“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

The Producer's Problem: Too Many Options, Not Enough Clarity

You've invested in decarbonization. Your processes are less carbon-intensive than many of your competitors. Now the question is: How do I drive income from this critical decision?

The monetization landscape for lower-carbon commodities is genuinely complex, and the pace of the energy transition is only adding pressure to get it right. Sylvera has mapped 21+ mechanisms for a single fertilizer producer. Said mechanisms include compliance schemes, voluntary markets, environmental attribute certificates, green premiums, and tax incentives—but each covers different commodities, operates on different rules, and calculates carbon intensity in its own way.

The last point is essential. Your carbon intensity score will change when you calculate it under CBAM, EU ETS, RFNBO standards, or LCFS. This isn't a technicality. It determines whether you're eligible for a given mechanism and how much money you can earn from it.

In addition, the financial value of each pathway changes over time. As Shona Crawford-Smith, General Manager – Carbon-Differentiated Commodities at Sylvera puts it: "Everything comes down to money. If they need to make the investment decision for decarbonizing, they need to understand—now and over time—how could I monetize this, and what's the best strategy?"

The complexity of the market prevents many producers from acting. They can't navigate the mechanisms, or they undervalue their lower-carbon product by pursuing one mechanism when a combination would yield more. Both outcomes slow decarbonization and leave money on the table.

