"Ao longo dos anos, investimos significativamente em nossa equipe de dados de campo, com foco na produção de classificações confiáveis. Embora isso garanta a precisão de nossas classificações, não permite a escala dos milhares de projetos que os compradores estão considerando."

Para obter mais informações sobre as tendências de aquisição de créditos de carbono, leia nosso artigo"Key Takeaways for 2025". Compartilhamos cinco dicas baseadas em dados para aprimorar sua estratégia de aquisição.

Mais uma coisa: os clientes do Connect to Supply também têm acesso ao restante das ferramentas da Sylvera. Isso significa que você pode ver facilmente as classificações dos projetos e avaliar os pontos fortes de um projeto individual, adquirir créditos de carbono de qualidade e até mesmo monitorar a atividade do projeto (especialmente se você investiu no estágio de pré-emissão).

Agende uma demonstração gratuita do Sylvera para ver os recursos de compras e relatórios da nossa plataforma em ação.

Por trás de cada compra corporativa de CDR está um equilíbrio entre estratégia de portfólio, considerações de reputação, defesa interna, padrões em evolução e gerenciamento de riscos.

Nossa pesquisa de mercado de CDR 2025 - realizada com a CDR.fyi - e as discussões do setor esclarecem como os compradores corporativos estão navegando nesse cenário. Entender a mentalidade deles é fundamental para fornecedores, investidores e formuladores de políticas que trabalham para ampliar as remoções duráveis.

Os padrões estão prontos para impulsionar a demanda de CDRs corporativos?

65% dos compradores corporativos citam padrões claros de zero líquido como o principal fator que aumentaria sua motivação para comprar um CDR durável

Os padrões fornecem o que, na maioria das vezes, é o "porquê" para os compradores corporativos. Órgãos de padronização como a iniciativa Science Based Targets (SBTi) cumprem essa função essencial.

Isso se torna especialmente crítico quando as equipes de sustentabilidade precisam justificar os investimentos em CDR para os CFOs, que exigem uma lógica comercial clara. Sem mandatos externos, a defesa interna pode ser mais difícil.

Um exemplo recente importante é o Corporate Net-Zero Standard V2 da SBTi, que ilustra tanto o progresso quanto a incerteza contínua. A nova estrutura permite que as empresas usem créditos de CDR para emissões residuais do Escopo 1 até que atinjam o zero líquido, mas somente para emissões difíceis de serem eliminadas por meio de metas duráveis de curto prazo. Embora isso represente um movimento em direção à inclusão de CDRs, a SBTi continua cautelosa em relação ao uso mais amplo de créditos de carbono, deixando os compradores corporativos com pouca clareza sobre quando e como podem implementar remoções em suas estratégias de descarbonização.

Quais preços de CDR os compradores corporativos estão dispostos a pagar?

77% dos compradores classificam o preço como um dos principais fatores na seleção de fornecedores de CDR. 52% dos compradores classificaram o preço como um dos principais fatores na seleção de um fornecedor de CDR durável, enquanto 46% disseram que custos mais baixos aumentariam sua motivação para comprar CDR durável

