“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

Cement contributes about 8% of global emissions. A typical tonne of portland cement produces around 0.95 tCO2e, and roughly 60% of those emissions come not from the fuels used to heat the kiln, but from the calcination of limestone itself. Lower-carbon cement can be produced utilising various alternative materials and technologies, alongside carbon capture.

The fundamental challenge is now understanding and utilising a wave of regulatory and market mechanisms across EMEA that are putting a price on carbon. Here, we dive into five voluntary and compliance mechanisms that are either live or coming into force between 2026 and 2027.

For cement producers, the question is no longer whether carbon will affect commercial performance. It is whether you understand the mechanisms well enough to treat them as an advantage rather than a cost.

1. EU ETS: The Cost Ramp Has Started

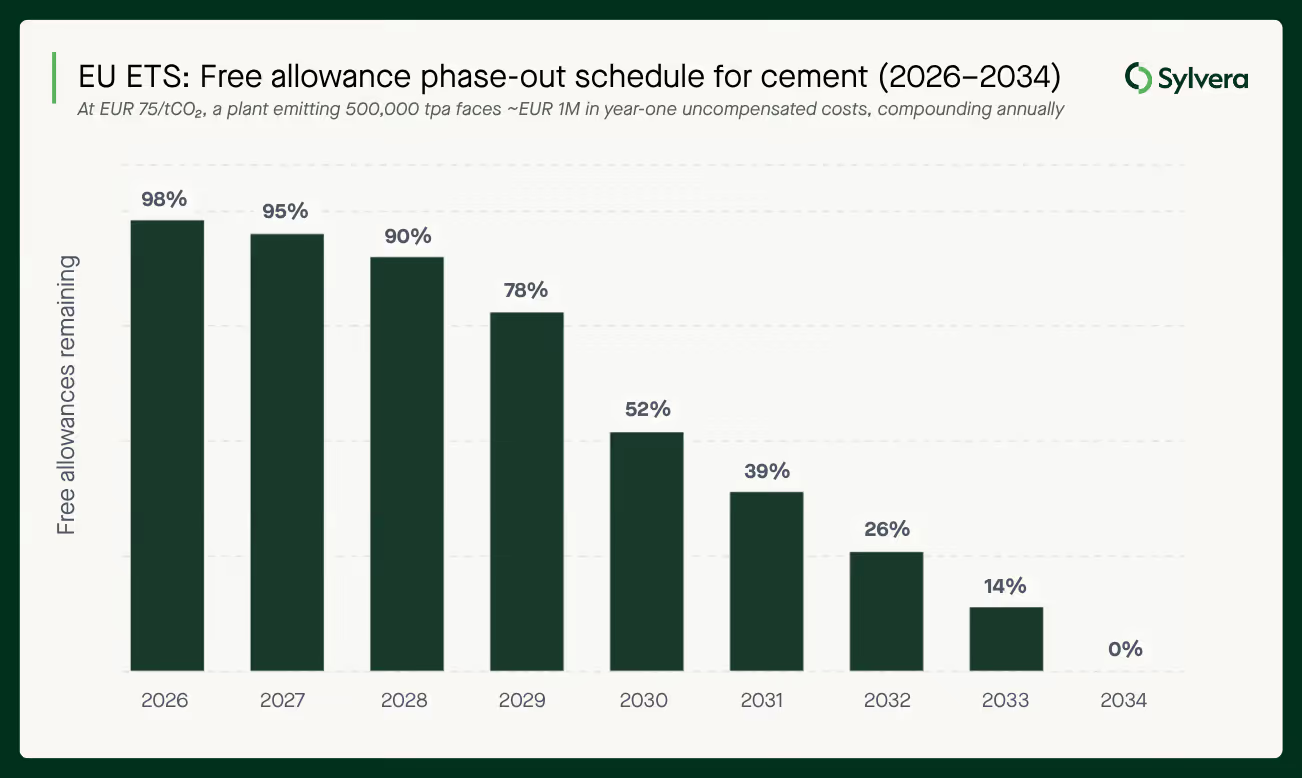

EU cement plants have operated under the Emissions Trading System for years, surrendering allowances per tonne of output. Free allowances have historically offset much of that cost. That buffer is now being removed on a legislated schedule.

From 2026, free allocations are phased out in parallel with the roll-out of CBAM, following a non-linear trajectory: the reduction factor starts at 2.5% in 2026 and reaches 100% by 2034. At the current EU ETS price of around EUR 75 per tonne of CO2, a plant emitting 500,000 tonnes annually will see its uncompensated carbon cost grow by roughly EUR 1 million in 2026 alone, with that figure compounding every year through the decade. By 2034, full exposure means every tonne of clinker produced carries a market-rate carbon cost.

