“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

Forward contracts and compliance demand push prices higher despite falling retirements

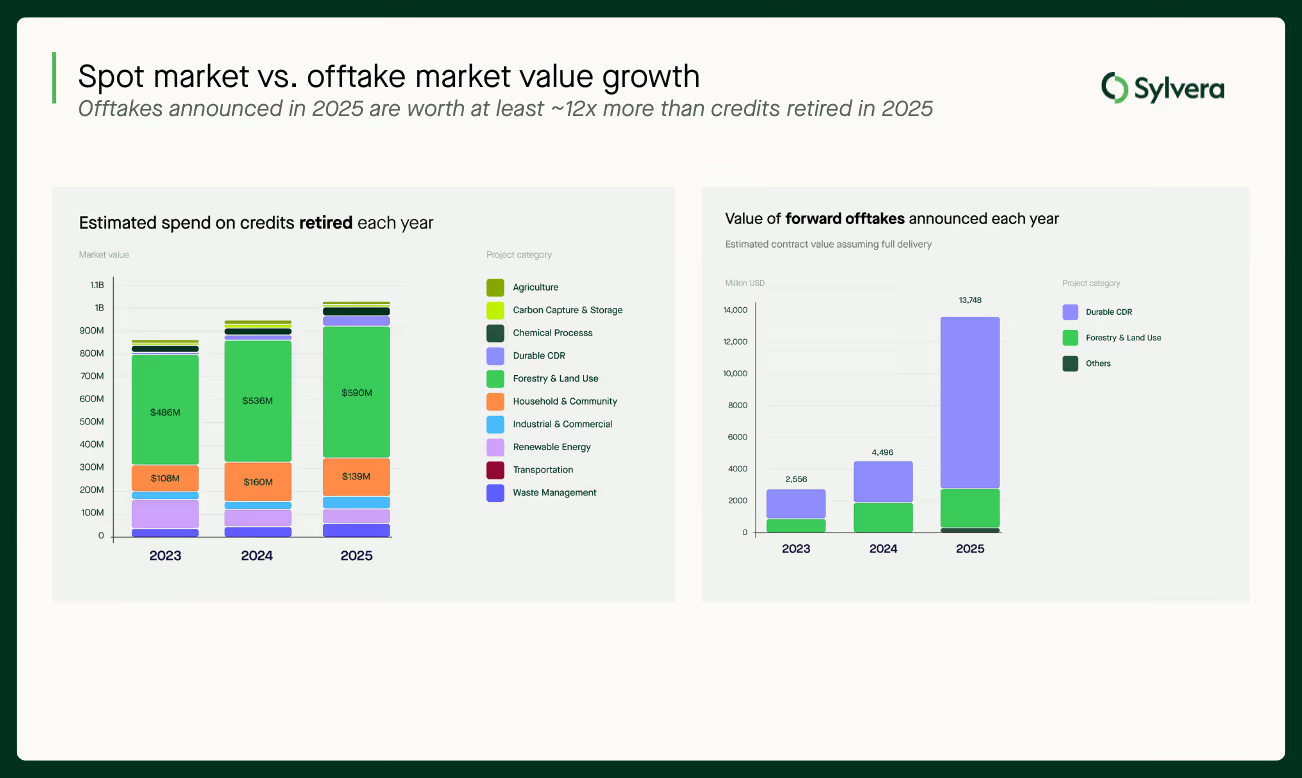

- 168 million credits retired in 2025, with market value up 6% to US$1.04bn, as higher prices offset a 4.5% decline in volumes

- Forward offtake market surged to US$12.3 billion, more than 12x spot market value, signalling potential for 3x market value expansion

- High-quality credits (BBB+) made up nearly a third (31%) of retirements and trade at clear premiums with BBB+ ARR credits averaging around US$26 per tonne, versus US$14 for lower-quality supply, leaving top-tier credits in deficit for a third year running

