“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

Carbon costs used to be a domestic concern, but the European Union has changed the rules. If your supply chain touches steel, cement, aluminium, fertilisers, electricity, or hydrogen, you need to understand what CBAM means for your business, and how to operate moving forward.

What Is CBAM in Europe?

CBAM stands for Carbon Border Adjustment Mechanism. It's an EU regulation that puts a carbon price on certain goods imported into the European Union. The mechanism mirrors the EU Emissions Trading System (EU ETS) which EU producers have operated under for years.

The idea behind CBAM is straightforward: Manufacturers inside the EU pay for every tonne of carbon they emit, so importers bringing in similar goods from other countries should do the same.

To clarify, CBAM isn't a tax. It's a carbon intensity equalizer that applies the EU carbon price consistently across both domestic industries and foreign producers in the EU market.

Why Was the Carbon Border Adjustment Mechanism Introduced?

Three interconnected problems drove the creation of CBAM.

The first is carbon leakage, i.e. the risk that EU industries move production to countries with lower environmental standards to avoid carbon costs, ultimately shifting rather than reducing emissions.

The second is offshored emissions, i.e. when EU companies import carbon-intensive goods rather than making them domestically. The emissions still happen, they just don't appear on EU ledgers.

The third is the inconsistency of global carbon pricing. Not every country prices carbon seriously. The inconsistency distorts competition and undermines the goal of reducing global emissions.

CBAM sits within the EU's broader Fit for 55 package, which aims to cut net greenhouse gas emissions by at least 55% by 2030. It also supports the EU's longer-term net-zero targets. By extending the EU ETS logic to imports, regulators hope to encourage cleaner industrial production around the globe.

How Does CBAM Work?

CBAM requires EU importers to account for the carbon embedded in goods they bring into the European Union. Here's how the process unfolds in practice.

- First, the importer reports embedded greenhouse gas emissions, i.e., the carbon emissions released during the production of the goods. This includes direct emissions from the production process itself, and in some cases, indirect emissions from electricity consumption.

- Second, the EU ETS sets the carbon price. The CBAM certificate price is linked to the weekly average auction price of EU ETS allowances. As such, the carbon prices paid vary.

- Third, the importer purchases CBAM certificates equivalent to the embedded emissions in their imports. These certificates are then surrendered to EU authorities.

- Fourth, if the exporting country applied a carbon pricing system, importers deduct the cost from their CBAM obligation, avoiding double payment.

This last point is important. CBAM isn't designed to punish countries that already price carbon. It's designed to close the gap when no pricing exists, and thus reduce direct and indirect emissions.

When Does CBAM Start?

The CBAM implementation process is divided into two phases:

Transitional Phase (2023–2025)

During this period, CBAM obligations were reporting-only. EU importers had to submit quarterly reports to cover embedded emissions data and production information. No financial payments were required at this point. The phase was designed to help companies build data infrastructure.

Definitive Regime (From 2026 On)

The financial mechanism turned on in January 2026. Importers must now purchase and surrender CBAM certificates proportional to the carbon emissions embedded in their imports. At the same time, the free allocation of allowances for covered sectors under the EU ETS will gradually disappear. As such, the financial incentive to source from lower-carbon suppliers will increase.

Who Is Affected by CBAM?

CBAM covers six sectors: cement, iron and steel, aluminium, fertilisers, electricity, and hydrogen. These sectors were chosen because they're among the most carbon-intensive goods, and because EU producers in these sectors already face significant carbon costs under the ETS.

CBAM affects two distinct groups. EU importers, AKA companies registered in the EU that bring covered goods across EU borders, carry the direct compliance obligation. They must track embedded carbon emissions, file reports, and purchase certificates.

Non-EU producers face a different but equally significant obstacle. If your manufacturing facility exports covered goods to the EU, for example, your carbon intensity directly impacts the cost to buyers. Producers with lower carbon intensity become more competitive — and those who can prove it independently are better positioned to attract offtakers and command a premium.

Upstream supply chains are also affected. If a company's products feed into covered goods that end up in EU markets, the carbon intensity of its production matters to potential buyers.

