“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

On 17 July 2026 the European Commission tabled its overhaul of the Emissions Trading System (COM(2026) 616). Published alongside an Electrification Action Plan and badged as "driving competitiveness and cost-effective decarbonisation," it’s the Commission's answer to sustained pushback from member states worried about industrial competitiveness.

It does realistically widen the carbon budget and ease near-term pressure on commodity producers, but it doesn’t change the underlying need to start measuring emissions and building the business case for decarbonisation. If anything, it makes acting early more valuable.

To stabilise near-term carbon prices and avoid undercutting investment already committed on the previous terms, most of the changes land from 2031 onwards. That reflects what industry has been asking for: room to pull the lower-hanging levers of decarbonisation today, and more time before the largest capital decisions fall due.

Producers who use this as an opportunity to understand their pathway and build the case now will be the ones positioned to capture free allocation and transition funding once the conditions bite in 2031.

Importers are on the same clock from the other side, with the CBAM charge still climbing to full cost, just on a slightly slower schedule.

So, the time to lock in lower-carbon suppliers and get embedded-emissions data in order is now.

The big picture: a slower, looser carbon price

The cap is the total number of allowances the system issues each year, and it shrinks annually by the “linear reduction factor” (LRF).

The proposal cuts that factor from around 4.3% today to 3.7% for 2031–2035, then to just 1.7% from 2036. In plain terms, the pool of allowances shrinks far more gently, keeping supply flowing into the 2040s rather than running dry around 2039.

Two levers do the loosening. From 2036 the EU plans to buy up to 260 Mt of high-integrity international credits, which lets it cut domestic effort by up to five percentage points (to -85% versus 1990 for 2036–2040). And the Market Stability Reserve, the mechanism that soaks up surplus allowances, will absorb them at half the current rate (12% instead of 24% from 2028) and lean toward smoothing price swings.

The net effect is more supply and a softer, more predictable carbon price in the near term than the old rules implied. But there is a safety catch: if credible international credits fail to appear, the LRF snaps back to 2.7% from 2036, tightening the cap again. Weak credit quality mechanically means a stronger EUA.

What it means for the market

EU commodity producers

Europe's energy-intensive producers are the clearest near-term winners. A slower cap decline and a gentler carbon-price path lower compliance costs, and producers in CBAM sectors retain partial free allocation for four additional years (see below). That relief is conditional, however. From 2031, free allocation is split: 80% is granted against a verified plan to invest in EU decarbonisation, and the remaining 20% is released only once those investments are delivered and the emissions reductions verified by the end of each five-year period. Producers that relocate activity outside the EU must return allowances.

There is a competitive wrinkle worth drawing out. Because free allocation is handed out on a benchmark-and-output basis rather than on actual emissions, producers still pay the carbon price at the margin, and those beating the benchmark can sell their surplus, so the system keeps rewarding cleaner operators, new entrants included. What extending free allocation does slow is the pass-through of carbon costs into the price of conventional steel, cement and ammonia.

That widening price gap is precisely the tailwind low-carbon products rely on, and four more years of partial free allocation, alongside a slower CBAM ramp on imports, keeps it narrower for longer. The proposal's answer is to lean less on the carbon price to pull clean product through, and more on funding the plants directly.

Alongside the stick, the proposal builds out a substantial support architecture, and this is arguably the more important half of the story for industry. The centrepiece is a new Industrial Decarbonisation Bank, operating from 2028 as an EU-level financing entity for technologies that cut emissions at industrial installations, including those that also generate permanent removals. It runs in two phases.

First, an "Investment Booster" (2028–2031) reserves 400 million allowances, roughly €30 billion at recent prices, to award fixed carbon premia on a first-come, first-served basis that deliberately rewards speed, with a ring-fenced share for lower-income member states and payments tied to independently verified emissions avoidance. From 2031, the Bank shifts to competitive tenders awarding Carbon Contracts for Difference and carbon premiums, giving projects the long-term revenue certainty that underpins a final investment decision, backed by bid and completion bonds to ensure serious intent and timely delivery. A "Competitiveness Seal" links successful projects to the wider European Competitiveness Fund.

In parallel, the Innovation and Modernisation Funds are refreshed and broadened to cover electrification and industrial decarbonisation, and member states may continue to compensate electro-intensive industries for the indirect carbon costs passed through electricity prices.

For producers, the real work now happens before any allowances are claimed. With free allocation tied to delivering actual decarbonisation, and a pot of funding attached to it, the operators who benefit will be the ones who understand their plant's route to lower emissions early enough to build the business case around it. That means knowing which technologies are viable for a given site, what the transition costs, and which of the new mechanisms and funds it can draw on, so the investment can be justified and the support secured ahead of time rather than scrambled for after the fact. This is where good data earns its keep, and where Sylvera helps producers map the pathway, benchmark their carbon intensity and pin down the value of decarbonising before they commit.

Bottom line:

The largest cost relief in the package, but free allocation is now a performance contract, and the winners will be the producers who build the business case early enough to secure the funding on offer.