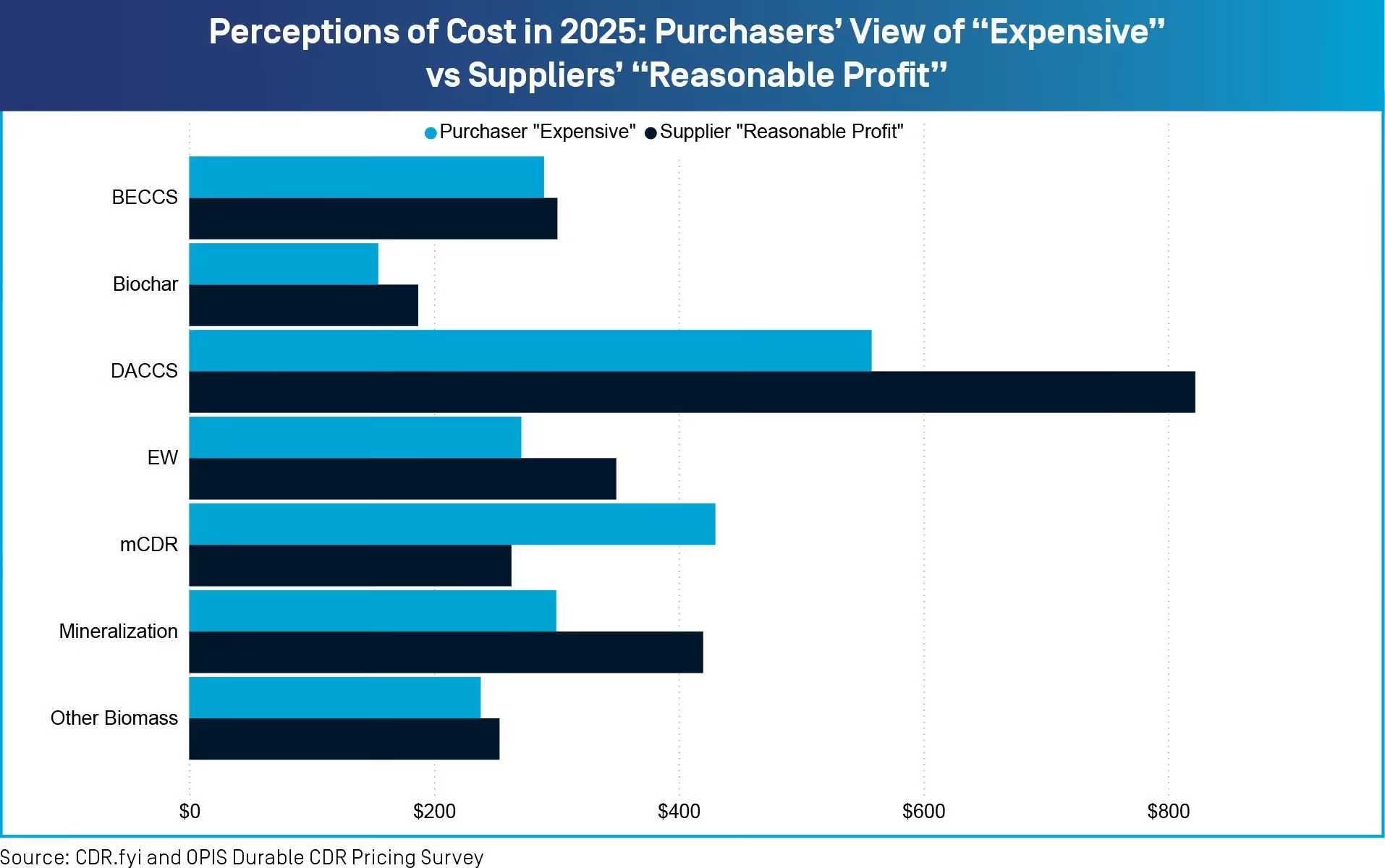

Persiste uma lacuna de expectativa de preço entre compradores e vendedores. Os compradores corporativos são mais otimistas em relação à queda de preços do que os fornecedores, criando um obstáculo fundamental ao progresso.

Por exemplo, uma pesquisa de preços CDR.fyi/OPIS separada constatou que os fornecedores de biochar precisam de US$ 187 por tonelada métrica em 2025 e US$ 180/mt em 2030 para obter um lucro razoável. Entretanto, os compradores consideram caros os preços de US$ 155/mt em 2025 e US$ 130/mt em 2030. No caso do Enhanced Rock Weathering (ERW), os fornecedores buscam um preço de US$ 349/mt em 2025 e US$ 328/mt em 2030 para obter lucro, mas os compradores consideram US$ 271/mt em 2025 e US$ 238/mt em 2030 como caros.

