“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

The Market Matures: From Hype to Hard Reality

Direct Air Capture (DAC) has evolved significantly since its early hype cycles. In 2025, sky-high fundraising and overly ambitious timelines have given way to pragmatic experimentation. While 1PointFive continues to lead the pack, most DAC systems won’t reach commercial scale until 2027 or later.

But progress hasn’t stalled. Capital is still flowing, and long-term offtake agreements are in play. The spotlight has simply shifted: from commercial headlines to foundational pilot projects that stress-test technology, generate lifecycle data, and refine operations.

A recent Sylvera blog post, “Direct Air Capture Explained”, breaks down the fundamentals of DAC technology, including its purpose: to remove CO₂ directly from ambient air and store it permanently underground or in long-lived products. The blog highlights that unlike traditional carbon capture, DAC isn't tied to point-source emissions, giving it a critical role in neutralizing residual or legacy emissions.

Case Study: Climeworks

Climeworks faced criticism for emitting more CO₂ than it removed, but this critique missed the nuance. Orca and Mammoth were always designed as learning platforms. Their emissions are transparently reported in Life Cycle Assessments (LCAs)—a practice that underpins credit integrity in voluntary carbon markets. The emissions of a scaling company are not the same as the emissions of a carbon credit.

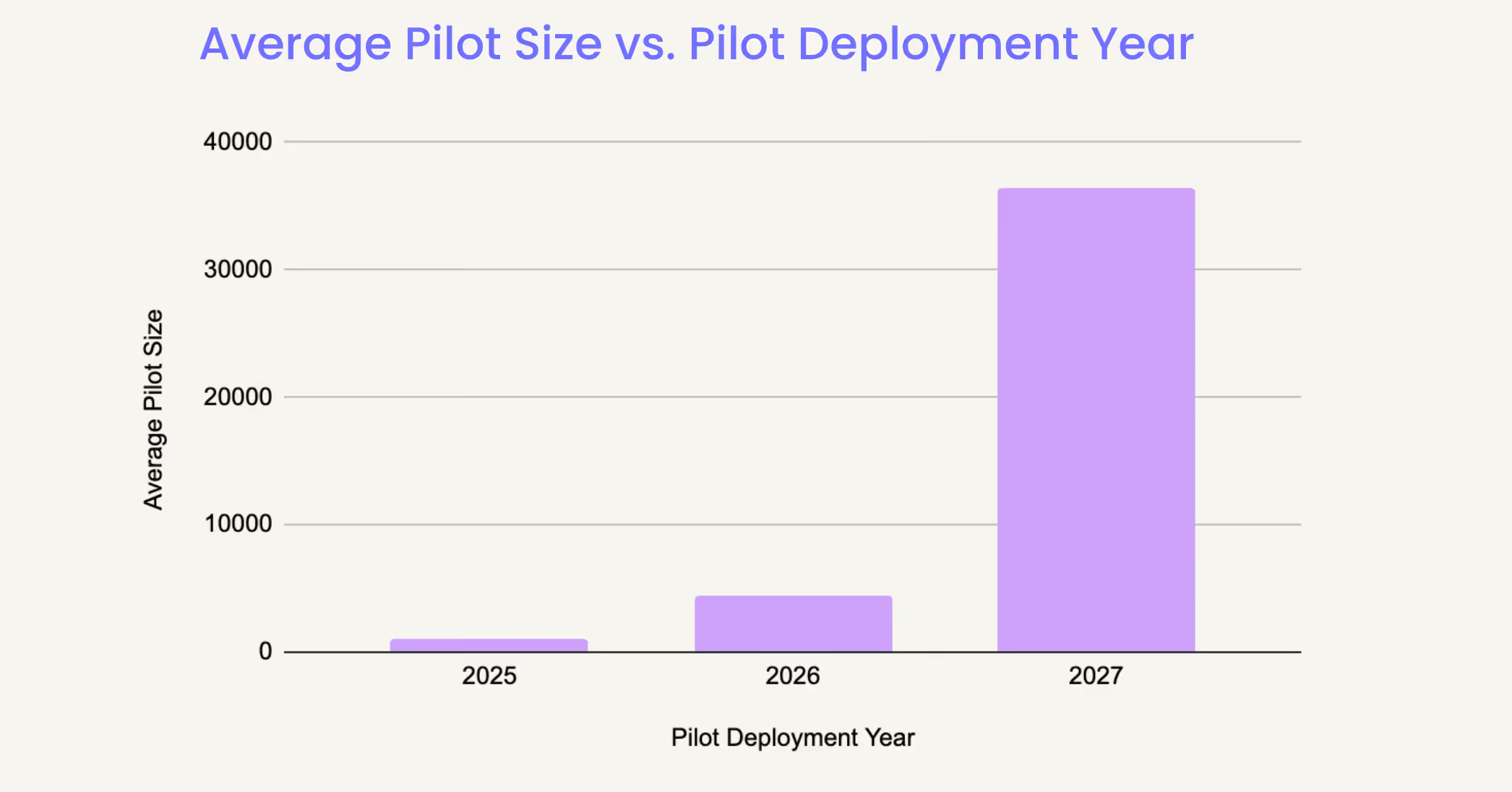

Deployment Trends: Small Pilots, Big Learnings

According to the IEA, global DAC capacity remains low—just over 10,000 tonnes per year in 2023—but over 130 new facilities are in the pipeline, signaling a dramatic scale-up trajectory. Pilot plants deployed in 2025 are typically small (hundreds to low thousands of tonnes), but average project sizes are expected to increase in 2026 and 2027. This reflects growing technical confidence and a readiness to scale responsibly.

These "super pilots" are bridging the gap between R&D and full commercialization. And critically, they generate the operational data needed to improve monitoring, reporting and verification (MRV) standards.

