“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

What Is Green Cement?

Green cement, also called low-carbon cement, refers to cement produced with significantly lower carbon intensity than conventional Portland cement, AKA grey cement.

However, a more useful framing is "carbon-differentiated." In our view, the market should price a continuum of carbon intensity (CI) where every reduction has value. After all, a facility that cuts CI by 30% through clinker substitution is carbon-differentiated even if it's not zero carbon.

A binary "green vs. grey" framing misses the point—and the opportunity. This is because conventional Portland cement carries a high carbon intensity of roughly 0.6–0.9 tCO2 per tonne, depending on the facility, fuel mix, and clinker ratio. The best-performing facilities today achieve 0.3–0.5 tCO2 per tonne through existing technologies. Novel approaches aim for near-zero.

Cement carries a heavy carbon footprint because roughly 60% of carbon emissions come from calcination, the chemical process of converting limestone to clinker, which releases CO2 as an unavoidable byproduct. The remaining ~40% comes from fuel combustion in the kiln.

This split means you can't decarbonize cement by switching to renewable energy. Process emissions from calcination require a different solution.

Why Cement Decarbonization Matters

Aside from water, cement is the most widely produced material on Earth. Global production runs at roughly 4 billion tonnes annually. Because of this, even small reductions in CI, applied at scale within the cement industry, have enormous climate impact.

Regulatory pressure is only accelerating this fact. Cement is one of six sectors covered by the EU's Carbon Border Adjustment Mechanism (CBAM). From 2026, EU importers must purchase CBAM certificates based on the embedded carbon in cement imports. This requirement creates a financial consequence for high CI production, and an advantage for lower-carbon producers.

Meanwhile, demand for cement and concrete production is at an all-time high. Data centers, infrastructure expansion, and urbanization across developing economies are the main drivers. As Shona Crawford-Smith, General Manager – Carbon-Differentiated Commodities at Sylvera, puts it: "We need more of everything everywhere, but it all needs to be decarbonized at the same time."

Companies like Microsoft, Meta, and others actively source lower-carbon cement and environmental attribute certificates for construction projects. Plus, the First Movers Coalition has made buyer commitments for green cement, and construction companies operating in the EU face their own compliance requirements. The demand signal is real and growing.

How Cement Producers Reduce Carbon Intensity

To reduce CI in cement manufacturing, producers must address the process and energy used. Several pathways exist, each with different carbon impact, feasibility, and capital requirements.

.png)

Clinker Substitution

When it comes to reducing carbon emissions in cement production, clinker substitution is the most established approach.

Producers replace some clinker, the most carbon-intensive component, with supplementary cementitious materials (SCMs). These include fly ash, ground granulated blast furnace slag (steel slag or GGBS), limestone filler, natural pozzolans, calcined clay, and silica fume.

Calcined clay, used in LC3 cement, is a promising pathway. Clay is globally abundant, unlike fly ash and steel slag, which depend on coal and steel production to exist as waste materials.

As a bonus, many of these alternative materials qualify as industrial by-products or recycled materials, fitting neatly into circular economy principles.

At the end of the day, clinker substitution can reduce carbon intensity by 20–40% depending on the substitution ratio, though it's limited by material availability and performance requirements.

Clinker substitution also offers potential cost savings, since SCMs are often more cost-effective to produce than clinker. Equally as important, the resulting material, when properly engineered, can match or exceed the compressive strength of traditional cement, so it's extremely usable.

Alternative Fuels and Energy

By replacing fossil fuels in the kiln with waste-derived fuels, biomass, or hydrogen, producers minimize their energy consumption footprint during the cement-making process. Some plants in Europe achieve over 80% alternative fuel rates to help reduce carbon dioxide emissions.

The electrification of kilns using renewable energy is another approach that could result in low-carbon concrete. Producers are testing this method, but it remains early-stage.

The alternative fuels and energy pathway addresses ~40% of emissions that come from fuel combustion, reducing carbon intensity by 10–25% depending on substitution rate and fuel type.

Carbon Capture, Utilization, and Storage (CCUS)

CCUS is the only pathway that can address process emissions from calcination, i.e., the emissions you can't eliminate by changing raw materials or fuel sources.

Producers are testing post-combustion capture, oxy-fuel combustion, and direct separation for effectiveness. It's important because CCUS can reduce carbon intensity by 50–90%, but capital costs are high, and CO2 transport and storage infrastructure must exist.

One key advantage specific to cement: Producers can retrofit facilities with carbon capture relatively quickly compared to building greenfield sites. This means incumbents like Holcim and HeidelbergCement can decarbonize existing capacity rather than writing it off.

Novel Cement Chemistries

New producers have developed cement formulations that avoid calcination entirely. Examples include geopolymers, magnesium-based cements, mineralization-based approaches, and other cement alternatives with unique properties and lower environmental impact.

These represent the longest-term pathway to near-zero or zero carbon cement. Though we should say, most aren't at a commercial scale and face adoption challenges, like building codes, performance standards, and contractor familiarity. Still, these new cement formulations represent a genuinely promising strategy for the construction industry's sustainable future.