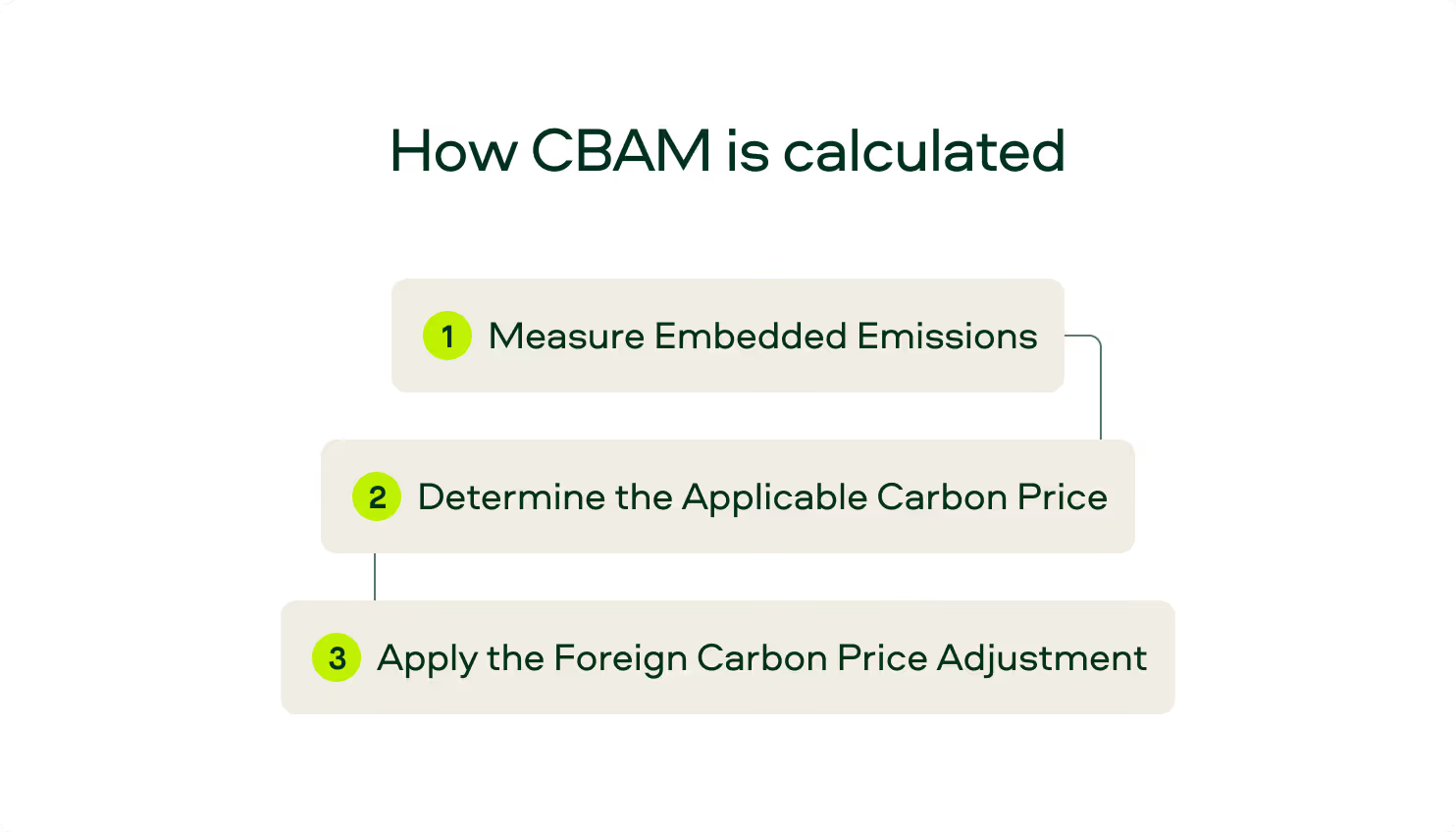

How Is CBAM Calculated?

The CBAM calculation has three steps:

Step 1 — Measure Embedded Emissions

First, calculate the carbon intensity of the product to see how many tonnes of CO₂e are emitted per tonne of output. Actual data from facilities is preferred, but if verified emissions data isn't available, you can use the EU's default values. (Note: The EU's default values are conservative. Because of this, using the EU's default values can lead to overpayment, which is why facility-level data is preferred.)