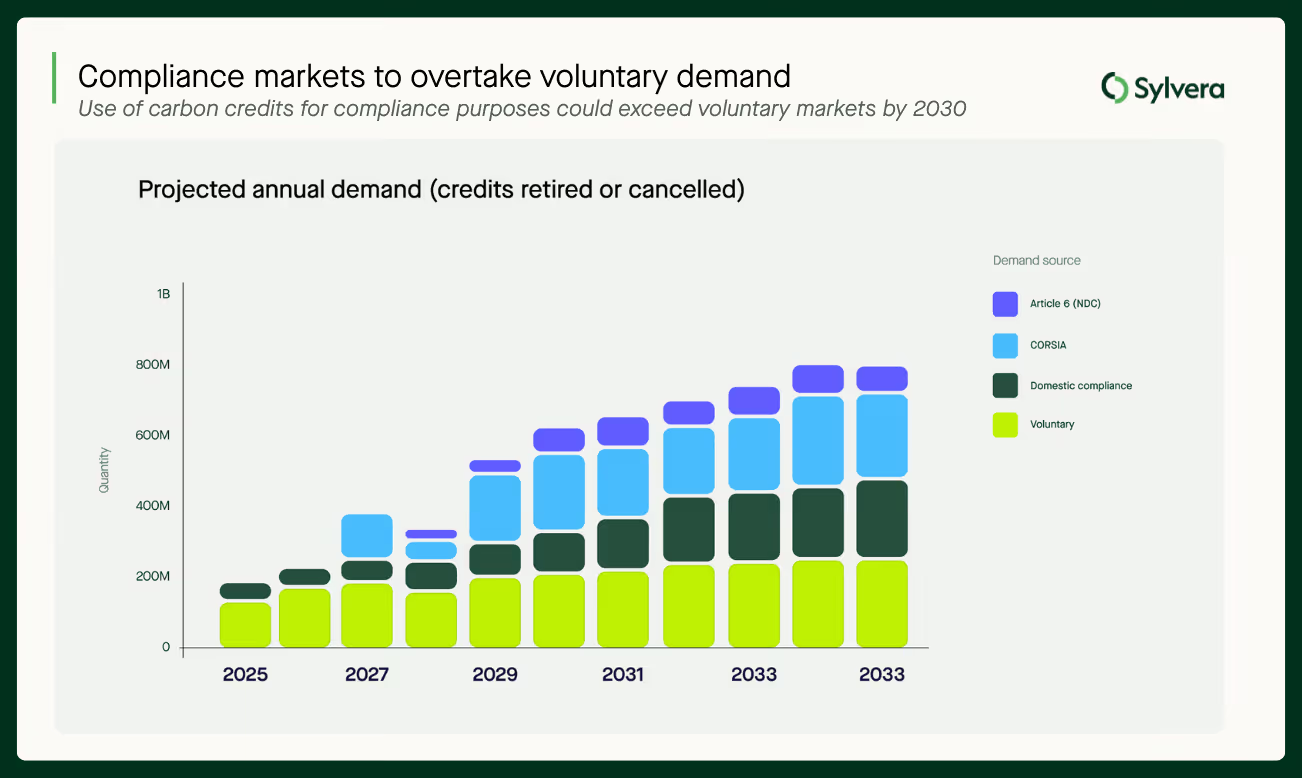

- Compliance demand volume projected to exceed that of voluntary by 2027, with nearly a quarter of 2025 retirements already linked to compliance schemes, including CORSIA and CCP-labelled credits

Our annual State of Carbon Credits 2025 report is now live, analysing how pricing, quality and compliance pressures are reshaping market economics.

The report finds that while overall retirements declined 4.5% to 168 million credits, market value continued to rise. End-user spending reached US$1.04bn in 2025 (up from US$980m in 2024), with the weighted average price increasing to US$6.10 as buyers paid more for higher-integrity supply.

Most significantly, the forward offtake market is already signalling how the next phase of the carbon market may be priced.

Offtake deals announced in 2025 totalled US$12.3 billion, up from US$3.95 billion in 2024, while delivering only around 12 million credits annually through 2035 at a weighted average price of US$180. This represents over US$2 billion in annual market value from less than 10% of current retirement volumes. If similar pricing dynamics extend across the broader voluntary market, it suggests potential for 3x market value growth even without volume expansion, demonstrating how quality premiums are fundamentally reshaping carbon market economics.

A market increasingly shaped by quality

The report shows a continued move towards higher-rated credits across both issuances and retirements. In 2025, credits rated BBB and above accounted for 31% of retirements, up from 25% the previous year. For the first time, half of all retired credits were rated BB or higher, underlining growing buyer scrutiny and demand for integrity.

At the same time, the supply of high-quality credits remains constrained, with the market increasingly defined by scarcity at the top end and oversupply at the bottom, as procurement shifts toward higher-rated and compliance-ready credits. Highly-rated credits have experienced a market deficit for the third consecutive year, as demand continues to outpace new issuances. By contrast, lower-quality and unrated credits remain heavily oversupplied, accounting for the vast majority of excess issuance each year.

Allister Furey, CEO of Sylvera, said: “Spot market volumes only tell part of the story. Forward markets show buyers are already pricing future supply very differently — paying around US$180 per credit for quality removals versus a US$6 spot average. That signals a structural shift toward value growth driven by integrity.”

Buyers pay a growing premium for integrity

Pricing data from 2025 shows that quality is now firmly embedded in carbon credit pricing. While the market-wide average price sits at US$6.10, prices vary widely within project types.

Afforestation, Reforestation and Revegetation (ARR) projects traded anywhere from US$2 to over US$50, with around half priced between US$5 and US$25. Highly-rated ARR projects with a rating of BBB or above averaged more than US$26 by late 2025, compared with around US$14 for lower-rated equivalents. These prices had been closely aligned at the start of the year, highlighting how rapidly the quality premium has emerged.

The report also finds buyers are paying additional premiums for projects with strong co-benefits for nature and communities, reinforcing the shift away from price-led strategies.

Furey added: “Integrity has become a key driver of value in carbon markets. Buyers are increasingly sophisticated and prepared to pay more for credits that withstand scrutiny and deliver genuine climate impact. And, for compliance markets, quality premiums will continue to be less marked, with higher scrutiny of risks around volume delivery and corresponding adjustments.”

Compliance demand gains momentum

In 2025, compliance programmes accounted for nearly a quarter of all credits retired or cancelled. Sylvera’s latest modelling indicates compliance demand could exceed voluntary purchases by 2027, driven primarily by CORSIA Phase 1 ahead of its January 2028 deadline.

Almost 46% of credits issued in 2025 came from methodologies potentially eligible for CORSIA, while 10% carried CCP-approved labels, signalling growing alignment with recognised integrity thresholds.

As voluntary and compliance buyers increasingly compete for the same high-quality supply, pressure on prices and project finance dynamics is expected to intensify.

Outlook for the year ahead

The findings point to a carbon market entering a new phase, where pricing, forward contracting and compliance timelines, not headline volumes, will determine growth. Early access to high-quality, compliance-ready supply is likely to become a decisive advantage as regulation tightens and scrutiny intensifies.

Download the State of Carbon Credits 2025

Drawing on live data from more than 22,000 projects and 40,000 companies worldwide, our The State of Carbon Credits 2025 is available for download here.