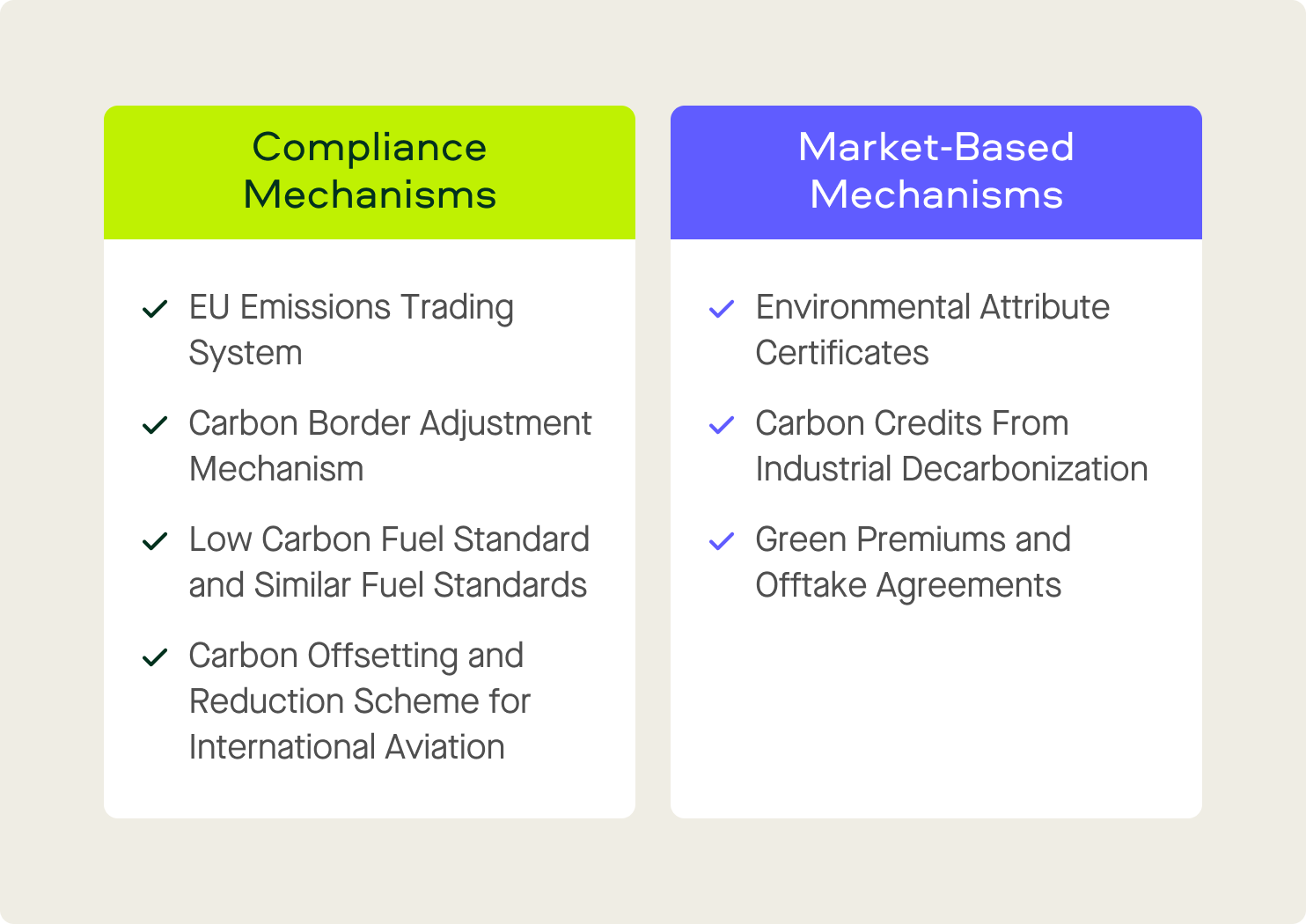

Compliance Mechanisms

Compliance mechanisms are mandatory for certain market participants. They create direct financial consequences based on carbon intensity, either as costs avoided or competitive advantages gained.

EU Emissions Trading System (EU ETS)

The EU ETS is the European Union's cap-and-trade system.

EU-based producers in covered sectors, such as cement, steel, aluminium, chemicals, power, aviation, and maritime, must hold allowances for their emissions. Lower carbon intensity equals fewer allowances, which means lower compliance costs. Switching to renewable power in the production process is one of the most direct ways to achieve this. However, there are plenty of other options, too.

The EU ETS carbon price traded between €50 and €100+ per tonne in recent years. As free allocation phases out between 2026 and 2034, the financial advantage of lower carbon intensity will grow. These savings will scale with the size of the carbon intensity reduction and the prevailing carbon price.

Carbon Border Adjustment Mechanism (CBAM)

CBAM is the EU's border carbon tariff. As such, EU importers pay for the embedded carbon in covered imports, like cement, iron and steel, aluminium, fertilisers, hydrogen, and electricity, by purchasing CBAM certificates. That cost falls on the importer, which means a lower-carbon intensity producer becomes more competitive because their products cost the importer less to bring in.

At current EU ETS prices, a cement plant that reduces embedded emissions in its supply chain by 0.5 tonnes of CO2 per tonne of product saves its EU importer roughly €25 to €50 per tonne. As free allocation disappears, that gap will widen, offering more advantages to monetization commodities.

Of note, the UK is developing its own CBAM, and other jurisdictions may follow suit.

Low Carbon Fuel Standard (LCFS) and Similar Fuel Standards

California's LCFS is the most direct mechanism for carbon intensity monetization in global markets.

Fuel producers and suppliers below the carbon intensity baseline generate tradable credits. The value is directly proportional to the CI gap, so every gram of CO₂ equivalent per megajoule of improvement adds more revenue. Similar programs exist in Oregon and British Columbia, and are emerging elsewhere.

LCFS credit prices range from roughly $50 to more than $200.

CORSIA (Carbon Offsetting and Reduction Scheme for International Aviation)

CORSIA, the International Civil Aviation Organization's global scheme, requires airlines to offset or reduce emissions above a baseline. Airlines can meet their obligations using eligible fuels like sustainable aviation fuel (SAF) or lower carbon aviation fuel (LCAF), alongside eligible carbon credits.

Since SAF carries a 2-4x premium over conventional jet fuel, LCAF has emerged as a more accessible alternative. For oil producers, including those producing crude refined from natural gas feedstocks, LCAF represents a real opportunity to capture value from lower carbon intensity crude.

Other Compliance and Tax Mechanisms

There are other compliance mechanisms to be aware of, too.

For example, the UK ETS and planned UK CBAM expand the compliance footprint for producers who export to the UK. Japan's J-Credit scheme finances lower-carbon ammonia projects, including a collaboration between Adnoc and Mitsui, and should be considered for the APAC market.

Then there's the US Inflation Reduction Act's production tax credits—45V for clean hydrogen and 45Q for carbon capture—which can be substantial. 45V offers up to $3 per kilogram for clean hydrogen.