The phase-out also introduces a new compliance condition: free allocations from 2026 to 2030 are contingent on demonstrated energy efficiency measures and, for the worst-performing installations, the existence of a carbon neutrality plan. This is not guidance. It is a precondition for receiving free allowances at all.

The EU ETS benchmark itself is also changing. The new benchmark will shift from a clinker basis to a binder basis, which has direct implications for producers using supplementary cementitious materials (SCMs) such as fly ash, slag, or calcined clay. Producers whose product mix involves lower-clinker formulations may find their benchmark treatment changes. Understanding that interaction before allocations are set is important.

Sylvera's take: With free allowances phasing out from 2026, low-carbon retrofits will become increasingly valuable every year up to 2034. Producers need to model their cost exposure under the phase-out schedule now, not once the curve has moved against them.

2. EU CBAM: Carbon Performance Is Now a Trade Variable

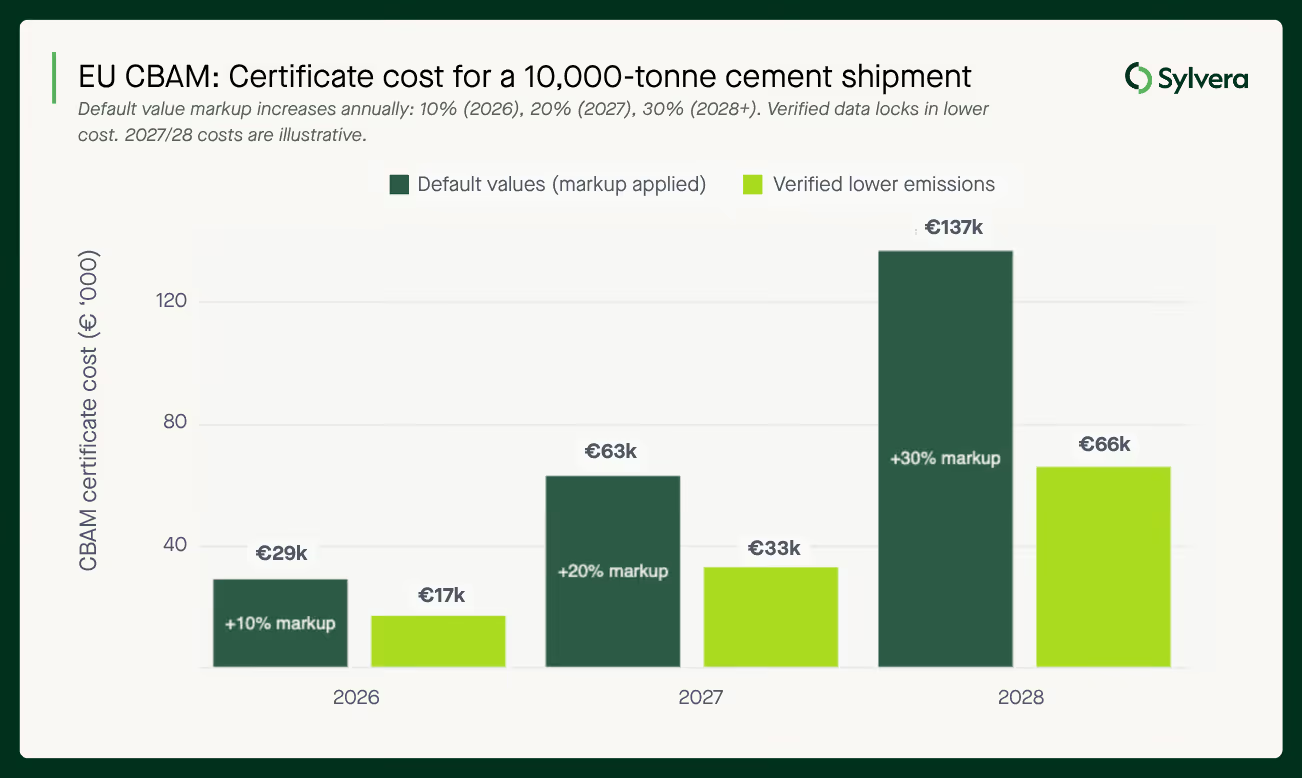

The Carbon Border Adjustment Mechanism entered its definitive phase on 1 January 2026. Any importer bringing cement into the EU must now surrender CBAM certificates priced against the EU ETS, currently set at EUR 75.36 per tonne of CO2 for Q1 2026.

The mechanism creates a direct commercial incentive for foreign producers to demonstrate lower emissions. Importers bearing the certificate cost will seek to minimise it, which means they will increasingly favour suppliers who can provide verified actual emissions data over those relying on EU default values. The default values carry a deliberate penalty: a 10% markup above country-specific averages in 2026, rising to 20% in 2027 and 30% from 2028 onward. That markup compounds on top of an already conservative base figure.

