissions and often leaves out lifecycle emissions—especially from manufacturing batteries and vehicles. Even when EVs have lower lifetime emissions overall, manufactured emissions from battery EVs (BEVs) are estimated to have ~40% higher production emissions than ICEVs. Exclusion of these manufacturing emissions from carbon accounting risks overcrediting.

Manufacturing emissions of charging projects are typically of a smaller scale relative to the avoided emissions, although excluding LCA emissions still risks overcrediting. Projects can differentiate themselves by proactively performing LCAs, or including default reduction values to address built emissions that aren’t explicitly required in methodologies.

EV Project Quality Differentiator 3 – Baseline Setting

Baselines define the counterfactual scenario—what would have happened without the carbon project—so that resulting differences in emissions can be quantified. In EV projects, baseline setting often turns on a deceptively simple question: which fossil vehicle is being replaced? A common optimistic choice is comparing EVs to the “average vehicle on the road,” even though the real counterfactual for many buyers is closer to a new ICE vehicle, which is often more efficient than the fleet average.

Small baseline differences then scale into large calculation differences, particularly concerning fuel economy. Projects can differentiate themselves by choosing conservative baselines—replacement of new, fuel-efficient vehicles—and ensuring that fuel economy in baseline emissions calculations aligns with the counterfactual baseline vehicles.

EV Project Quality Differentiator 4 – Overlapping Claims

Electrification is unusually exposed to overlapping claims. A vehicle deployment project can claim avoided tailpipe emissions; a charging network can claim the same avoided tailpipe emissions from electricity dispensed; and a renewables project can claim again on the electricity side, as a carbon credit or as a renewable energy certificate. Without clear boundaries, one real-world reduction can appear multiple times across different projects.

Accommodating for this overlap requires the use of reduction factors prior to issuance - VM0038 includes one such reduction factor to accommodate EV projects, but VMR0014 & AMS-III.C have no such factor, and no methodology requires accommodating for renewables. While individual projects can adjust for overlapping claims, ensuring that no double-counting occurs requires that each project in a system appropriately adjust its issuance.

Projects attempting to limit exposure to double-counting risk comprehensively can either attempt to credit entire systems (energy supply, charging systems & EV deployment) or conservatively adjust credit issuances based on any overlapping projects.

Electrification Projects and Sylvera’s Pre-Issuance Assessment

Electrification projects offer opportunities to rapidly develop carbon projects in both established and emerging markets, supporting climate goals and local development. EV projects have unique pitfalls that should be addressed in project design to ensure integrity and success.

Through Sylvera’s platform and Pre-Issuance solution, developers can position their projects for investor confidence and compliance with market suitability, as well as connect with suppliers seeking to secure credit volumes.

Want to learn more about how Sylvera can help you navigate the electrification market?

We’d love to hear from you. Get in touch here to discuss an assessment for your project.