In Sylvera’s analysis of DAC MRV frameworks, we highlighted the importance of independently validated methodologies for quantifying CO₂ removed, energy inputs, and permanence. As carbon credit buyers become more sophisticated, MRV robustness will define which projects attract financing.

Between Policy Uncertainty and a Push for Scale

The DAC market is at a crossroads. While durable carbon removal is increasingly recognized as essential for net zero, barriers remain: high costs, energy demands, and infrastructure challenges.

In the U.S., policy support is cooling, but not frozen. States are stepping up as the federal focus wavers.

Corporate demand for durable CDR is closely tied to net-zero target-setting frameworks. In our 2025 CDR survey, 65% of respondents identified clear net-zero standards as the main factor that would increase their motivation to purchase durable removals.

A Cooling in U.S. Federal Support

The potential return of a Trump administration has triggered uncertainty. Programs like the Carbon Negative Shot and DAC Hubs are at risk. However, previously allocated funding (e.g., IIJA, 45Q tax credits) is still accessible—if developers move quickly.

Buyers and developers are hedging by concentrating in states like California, New York, and Washington, where clearer incentives and tools like LCFS remain stable.

A December 2024 article in Mongabay highlights growing scrutiny over DAC’s reliance on renewable power and permanent storage—resources that are not evenly distributed. This criticism underscores the need for more context-specific deployment strategies.

Tactical Adaptation

Developers are co-locating DAC facilities with industrial infrastructure to leverage waste heat and clean energy. The U.S. DAC ecosystem is becoming more tactical, less dependent on federal support, and more operationally grounded.

For buyers, diversification is key. Some corporations are now building DAC procurement into a broader portfolio of high-quality carbon removal, recognizing that no single approach will scale fast enough on its own.

