“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

Read the full Buying Blind report here.

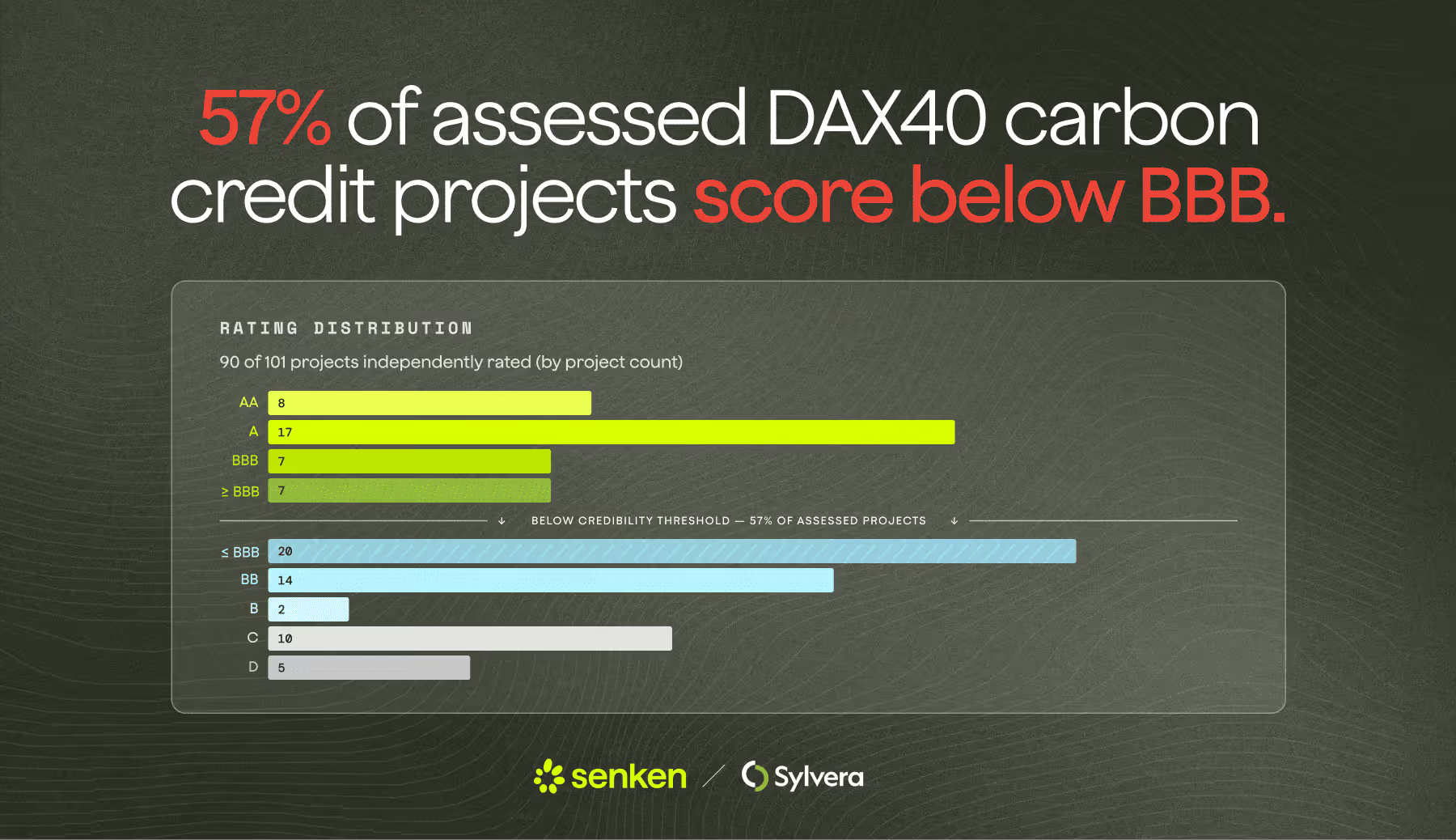

Senken’s Buying Blind report examined FY2025 CSRD carbon credit disclosures from 39 of Germany's largest listed companies. Of the 4.84 million credits reported, 45% could not be traced to a specific project from public sources. Of the projects we could identify and rate, 57% scored below BBB, Sylvera's threshold for credible climate impact.

It's worth being clear about what these numbers tell us, and some of the wider picture that’s worth considering in terms of corporate carbon credit purchasing.

Firstly, this is not a story about bad actors. The DAX40 companies in this analysis are, by and large, buying what the market offers and disclosing what regulation requires. The issue uncovered is that this type of regulation, in its current form, asks for very little. Aggregate volumes and registry names are required. Project identifiers, methodologies, and per-project volumes are not. Companies comply, and yet their purchases remain largely unverifiable, and often low-quality.

A useful way of interpreting this is not just understanding what regulation does or doesn’t require. Rather, what are the best corporate buyers already doing regardless of regulation? And what can others learn from them?