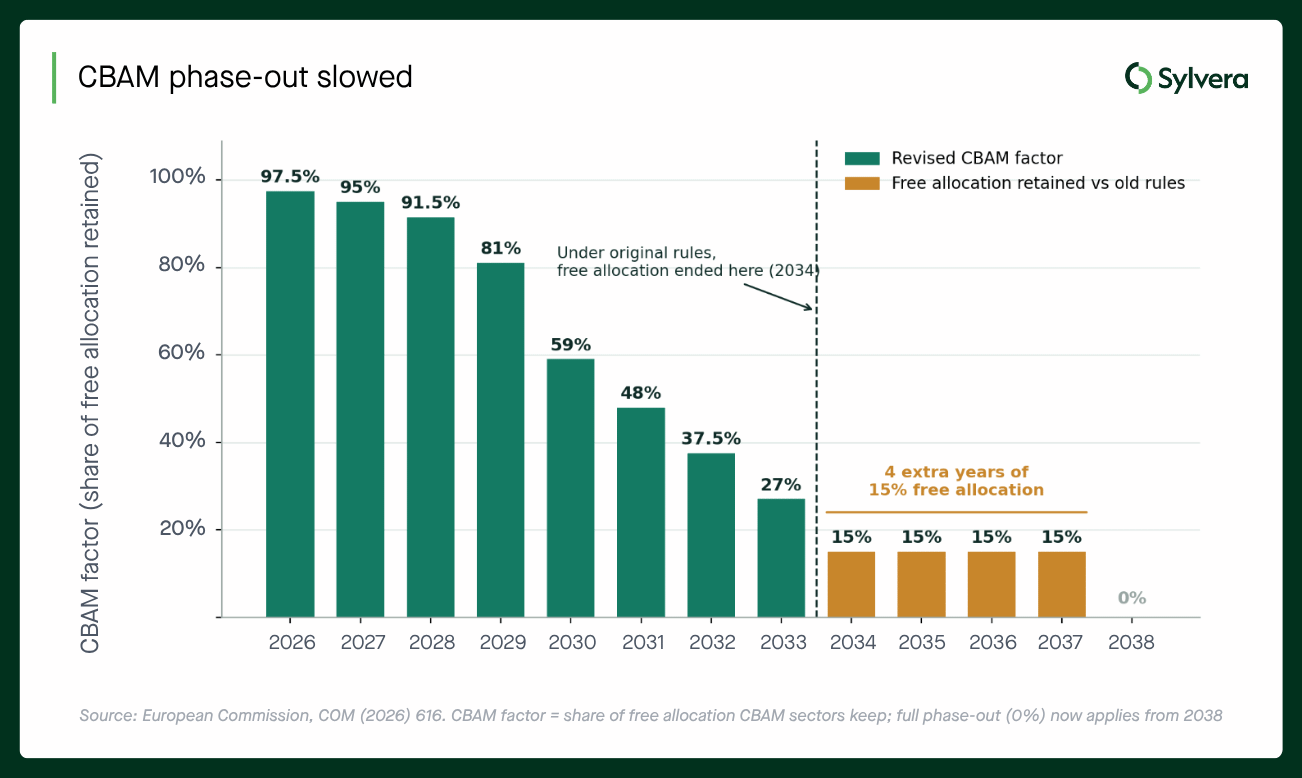

The CBAM timeline that shapes trade

CBAM works by charging imports the same carbon cost EU producers face. As EU free allocation phases out, the import charge phases in. The revision slows that handover: the “CBAM factor,” the share of free allocation EU producers keep, now steps down gently and holds at 15% from 2034 to 2037, hitting zero only in 2038, compared to old rules it ended in 2034.

This single schedule drives the outlook for the next two participants.

Producers outside the EU selling into the bloc

Because EU producers keep 15% free allocation through 2037, the CBAM charge on imported goods ramps up more slowly and reaches its full level later, in 2038 rather than 2034. That is a reprieve: the cost disadvantage in the EU market builds more gradually over the rest of this decade. The direction of travel is unchanged, though, and the EU is also launching an “ETS as a service” offer to help third countries price carbon domestically.

The way to protect EU market share remains cutting the embedded emissions in exported goods, which in turn makes credible, comparable carbon-intensity data a competitive necessity rather than a reporting chore.

Bottom line:

More time before the full CBAM cost bites, but no change to the destination, lower-carbon products remains the moat.

Importers of CBAM goods

An importer’s CBAM certificate bill is tied to that same phase-in, so a slower ramp means lower certificate costs for longer, with full exposure arriving in 2038. The extra runway is best used to lock in lower-carbon suppliers and build the embedded-emissions data that will be needed once the charge reaches 100%.

Bottom line:

Near-term cost relief, but sourcing and budgeting should already assume full CBAM from 2038.

The one caveat

This remains a proposal. Council and Parliament aim to agree a final text by early 2027, and member states are already pulling in opposite directions on the LRF. The numbers here are the opening position, not law. But the shape is set: more flexibility for industry, conditionality on free allowances, and integrity as the gatekeeper for every credit and removal that wants to count.

How Sylvera helps

For commodity producers and buyers navigating this landscape, the common thread across every change in the proposal is the same: understanding your market position, proving it independently, and knowing what it's worth across the mechanisms that apply to you.

Sylvera provides facility-level carbon intensity assessments across cement, steel, ammonia, and other commodities — built against the LCA boundaries that CBAM and EU ETS require — alongside mechanism eligibility and value assessments that map which compliance and voluntary pathways a producer qualifies for, and what the financial case looks like now and as the rules evolve.

For producers building these business cases, and for importers preparing for full CBAM exposure in 2038, that data is the foundation. Speak to our commodities team to find out more.