Finally, the EU's RFNBO standards set carbon intensity thresholds that determine eligibility for EU incentives and mandates, particularly for green hydrogen and e-fuels.

Market-Based Mechanisms

Market-based mechanisms are voluntary or commercial instruments. Regulators don't require them, but they create financial value for producers who understand how to use them.

Environmental Attribute Certificates (EACs)

Environmental attribute certificates (EACs) separate the environmental benefit of lower carbon intensity from the physical commodity itself. A producer sells the commodity as a standard product, then sells the certificate to a buyer who wants to claim the lower carbon intensity in a separate transaction.

This is particularly useful for heavy commodities like green cement and low-carbon steel that can be expensive and logistically complicated to transport. For example, a lower-carbon cement producer in one region can sell their environmental advantage to a buyer on the other side of the world without physically shipping the product. Microsoft and Meta have purchased EACs for both cement and steel.

EACs are an emerging market without standardized pricing. Values depend on the carbon intensity differential, commodity type, and the buyer's willingness to pay. Early transactions suggest meaningful premiums, but the market is still developing. Time will tell what EACs are truly worth.

One important clarification: EACs for commodities are not the same as renewable energy certificates, which sometimes go by the same acronym. They are completely different.

Carbon Credits From Industrial Decarbonization

Producers who use carbon capture, hydrogen-based processes, or other decarbonization technologies can generate voluntary carbon credits for the CO2 they capture or avoid.

Methodologies exist or are currently under development for industrial CCS, fuel switching, and process efficiency improvements. High-integrity industrial credits can command significantly higher prices, especially as compliance and voluntary carbon markets continue to converge.

It's important to note that carbon credits from industrial decarbonization need the same independent assessment and quality ratings as any other credit type. Fortunately for market participants everywhere, this is Sylvera's core focus within the commodities and carbon credit production communities.

Green Premiums and Offtake Agreements

Green premiums are direct price premiums that buyers pay for lower-carbon intensity products.

Greeniums, as they're often called, can be formalized through long-term offtake agreements, like when automakers buy low-carbon steel or tech companies source lower-carbon cement.

Greeniums vary by commodity and buyer segment, though green steel premiums range from 20-40%. For some commodities, the "premium" is effectively cost parity once you factor in carbon pricing.

Some buyers want lower-carbon products but resist paying more for them. The business case often comes down to showing that once you factor in CBAM certificates and ETS compliance costs, the lower-carbon product is cost-competitive or actually cheaper for the buyer.

Crawford-Smith frames it well: "When you factor in the internal carbon pricing for a buyer or a compliance tax, the green option is winning. But not because they're charging a premium, necessarily."

The CI Calculation Problem: Why Every Mechanism Is Different

The monetization commodities landscape is complicated.

As a producer, you can't pick any mechanism and run with it, because each mechanism defines system boundaries differently. Some use well-to-gate, others cradle-to-grave, and others partial lifecycle.

In addition, each mechanism uses different emissions factors, allocation methods, and data requirements. Because of this, a single producer's carbon intensity number can look different depending on the framework they apply: CBAM, EU ETS, RFNBO, LCFS, voluntary credit methodology, etc.

The same facility can carry a materially different CI figure depending on which boundary, baseline, and allocation rules apply, and that difference determines both eligibility and financial value.

It determines eligibility and financial value. For producers who want to pursue multiple mechanisms simultaneously, they must have the resources to run separate analyses with separate data packages under each framework. This is an expensive, slow, and error-prone process.

Sylvera's CI framework is designed against each mechanism's own LCA requirements and system boundaries — including OPGEE, ICAO CEF, CARB LCFS, ECCC Fuel LCA Model, and CBAM embedded emissions rules — so a single data input produces CI scores already calibrated to each relevant regulator's data hierarchy. This removes the need for separate analyses per mechanism.