To illustrate the scale: for a 10,000-tonne shipment of grey clinker from a country without a country-specific default, the certificate cost on default values rises from approximately EUR 29,000 in 2026 to EUR 137,000 by 2028, driven by both the increasing CBAM phase-in factor and the escalating markup. A producer supplying verified actual emissions data of 0.88 tCO₂/t would face EUR 17,000 in 2026, rising to EUR 66,000 by 2028. That gap, roughly EUR 12,000 in year one and widening to EUR 71,000 by 2028, lands directly on the importer's balance sheet, and they will price it into supplier negotiations accordingly.

This is a structural change in how carbon performance translates into commercial terms. Lower-carbon producers outside the EU now have a mechanism through which investment in emissions reduction generates a direct price advantage in international trade, one that grows materially with every passing year.

Sylvera's take: CBAM creates a clear commercial opportunity, but the window is tight. Lower-carbon producers outside the EU need to start negotiating offtake arrangements with importers before Q4 2026, ahead of the first full year of certificate surrender obligations. The producers who arrive at those negotiations with verified data will be in a materially stronger position.

3. UK CBAM: Similar Mechanism, Different Market

From 2027, the UK will require importers of cement to report embedded emissions and surrender CBAM certificates priced against the UK ETS. The structural logic mirrors the EU mechanism: verified lower-emission producers reduce the certificate burden for importers, creating a price premium.

There are, however, meaningful differences producers should not gloss over. The UK ETS and EU ETS are separate schemes with different price dynamics. Depending on the spread between the two at any given time, the commercial value of a verified low-carbon profile may differ across the two markets, which has implications for producers selling into both.

The question of verification alignment also matters. Producers who have already built MRV (monitoring, reporting, and verification) infrastructure to satisfy EU CBAM requirements will want to confirm whether that data and methodology are accepted under the UK framework. The two regimes are similar in intent but are being developed independently, and the alignment of acceptable verification standards is not yet fully determined.

The planning stage of the UK mechanism gives producers outside the UK a window to prepare. Those who treat EU and UK CBAM readiness as a single integrated project, rather than two separate compliance exercises, will be better placed as both deadlines converge.

Sylvera's take: Producers targeting UK buyers should begin building data and verification capability now. Early movers will negotiate from a stronger position, and producers already working on EU CBAM verification should assess whether that work can be structured to satisfy both regimes simultaneously.

4. UK ETS: The Same Cost Logic, Starting a Year Later

UK cement plants face an analogous trajectory to EU producers under the UK ETS: annual reporting obligations, allowance surrender per tonne, and a free allocation phase-out beginning in 2027 over an indicative nine-year period. The progressive reduction in free allowances will raise the effective cost of high-carbon production every year through the mid-2030s.

The nine-year phase-out timeline may feel comfortable relative to the EU's 2034 deadline, but the economics of decarbonisation investment do not allow that comfort. Carbon capture, clinker substitution programmes, and fuel-switching projects all carry lead times of several years. A producer who begins feasibility work in 2026 or 2027 is positioned to have operational solutions in place before the cost curve steepens significantly. A producer who waits until the allowance cost is visibly painful is already behind.

Sylvera's take: UK producers should model their phase-out exposure now and map that against the lead times for the decarbonisation options available to their specific plant configuration. Decisions made in 2026 will determine cost positions in 2031 and beyond.

5. EACs and Book and Claim: A Voluntary Scheme

Beyond the compliance regimes, a voluntary market mechanism is emerging for cement and concrete built around Environmental Attribute Certificates (EACs) and a book-and-claim model.

EACs allow producers to unbundle the environmental attributes of their lower-carbon cement from the physical product. A buyer can purchase the certificate independently of where the physical material is delivered — which matters in an industry constrained by bulk logistics. It removes the requirement to physically receive the lower-carbon product in order to claim its environmental benefit.

Demand-side momentum is building. The Sustainable Concrete Buyers Alliance (SCoBA) — backed by Meta, Amazon, and Prologis — is running an RFP for low-emission cement EACs in spring 2026. Deals are already appearing in the market, including between Microsoft and Sublime Systems, and frameworks are being developed by RMI and the Centre for Green Market Activation.

The challenge is that no single methodology governs how producers participate. Unlike compliance mechanisms, EAC buyers are likely to impose integrity requirements beyond emissions reductions — additionality, co-claiming restrictions, and verification standards. The draft GHG Protocol AMI framework explicitly addresses both additionality and co-claiming, signalling that these will be baseline expectations rather than optional considerations.

For producers, the voluntary landscape needs to be understood now. The methodology a producer aligns to will shape which buyers they can sell to, how their carbon intensity is calculated, and whether their certificates will hold up under the scrutiny that is clearly coming.