Step 2 — Determine the Applicable Carbon Price

The CBAM certificate price is directly tied to the weekly average auction price of ETS allowances, denominated in euros per tonne of CO₂. This means the cost of CBAM compliance fluctuates with the carbon market. In other words, per CBAM rules, applicable carbon prices vary.

Step 3 — Apply the Foreign Carbon Price Adjustment

If the exporting country already charges a carbon price on the production of goods, the amount is deducted from the CBAM cost. The formula looks like this:

CBAM cost = (Embedded emissions – foreign carbon price adjustment) × EU ETS price

For example, a steel plant in America exports to the EU market. Its production generates 2 tCO₂ per tonne of steel. The EU ETS price is €90 per tonne, and the steel plant's home country charges a local carbon tax of €20 per tonne. The calculation is: (2 – 0) × €90 = €180 per tonne, minus the €20 local tax adjustment, resulting in a CBAM cost of €160 per tonne of steel.

What Is CBAM Reporting?

CBAM reporting requires EU importers, officially known as authorized CBAM declarants, to submit quarterly reports through the EU's digital CBAM registry. Said reports must cover embedded emissions details, production data from the originating facility, and methodology verification.

The key challenge is data collection from non-EU suppliers. Few facilities outside the EU track and report emissions data in a format that's compatible with CBAM requirements.

When actual carbon emissions data isn't available, importers must use EU default values. This, as noted above, leads to higher costs than actual facility performance would justify. As such, complying with CBAM reporting requirements starts with getting reliable, facility-level emissions data from suppliers.

And independent, third-party assessments — rather than self-reported figures — give importers data they can rely on and defend.

CBAM and the Broader Decarbonisation Picture

CBAM is one piece of a larger strategic puzzle that every corporate buyer now faces: how to optimise spend across direct emissions reduction and carbon offsetting.

Switching to lower-carbon commodities — lower-CI cement, green hydrogen, green ammonia — directly reduces Scope 1, 2, and 3 emissions. Carbon credits offset what remains. The question for most organisations isn't which approach to use, but how to allocate between them to hit targets at the lowest total cost.

CBAM sharpens that calculation. Every tonne of carbon embedded in an import now has a direct financial cost, which changes the economics of sourcing lower-carbon supply versus continuing to offset. Organisations that model this trade-off systematically — rather than treating commodity procurement and carbon credit strategy as separate decisions — will find the most efficient path to their targets.

For airlines, this dynamic is particularly sharp. Under CORSIA, carriers must weigh the cost and availability of carbon credits against Sustainable Aviation Fuel (SAF) and Lower Carbon Aviation Fuel (LCAF). Each option has different CI implications, different pricing, and different availability by route and region. The right compliance strategy depends on being able to compare all three on a consistent basis — something that requires integrated data across commodity markets and carbon markets.

The Convergence of Carbon Credits and Carbon Intensity

CBAM and expanding compliance schemes are tightening the "penalty net" on carbon-intensive goods. What was once a voluntary ESG consideration is now a direct financial calculation.

As such, tech companies weigh the cost of voluntary carbon removal credits against the premium for low-carbon steel in their supply chains. At the same time, airlines navigate CORSIA-eligible credits alongside emerging low-carbon fuel premiums, and commodity producers face a fundamental question about how to monetize their lower-carbon attributes to achieve price premiums.

This convergence of carbon credits and carbon intensity presents a data problem. Different carbon accounting systems—EU ETS, national schemes, sectoral mechanisms, etc.—define and measure carbon intensity differently. Without a comparable view of carbon intensity at the facility level, buyers can't make informed procurement decisions, producers can't reliably price low-carbon options, and capital can't flow to top decarbonization opportunities.

The solution isn't full harmonization, but interoperability. The industry needs common data standards that let participants compare performance across borders and systems.

Where Sylvera Stands

Sylvera has expanded beyond carbon credit ratings into carbon-differentiated commodity markets, As such, our platform provides the data infrastructure companies need for industry convergence.

That means independent carbon intensity verification, mechanism eligibility mapping, and market intelligence — for buyers, producers, and investors across the carbon credit and physical commodity markets.