How Cement Producers Can Monetize Lower Carbon Intensity

Most cement producers know they need to reduce greenhouse gas emissions. They may even have lower carbon intensity than their peers. What they don't know is how to get paid for it.

Crawford-Smith explains that producers always ask, "How could that translate to money? Because that's the important bit. Again, everything is money."

Sylvera has mapped over 21 monetization mechanisms for a single fertilizer producer. The cement landscape is similarly complex. Here are the key options.

CBAM and EU ETS

CBAM creates a direct financial link between CI and market competitiveness.

From 2026, EU importers must purchase certificates for the embedded carbon in cement imports. Lower carbon intensity equals fewer certificates, which reduces costs for buyers. As such, low-carbon producers are more attractive than conventional cement production plants.

For EU-based producers already operating under the Emissions Trading Scheme (EU ETS), lower carbon intensity means fewer allowances, which means lower compliance costs. As free allocation disappears between 2026 and 2034, the financial advantage grows.

Also worth mentioning, the UK is developing its own border adjustment mechanism, which will extend the compliance footprint further in an effort to achieve carbon neutrality.

Environmental Attribute Certificates (EACs)

EACs separate the environmental attribute, i.e., the lower carbon intensity, from the physical commodity. In other words, a producer can sell cement as traditional concrete, then sell the environmental certificate to a buyer who wants to claim the lower carbon intensity.

This is valuable in cement because cement is heavy and expensive to transport. If a low-carbon cement producer in one region can't physically supply a buyer in another, they can sell the EAC instead. The buyer gets the environmental claim, while the producer gets additional revenue. Companies like Microsoft and Meta have already purchased EACs for cement and steel.

One important distinction: Environmental attribute certificates in this context are not the same as renewable energy certificates, which are sometimes also called EACs. As Crawford-Smith notes, "Some people internally have got confused, and I always have to caveat."

Carbon Credits

Producers using CCUS or novel cement chemistries may be able to generate carbon credits for the CO2 captured or avoided. This is especially true if said producers use methodologies for industrial decarbonization or carbon sequestration that reduce global carbon emissions.

These credits need independent assessment and verification, like any other credit type, which connects directly to Sylvera's broader work in carbon markets.

Green Premiums and Offtake Agreements

Some buyers pay a direct premium for lower-carbon cement. Data center developers, corporate sustainability teams, and construction companies with net-zero commitments are anchor buyers for sustainable building materials. Also, procurement alliances like the First MoversCoalition and ConcreteZero create aggregated demand signals to support premium pricing.

That said, many buyers want lower-carbon construction materials but won't pay higher prices for them. The business case often depends on compliance costs—CBAM, EU ETS. Producers must show that lower-carbon cement is cost-competitive once carbon is properly priced.

As Crawford-Smith puts it: "When you factor in the internal carbon pricing for a buyer or a compliance tax, actually [they're then competing and the green is winning. But it's not because they're charging a premium, necessarily."

The Complexity Problem

Each monetization mechanism has its own carbon intensity calculation methodology, eligibility criteria, and financial model. The same facility can carry a materially different CI figure depending on whether CBAM embedded emissions rules, EU ETS benchmark logic, or EAC methodology applies, and that difference determines both eligibility and financial value.

Producers need to understand which mechanisms they qualify for, what their carbon intensity score would be under each framework, and what the financial value would be, both now and in the future when compliance schemes evolve and pricing dynamics shift.

Sylvera's Mechanism Eligibility Reporting is designed to answer exactly these questions, delivering a rule-traceable eligibility determination, a structured gap analysis mapping failed criteria to the specific changes needed to unlock eligibility, and a lifecycle value estimate per mechanism decomposed into compliance deficit offset, credit volume, and realised price per tonne and per facility-year.

Our work with CURA, a developer of low-carbon cement technology, illustrates what this looks like in practice. Sylvera independently assessed CURA's production against more than 3,000 facilities globally, placing it in the top 0.1% of cement producers for carbon intensity. We then mapped that performance across relevant compliance mechanisms, quantifying potential commercial value across ETS and CBAM in a form directly usable in investment and offtake conversations.

Who's Buying Lower-Carbon Cement?

Demand for lower-carbon cement comes from several entities.

Tech companies, like Microsoft and Meta, purchase physical, lower-carbon cement and EACs for data center construction. Data center construction companies, acting on behalf of tech clients, are also active buyers. Then, commercial property developers who operate under EU compliance requirements face direct financial incentives to source lower-carbon construction materials.

There are also infrastructure companies with public sustainability mandates that specify GHG emissions criteria in procurement. And buyer alliances like the First Movers Coalition and ConcreteZero create aggregated demand signals across the construction industry.

For buyers, the challenge is comparing suppliers. Without standardized carbon intensity data, procurement decisions rely on producer claims. That's a problem when trying to make progress toward a more environmentally friendly process than traditional cement production allows.