Sylvera's take: The voluntary EAC market for cement is at an early stage, but the infrastructure is being built now. Producers who understand eligibility criteria, pricing dynamics, and how EACs interact with compliance obligations will be positioned to access a new revenue stream early. The market will reward those who engage before standards are set, not after.

6. Stacking Mechanisms: What Is Additive, What Is Complementary, and What Creates Risk

Most mechanism combinations are straightforward. For example, EU and UK CBAM operate independently across separate jurisdictions, the same MRV infrastructure can likely serve both, generating price premiums in parallel. ETS cost savings and CBAM price premiums reinforce each other commercially, rewarding the same underlying thing: lower carbon intensity. And where a producer already pays carbon tax under a recognised domestic scheme — including Turkey's ETS, which launched in 2024, or Switzerland's ETS, which is linked to the EU system — CBAM includes an explicit deduction to avoid double-charging.

The genuinely complex question is whether voluntary revenue, such as that from EACs, can sit alongside compliance mechanism benefits. In principle, a producer with lower emissions could simultaneously generate a lower CBAM burden for importers and sell EACs representing that same low-carbon production. Each mechanism is notionally measuring something different: embedded product emissions vs a tradeable environmental attribute, but they draw on the same underlying asset.

Until regulators issue clearer guidance, producers should treat compliance benefits and voluntary certificate revenue as competing claims on the same emissions performance — not an additive stack. The risk of getting this wrong, as scrutiny of environmental claims tightens, is both reputational and financial.

This means that to optimise revenue options, producers need to understand which mechanism suits their carbon intensity, production method, and location best.

Sylvera's take: Stacking mechanisms is possible and, in the right combinations, commercially powerful. But it requires clarity on which benefits attach to which tonnes, and that clarity is still being established by regulators. Producers who build their carbon data infrastructure now, with sufficient granularity to attribute benefits correctly, will have the most flexibility to maximise value across multiple mechanisms as the rules solidify.

What This Means: The Complex Mechanism Landscape and where to start

Across all five mechanisms, the underlying logic is the same: producers who can demonstrate lower carbon intensity generate a commercial advantage. The mechanisms differ in who bears the cost, how the premium is realised, and when they come into force — but they all reward the same thing.

For a producer trying to act on this, three questions matter most:

- Which mechanisms is my facility actually eligible for, given its location, export markets, and current emissions profile?

- What is my carbon intensity under each mechanism's specific methodology — because the same facility can have a materially different CI figure depending on which boundary, baseline, and allocation rules apply?

- What is the potential financial value, and how does it change as compliance and voluntary mechanisms evolve?

These aren't straightforward to answer. Each mechanism carries different data requirements, different LCA boundaries, and different verification standards. A facility optimising for EU CBAM may need to report embedded emissions differently than one seeking EAC certification or pursuing a CBAM deduction under Turkey's or Switzerland's ETS.

Sylvera works with cement producers to map facility-level eligibility across this mechanism landscape — identifying which combinations are available, what the carbon intensity looks like under each relevant methodology, and where the most material value sits.

Our recent work with CURA, a developer of low-carbon cement technology, shows what this looks like in practice. Sylvera independently assessed and benchmarked CURA's production against more than 3,000 facilities globally, placing it in the top 0.1% of cement producers for carbon intensity. We then mapped CURA's performance across relevant compliance mechanisms and quantified the potential commercial value — linking carbon intensity to financial outcomes across the ETS and CBAM in a form that is directly usable in investment and offtake conversations. Read the full case study here.

How Sylvera Can Help

Sylvera's Mechanism Eligibility Assessments are built for exactly this. For each mechanism in scope, we deliver three things:

- A binary, rule-traceable eligibility determination grounded in the rule text and the data a producer can actually produce

- A structured gap analysis that maps each failed criterion to the specific data, documentation, or operational change needed to unlock eligibility

- A lifecycle value estimate decomposed into compliance deficit offset, credit volume, and realised price — per tonne, per barrel, and per facility-year — using live Sylvera price indices and the regulator's own baselines.

For cement producers, live mechanism coverage includes EU ETS, CBAM, and EACs. Every determination is linked to the rule section and carbon intensity input that drove it, so outputs are auditable, defensible, and updateable as rules evolve — unlike a one-off consultancy memo.

Our carbon intensity assessments are designed against each mechanism's own LCA requirements and system boundaries, so the carbon intensity feeding an eligibility determination already respects the regulator's data needs. This matters in cement, where the same facility can carry a materially different carbon intensity figure depending on whether CBAM embedded emissions, EU ETS benchmarks, or EAC methodologies apply.

Producers who want to understand their position across this mechanism landscape — and maximise the value it represents — can request a sample report here.