O desafio do preço se intensifica à medida que a base de compradores se expande para além dos primeiros usuários. Os compradores corporativos iniciais (principalmente grandes empresas de tecnologia) geralmente estão dispostos a pagar prêmios para apoiar o desenvolvimento do mercado.

No entanto, para que o mercado seja realmente ampliado, a próxima onda de compradores provavelmente será mais sensível ao preço, criando pressão sobre os preços de curto e médio prazo.

O que as empresas estão realmente comprando? E o que elas planejam comprar?

Como se espera que os preços dos CDRs diminuam com o tempo, os compradores corporativos enfrentam um dilema de tempo. Então, o que os compradores estão realmente comprando neste momento? E quais tipos de crédito eles estão priorizando em seu planejamento de compras?

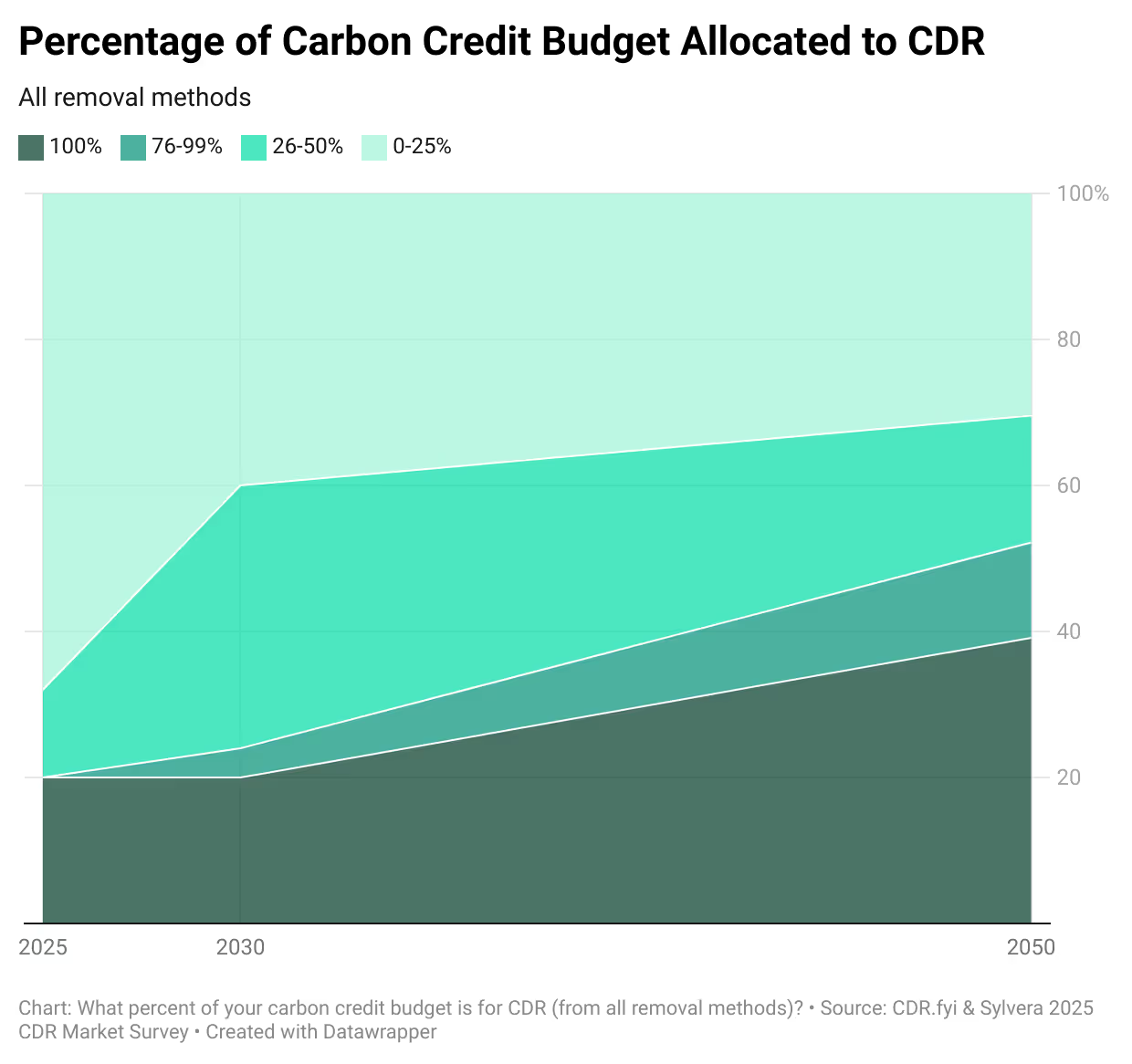

Em termos atuais, com base em nossa amostra limitada, o biochar lidera o caminho com 31% dos entrevistados que já compraram. As intenções de compra estão aumentando acentuadamente para ERW e Bioenergia com Captura e Armazenamento de Carbono (BECCS). Espera-se que o ERW aumente de 15% para 42% até 2030.

Até 2050, a projeção é de que o BECCS seja o principal método de CDR durável, juntamente com o biochar. Dito isso, todos os métodos mostram aumentos.

Os especialistas do setor com quem conversamos este ano oferecem motivos convincentes para a adoção agora, apesar dos custos mais altos em muitos métodos.

Por que comprar agora:

- As compras antecipadas ajudam os fornecedores a garantir o financiamento e a desenvolver a capacidade

- As empresas adquirem uma valiosa experiência em compras para futuros requisitos de conformidade

- Com a iminência de uma escassez de suprimento em 2030, as organizações com metas precisam garantir o suprimento agora por meio de contratos de compra e venda

- As compras antecipadas de diversas empresas sinalizam a direção do mercado, criando confiança

- Para tipos de projetos como o biochar, é mais provável que os preços aumentem do que caiam no médio prazo, portanto, vale a pena fixar um preço hoje

Como os compradores estão lidando com as complexidades do CDR?