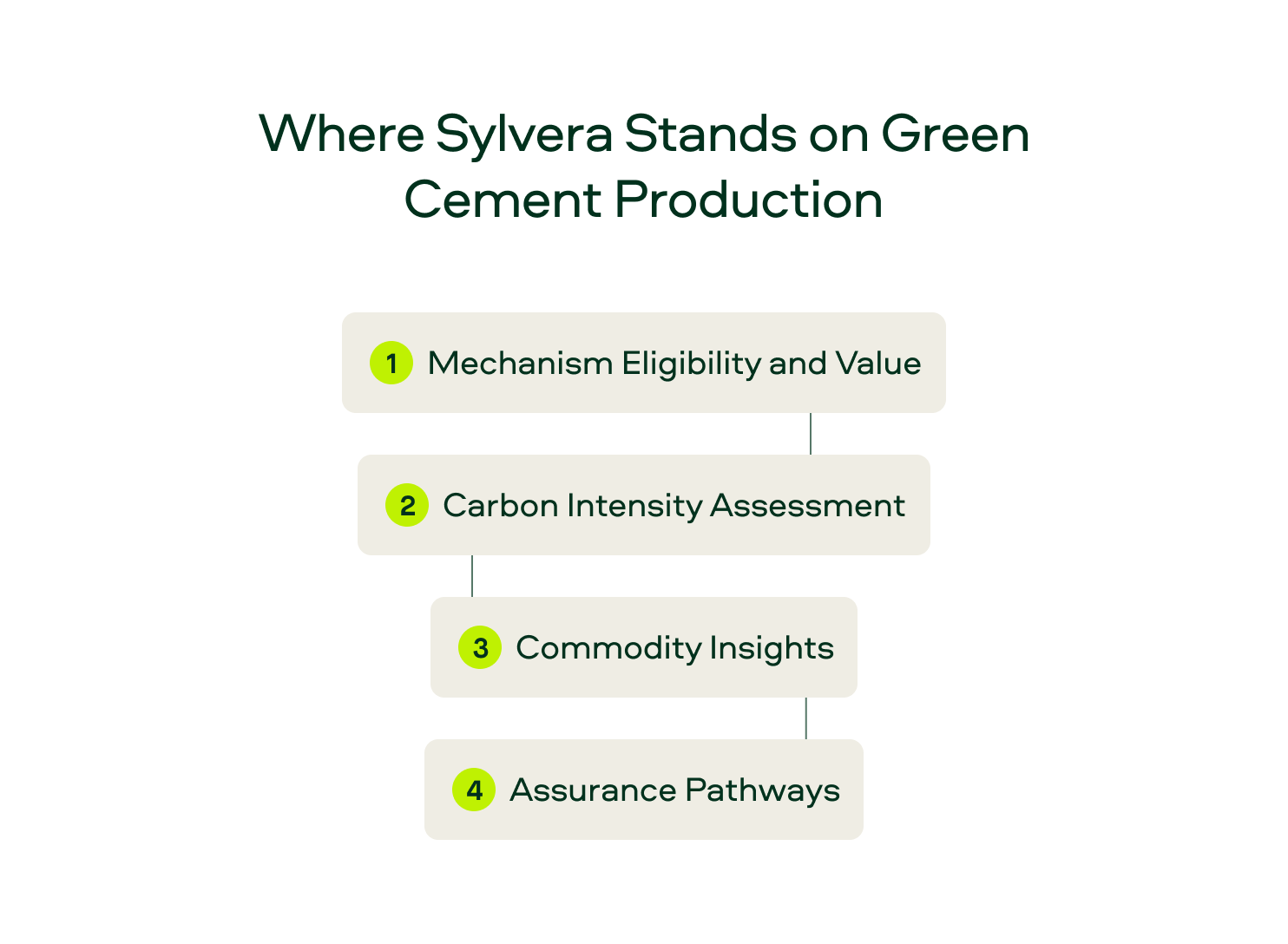

Where Sylvera Stands on Green Cement Production

Sylvera operates at the intersection of carbon markets and lower-carbon commodities by providing rigorous independent assessments. For cement producers, this means four things:

Mechanism Eligibility and Value: Sylvera helps producers understand which mechanisms they're eligible for, what their carbon intensity scores would be under each framework, and what the financial value of their lower emissions could be—both now and as compliance schemes evolve. Each mechanism has a different way of calculating carbon intensity.

Carbon Intensity Assessment: Sylvera also provides independent, facility-level carbon intensity verification. We calculate CI under our own standardized framework and mechanism-specific requirements, including CBAM, from a single data input. This gives producers the evidence they need to access markets and prove their competitive advantage.

Commodity Insights: Sylvera's market intelligence covers over 3,000 cement facilities globally, which enables producers to benchmark performance against their peers and buyers to compare suppliers on a standardized basis. These capabilities turn carbon intensity into a procurement criterion, which is exactly where the commodities market needs to go.

Assurance Pathways: Finally, Sylvera provides independent third-party assurance directly or prepares data packages for verified auditors required by specific mechanisms like CBAM. Either way, producers get a clear path from data to market access with our platform.

Request a demo to see how Sylvera helps cement producers unlock the value of lower CI.