“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

Commodity certificates have moved from concept to conversation. With that in mind - and specifically Environmental Attribute Certificates (EACs) - a new Sylvera survey of producers and buyers across the commodity landscape reveals a market that is forming faster than its foundations.

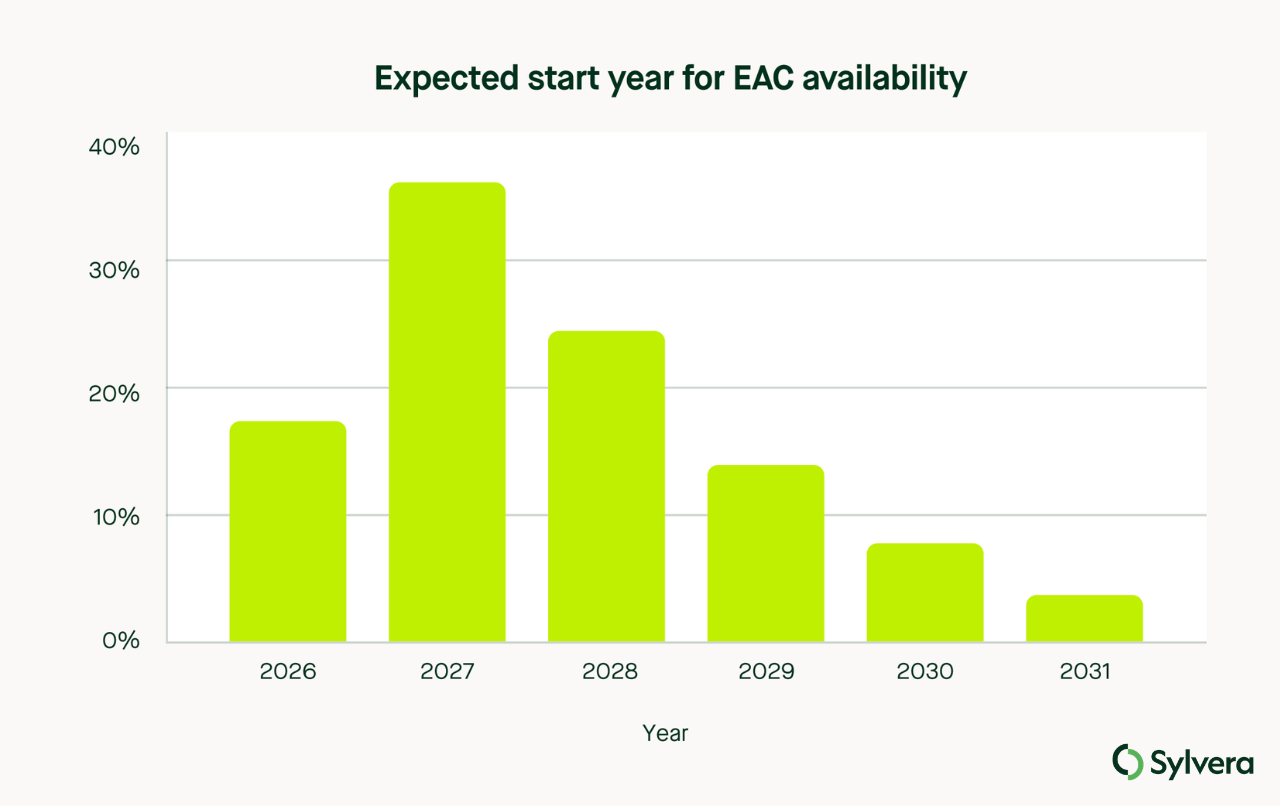

The headline finding: 75% of producers expect to begin issuing EACs within three years, with 2027 the most commonly cited target. Buyer demand is forming too, with respondents reporting annual appetite of 1.7 to 2.1 million EACs through 2030.

What EACs are — and why they matter

EACs work on the same principle as Renewable Energy Certificates (RECs). Just as RECs allow buyers to claim the environmental value of renewable power regardless of where they are in the grid, EACs allow buyers of commodities — cement, steel, ammonia, aviation fuel — to claim the lower-carbon intensity of a producer's output without needing a direct supply relationship.