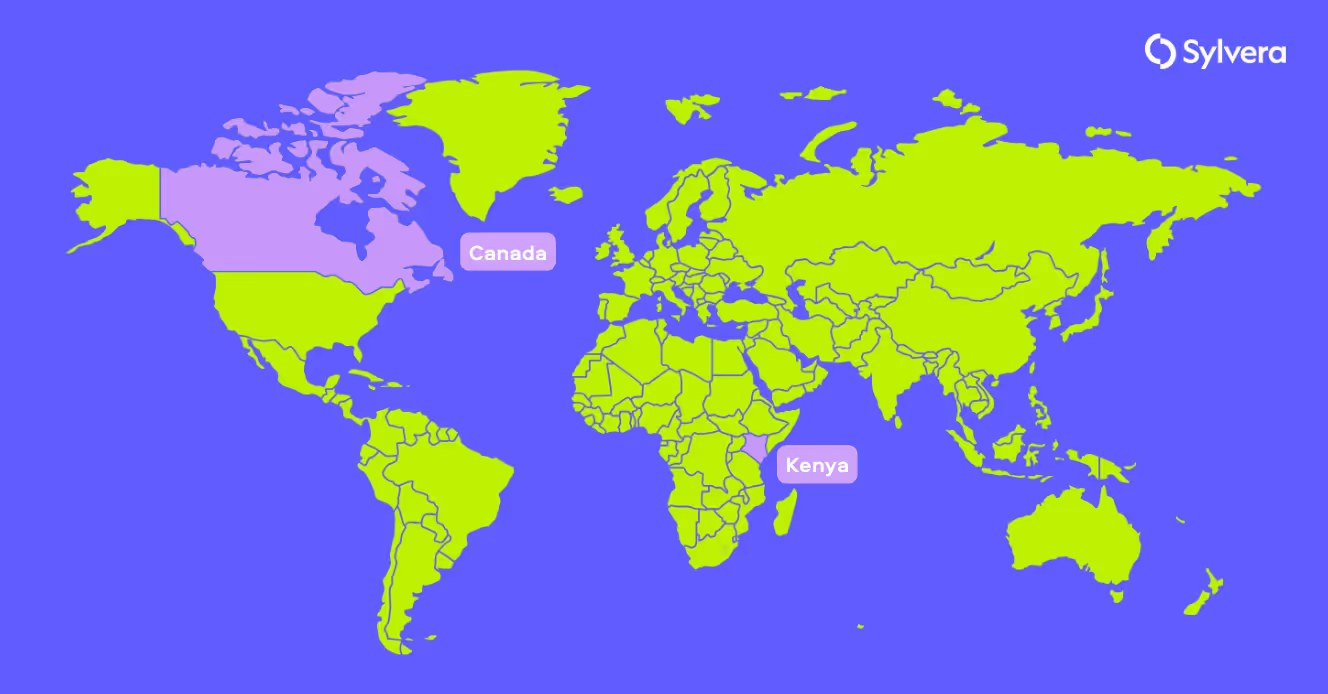

Global DAC Leaders: Canada and Kenya

Canada

- Up to 60% tax credits for DAC

- Clean hydroelectric power

- Strong geological storage

- Home to leading players like Deep Sky

Canada is positioning itself as a North American DAC leader, supported by its geology and progressive policy. The presence of low-carbon energy and permanent storage makes it a low-risk jurisdiction for developers.

Kenya

- Harnesses geothermal and solar energy

- Basalt-rich geology ideal for mineralization

- Hosts innovators like Octavia Carbon and Sirona Technologies

Kenya is leveraging its natural resources and clean energy infrastructure to test scalable, affordable DAC models. These markets also provide a testbed for Sylvera’s project evaluation frameworks in non-OECD contexts.

Chasing Scalable, Low-Cost DAC Models

DAC innovators are racing toward viable, scalable models:

- Co-products: Avnos generates clean water with CO₂ removal

- Industrial integration: Neocarbon and Capture6 embed DAC into existing facilities

- Modular design: Spiritus and Heimdal use passive airflow to cut fan-related costs

A split is emerging between:

- Technology providers (e.g., Sustaera, Mission Zero)

- Project developers (e.g., Deep Sky)

This specialization reflects a maturing value chain, as seen in 1PointFive’s acquisition of Holocene. However, scalability will hinge on delivering lower cost per tonne while maintaining credit integrity.

Read more on Sylvera’s framework for DAC project quality.

What Will Unlock Scale?

DAC remains early-stage, but its trajectory is clear. To reach climate-relevant scale, three enablers must converge:

- Stable and credible policy (federal, state, or international)

- Reliable access to clean, additional energy and geological storage

- Transparent, high-integrity MRV and LCAs

As the market matures, third-party data will become increasingly critical for risk-adjusted credit pricing, portfolio construction, and audit readiness.

Final Word: The Work of 2025 Builds the Future

Let’s not mistake slow for stagnant.

The strategic pilot projects, policy adaptations, and regional breakthroughs happening in 2025 are laying the foundation for carbon removal at scale. If you're a DAC developer, investor, or corporate buyer—this is your moment to build.

Ready to assess the quality and climate impact of your DAC project? Talk to Sylvera about our carbon credit ratings and MRV solutions.