Entender o biochar não prepara os compradores para avaliar o ERW ou a captura direta de ar. Essa diversidade tecnológica pode criar barreiras para uma aquisição eficiente.

Principais desafios de complexidade:

- Cada tecnologia de CDR requer conhecimento especializado para ser avaliada adequadamente

- Os longos períodos de avaliação frustram tanto os compradores quanto os fornecedores

- Práticas inconsistentes de divulgação de dados retardam a realização de negócios

À medida que o mercado se expande para além de um pequeno grupo de compradores experientes, navegar por essas complexidades se tornará ainda mais desafiador. Portanto, as agências de classificação independentes e as plataformas de dados são essenciais para fornecer uma visão transparente e consistente da integridade do projeto e do risco de entrega com confiança.

Essa lacuna de conhecimento é agravada pela necessidade de narrativas convincentes que se alinhem aos valores da marca e às expectativas das partes interessadas.

Os compradores corporativos, mais acostumados com soluções baseadas na natureza, costumam perguntar sobre os co-benefícios, buscando estruturas familiares para justificar os investimentos.

A narração de histórias varia drasticamente de acordo com a tecnologia:

- Injeção de bio-óleo: Envolvimento menos óbvio da comunidade em comparação com projetos florestais

- Projetos do DAC em países desenvolvidos: Co-benefícios limitados além da criação de empregos

- Projetos em mercados em desenvolvimento: Narrativas mais fortes sobre desenvolvimento econômico e transferência de tecnologia

Como os compradores corporativos justificam as compras de CDR internamente?

Além dos padrões, 62% dos compradores pesquisados identificaram benefícios comerciais claros ou ROI como um fator motivador importante. Isso destaca o desafio persistente da defesa interna dentro das corporações.

Diferentemente dos investimentos comerciais tradicionais com retornos financeiros mensuráveis, as compras de CDR agregam valor por meio de:

- Benefícios para a reputação

- Conformidade regulatória futura

- Alinhamento com as metas de descarbonização de longo prazo

Essa proposta de valor cria atritos quando as equipes de sustentabilidade precisam garantir a adesão dos departamentos financeiros acostumados a um ROI mais direto e de curto prazo.