The mechanism is known as book-and-claim, and it solves one of the hardest barriers in green procurement: the geographic mismatch between where low-carbon production happens and where buyers need materials.

For sectors that are hard to abate — construction materials, heavy industry, chemicals, transport fuels — EACs are becoming a critical tool for connecting corporate decarbonisation targets to real-world emissions reductions. Rather than offsetting emissions through carbon credits alone, buyers can now take credit for contributing to upstream change in how these commodities are made.

What the market looks like today

The demand signal is clearest from large corporates with Scope 3 targets. Microsoft has already executed EAC deals with lower-carbon cement and steel producers, deploying a book-and-claim structure to access environmental attributes from production happening elsewhere in the world. Meta, Amazon, and Google have built structured procurement programmes for lower-carbon materials. These are purchases with defined criteria that are driving broad market attention.

Our survey found that SBTi compliance is the primary driver of buyer intent, with 78% of buyers stating that published SBTi targets or trade-offs with existing offset instruments were their main reason for purchasing. The recent release of SBTi V2, which formally incorporates book-and-claim instruments, provides a clear framework that will bring secondary buyers — currently waiting on sidelines for standards to crystallise — into the market.

Read our analysis of what SBTi V2 means for commodities here.

Respondents covered a range of commodities. Cement and concrete was the largest producer segment (27%), followed by biofuels (24%), with fertilisers, steel, road transport fuels, and agricultural products also represented. 45% of respondents came from North America.

Five signals from the data

Price discovery is hard to come by. This was the clearest producer need, with 31% naming pricing benchmarks as their single top requirement. The range of stated prices tells the story: across commodities, producers named prices anywhere from $5 to just under $400 per certificate. Even within cement — the most represented segment — expected prices ranged from $60 to $200 per tonne.

Supply is ahead of issuance infrastructure. The 75% of producers planning to issue by 2028 reflects genuine momentum. But product-specific registries are still being developed, third-party verification capacity is limited, and standards frameworks that would allow buyers to compare certificates with confidence are, outside of cement, largely absent. The risk is that intended supply outstrips the market's ability to absorb it credibly.

SBTi V2 is the demand catalyst. The formalisation of book-and-claim in SBTi's framework is the most significant near-term demand driver the survey identified. It gives buyers a standards basis to act — and gives producers a clear integrity bar to clear.

Buyers will pay for verified carbon intensity, not claims. When asked what would determine price, buyers ranked emissions reduction achieved first (45%), and verification of those claims second (11%).

Producers can't see the demand they're building for. Producers consistently surfaced the same need: access to buyers, off-take visibility, demand signals. Both sides are waiting for the other to move first.

To see the full breakdown, download the full report here

The supply scarcity problem

Using our global carbon intensity benchmarking across 3,723 cement products worldwide, we found that fewer than 2% would currently qualify for EACs on emissions intensity alone — requiring a rating of D or better (below 500 kgCO₂e/t). Over 3,300 products fall entirely outside the grading range.

This matters for pricing. Genuine scarcity of qualifying supply is exactly the condition under which a credible benchmark creates real premium. Producers who can demonstrate they are in that minority, so those with verified, third-party data are in a position to command attention in a market where demand is forming faster than credible supply.

What producers should do now

For producers, the practical sequence is straightforward:

- Calculate carbon intensity using an industry-recognised standard

- Benchmark against the most credible and widely-accepted external reference

- Secure independent verification ahead of counterparty due diligence

- Build buyer relationships now, while supply is scarce enough to command attention before the 2027 issuance wave

This Sylvera 2026 EAC Market Survey draws on responses from participants across the EAC market, collected via a structured survey of 18 questions covering production capacity, issuance timelines, carbon intensity, pricing expectations, demand drivers, and priority support needs.

Respondents were split between producers and sellers of EACs, and buyers or users of EACs, spanning a broad range of commodities including cement and concrete, biofuels, SAF, agricultural products, hydrogen, fertilizer, and steel. Geographically, the survey captured perspectives from North America, Europe, Africa, Oceania, Asia, and South America.

The survey was designed to surface directional signals on intent, pricing expectations, and market readiness. All individual responses are kept confidential, results are reported in aggregate only.