Certification is not the same as credibility

One thing the report data shows is that a registry label is not a quality guarantee. Credits carrying Verra or Gold Standard certification still appear throughout the lower end of Sylvera's rating distribution (as well as the higher end). Certification confirms a process was followed. It does not tell you what the credit represents, in terms of for example whether the underlying project would have happened anyway (additionality), or whether the carbon will stay stored (permanence).

This distinction matters greatly, and is what contributes to project ratings. And, the broader market is now increasingly pricing it in. Sylvera's Q1 2026 market data shows investment-grade credits (BBB+) now command an average of $20.10 per credit, up from $18.10 a year ago. Meanwhile, B-rated credits have fallen from $8.50 to $7.80 over the same period.

And these higher quality credits are increasingly in demand. The bifurcation between quality and legacy supply is the present reality of the voluntary carbon market.

For corporate buyers, the cost of doing this well is rising, but so is the cost of getting it wrong. Boards, investors, and regulators will increasingly be putting the spotlight on not just volumes of retirements, but increasingly the quality of them. Companies that cannot answer that second question with confidence are exposed.

What leading buyers are doing differently

Within the same DAX40 cohort, some of the companies toward the top of the scoreboard are already doing this well. And not because of regulatory pressure, but because of deliberate choices. Some are voluntarily disclosing project-level detail beyond what CSRD requires.

Some provided full project names, registries, vintages, and volumes. And, when looking at selected portfolios, there are instances of majority Sylvera-rated A or AA quality.

And, looking more widely, this quality pattern is visible globally. Sylvera's Q1 2026 data shows that UK buyers have moved from 37% high-rated retirements in 2022 to 85% in Q1 2026 - a quality transformation driven by disclosure pressure and evolving procurement standards. US and Canadian buyers have improved from 21% to 68% high-rated over the same period. The common thread across these markets is that buyers who applied rigorous internal standards early are now in a stronger position as scrutiny intensifies.

In terms of direct comparison to the DAX40 cohort, the leading buyers globally hold transparency at the project level. They know which projects they've funded, can name them, and can defend them. That is increasingly the standard that serious buyers are being held to.

The proactive approach: What good practice looks like

For corporates serious about getting this right, the framework is straightforward even if the execution takes effort.

Start at the project level.

Aggregate reporting tells you almost nothing about quality. The unit of analysis should be the individual project: its rating, its methodology, its geography. Before any purchase, the project should be identifiable in a public registry and independently assessable. The DAX40 data illustrates what happens without this discipline, with 45% of reported volume not able to be traced.

Use independent ratings.

Sylvera rates projects across additionality, permanence, carbon accounting, and co-benefits. These essentially determine whether a credit actually delivers real-world impact. A BBB or above rating is a meaningful threshold. Anything below it warrants serious scrutiny. The market is already moving this way: BBB+ rated credits now account for 62% of total rated market value, up from 31% in 2023.

Pay attention to compliance signals.

The convergence between voluntary and compliance markets is accelerating. CORSIA-eligible credits now represent close to 50% of new issuances, and the CCP price premium has more than doubled since 2023.

Credits that meet compliance-grade standards today are better positioned as regulatory demand tightens. Buyers who understand this are building portfolios that will hold up under any future framework, not just the current one.

Build internal quality benchmarks.

The companies doing this well have moved carbon credit quality out of the procurement team and into a broader governance conversation. They define what good looks like internally, document their criteria, and apply them consistently, regardless of what the cheapest compliant option on the market happens to be.

Sylvera's market data shows that tech and professional services firms are among those demonstrating the greatest sophistication here, planning well beyond 2030 targets rather than managing quarter to quarter.

Think ahead on supply.

High-quality supply is tightening. Sylvera's Q1 2026 data shows issuances of BBB+ credits declining even as demand increases, creating a growing premium for those that remain. One finding from the DAX40 data was how less than 1% of DAX40 carbon credits fund projects within the EU. Not unsurprising, given the current makeup of the supply side of the market.

But, as the EU builds out frameworks and high-quality domestic CDR supply (including biochar and other durable removal approaches) begins to scale, European buyers with early relationships in this space will be well positioned. The supply is nascent, but the quality potential is significant, and the window to get ahead of it is now.

The opportunity for corporates

The transparency gap this report exposes is real. But it is also, for companies willing to act on it, a meaningful competitive advantage. The market data is clear: quality commands a premium, supply of high-integrity credits is tightening, and compliance convergence means the bar will only rise.

Buyers who can demonstrate project-level quality are building credibility that will hold up under any future regulatory tightening, investor question, or other scrutiny.

And the data and tools to do this exist now. Sylvera's ratings and data platform are used by investors, corporates, and governments worldwide to assess carbon credit quality. To learn more about how Sylvera can support your carbon procurement strategy, get in touch.

Read the full Buying Blind report here.

.png)