73% dos fornecedores de CDR ainda não entregaram um único crédito

As preocupações podem ser agravadas pela incerteza na entrega. Muitas vezes, os compradores estão apostando em capacidades futuras em vez de serviços comprovados. Essa incerteza força as empresas a avaliar não apenas a tecnologia em si, mas também a experiência operacional, os fundamentos comerciais e a viabilidade de longo prazo dos fornecedores.

Como os compradores corporativos estão criando seus portfólios de CDR?

As estratégias corporativas de CDR estão evoluindo para abordagens de portfólio sofisticadas e diversificadas, em vez de simples escolhas binárias entre remoções baseadas na natureza e duráveis.

Realidade atual do mercado: As soluções baseadas na natureza superam os CDR duráveis em uma proporção de 6:1

projeção para 2050: Essa diferença diminui drasticamente para 1,2:1

Em vez de considerar os diferentes tipos de remoção como alternativas concorrentes, as empresas com visão de futuro estão adotando a correspondência de emissões. Essa abordagem alinha diferentes tipos de emissões com soluções de remoção correspondentes com base em características como durabilidade.

A mentalidade do portfólio também reflete as realidades práticas dos negócios. Nenhuma empresa age isoladamente; suas estratégias de carbono devem estar conectadas a objetivos nacionais mais amplos e a requisitos legais sobre o clima e a natureza.

Essa realidade significa que a maioria das empresas manterá uma combinação de tipos de crédito em seus portfólios, incluindo soluções baseadas na natureza e remoções projetadas.

O que vem por aí na compra de CDRs corporativos?

A demanda por CDRs corporativos provavelmente permanecerá concentrada entre alguns dos principais compradores, até que o mercado desenvolva um apelo mais amplo por meio de preços mais baixos e padrões mais rígidos voltados para CDRs.

- As regulamentações e o desenvolvimento da oferta devem estar alinhados

- A disponibilidade de financiamento deve corresponder à demanda do comprador

- Os padrões continuarão a evoluir à medida que a ciência avança

- Os contratos de longo prazo precisam de flexibilidade para mudar os requisitos

Para os compradores corporativos, a prioridade imediata é desenvolver a capacidade interna e a experiência em aquisições enquanto os padrões amadurecem. Até mesmo as pequenas compras desempenham um papel de grande importância, sinalizando confiança para o mercado e apoiando a expansão do fornecedor.

Como Robert Höglund argumentou, a demanda corporativa voluntária é essencial nesse período intermediário: assim como os eletrônicos de nicho sustentaram o setor de energia solar na década de 1970, as compras corporativas de CDRs hoje são a ponte que pode sustentar o setor até a chegada dos mercados de conformidade na década de 2030.

Qual é o papel da COP30 nesse momento?

COP30 no Brasil chega em um momento importante para o CDR e os compradores corporativos. O pavilhão inaugural do CDR30 - a primeira presença dedicada ao CDR em uma COP - representa uma oportunidade para abordar e discutir os principais desafios nesse espaço.

Ao reunir formuladores de políticas, investidores e profissionais do setor, COP30 pode abordar as discussões técnicas e as negociações políticas necessárias para harmonizar as normas, os regulamentos e os mecanismos de financiamento necessários.

A política é especialmente importante para o CDR porque a demanda voluntária, por si só, não pode oferecer a escala ou a certeza necessárias. Sinais regulatórios claros, integração aos mercados de conformidade e incentivos de apoio determinarão se a ação corporativa antecipada se traduzirá em um mercado durável e com capacidade de investimento, capaz de atingir níveis de gigatoneladas.

Se você é um desenvolvedor, comprador ou investidor de CDR, por que não participar de nossos próximos drinques CDRcomo parte da semana do Carbon Unbound Europe?