Mechanism Eligibility & Value Assessment

Our Mechanism Eligibility & Value Assessment helps producers know exactly which schemes their facility qualifies for, and what that's worth commercially. Get a clear, auditable answer across CBAM, plus other mechanisms like LCFS, EACs, and more, with a market-priced value estimate per mechanism.

Carbon Intensity Assessment

Sylvera's Carbon Intensity Assessment offers independent, facility-level carbon intensity scoring for commodities like hydrogen, ammonia, and cement. Rather than relying on broad industry averages and producer self-reporting, Sylvera produces standardized CI metrics that allow comparable benchmarking across facilities.

We calculate CI both under Sylvera's own consistent framework and under the specific schemes that matter — including CBAM — from a single data input. This gives buyers and investors evidence-based differentiation data for suppliers, and gives producers a credible way to demonstrate performance to the market.

For buyers conducting due diligence on a specific facility before committing, Carbon Intensity Assessments go deeper: independently verified CI, confidence scoring based on data quality, mechanism eligibility confirmation, and delivery risk assessment.

Commodity Insights

Sylvera's Commodity Insights product tracks supply and demand across carbon-differentiated commodity markets, including live data on facilities, announced projects, production capacity, and offtake agreements.

Buyers can filter thousands of facilities by carbon intensity, geography, production method, and mechanism eligibility — building a qualified shortlist without relying on brokers. Producers can benchmark their CI position against competitors, identify where demand is emerging, and find the offtakers actively buying in their space.

This gives users visibility into regulatory exposure, competitive positioning relative to peers, and market intelligence to make better sourcing decisions.

As carbon becomes a direct cost embedded in every import transaction, companies need independent carbon intensity verification infrastructure. That's what Sylvera provides.

Try Commodity Insights for free in the Sylvera platform

What Comes Next for CBAM?

CBAM currently covers six sectors, but expansion is likely.

Indirect emissions, particularly from electricity used in production, are expected to fall more fully within scope over time. The EU is watching developments in other jurisdictions as well.

In the UK, the government is advancing its own carbon border mechanism, designed to mirror key elements of the EU approach. In the US, proposals like the Foreign Pollution Fee Act have raised the prospect of a similar instrument. Globally, regulators are converging toward carbon intensity-based trade policy. In other words, the logic of CBAM is proving contagious.

For companies operating across global supply chains, this means CBAM is not a one-time compliance project. It represents the future of how trade and carbon interact.

Organisations that build the data infrastructure now — facility-level CI data, mechanism eligibility mapping, integrated commodity and carbon market intelligence — will be better positioned as the scope widens and the financial stakes grow.

5 Common Challenges Companies Face

Most companies face the same set of difficulties when it comes to CBAM:

- Data gaps are a fundamental challenge. Calculating actual embedded emissions at the facility level requires granular production and energy data that many companies never collect. Building those data pipelines takes time, thus the transitional phase.

- Supplier transparency is closely related. For many EU importers, the data problem rests in the manufacturing facilities of non-EU suppliers. Persuading suppliers to calculate embedded emissions requires strong relationship management skills.

- Default values that lead to overpayment are a real risk. When actual data isn't available, EU default values apply, and they're typically set high to discourage use. Companies that rely on defaults rather than proprietary carbon data pay more.

- Verification bottlenecks are another constraint. CBAM reporting requires verified data, but the ecosystem of accredited verifiers for non-EU production facilities is still developing. Companies can help themselves by engaging verification providers now.

- Internal coordination is often underestimated. CBAM sits at the intersection of finance (because of the certificate cost), sustainability (because of emissions measurement), and procurement (because of supplier selection). These functions don't always work well together. Building cross-functionality for CBAM purposes is a practical step in the right direction.

Commit to CBAM Compliance

CBAM marks a structural shift in global climate policy.

Carbon intensity is now a trade metric, not just an ESG metric. Companies should treat it as such, and build infrastructure to measure, verify, and act on carbon intensity data.

Doing so will lead to real advantages, like lower certificate costs, stronger supplier leverage, better regulatory resilience, and the ability to prove differentiation to investors and customers.

Sylvera's Carbon Intensity Assessment and Commodity Insights help teams standardize carbon intensity data, benchmark suppliers consistently, and turn CBAM compliance into a competitive advantage rather than a cost center. Request a demo to learn more.