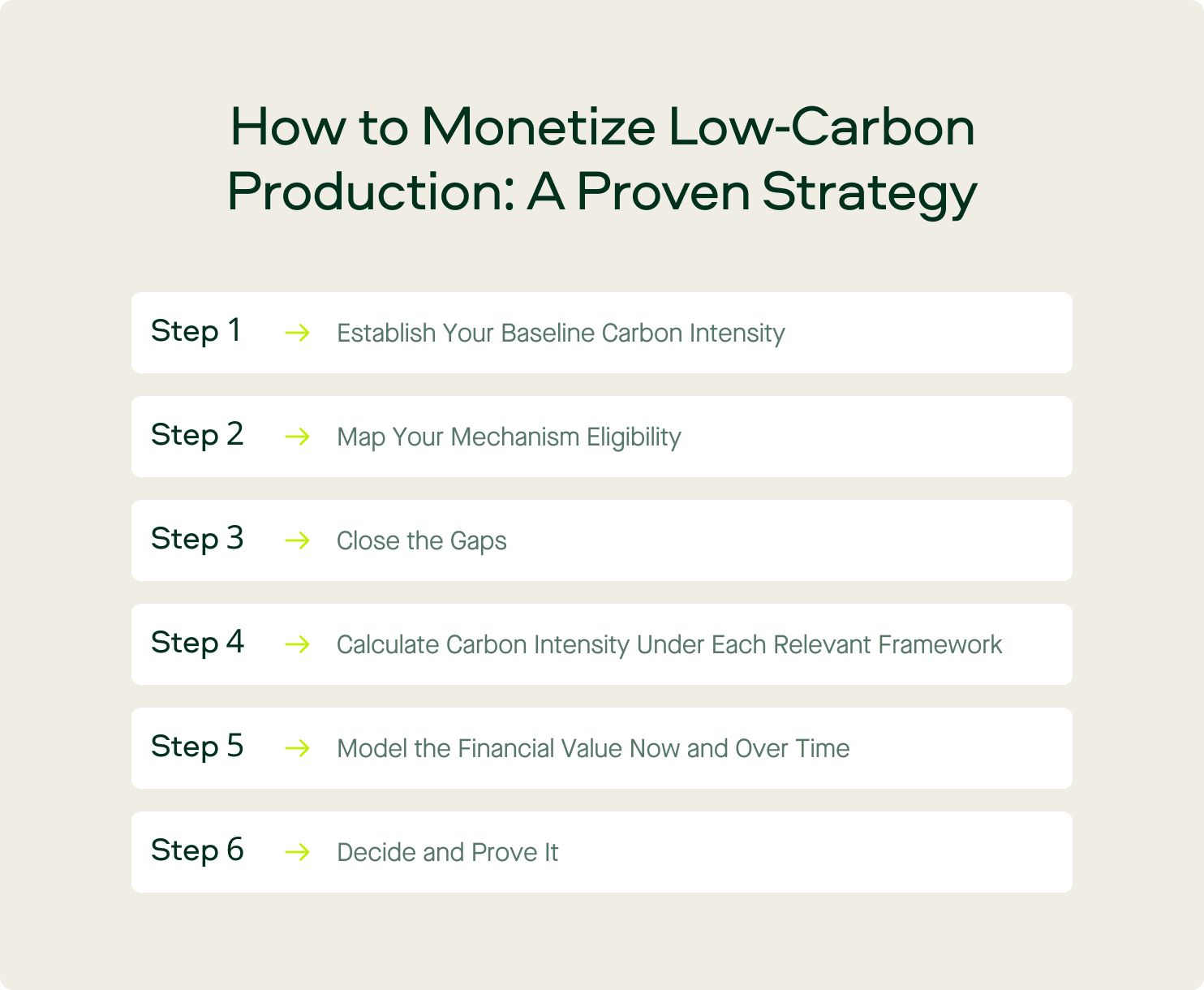

How to Monetize Low-Carbon Production: A Proven Strategy

Good news: Producers who approach the mechanism-choosing process with a structured methodology can learn what they're eligible for, what it's worth, and what moves to make.

- Step 1: Establish Your Baseline Carbon Intensity: Get an independent, facility-level carbon intensity assessment. Do NOT rely on self-reported, self-estimated assessments. You want a verified assessment that proves your quality. This is the foundation for everything that follows.

- Step 2: Map Your Mechanism Eligibility: Understand which mechanisms you're eligible for, given your commodity, geography, and carbon intensity profile. Sylvera's Mechanism Eligibility Reporting delivers a binary, rule-traceable eligibility determination for every mechanism in scope — grounded in the rule text and the data a producer can actually produce.

- Step 3: Close the Gaps: For each mechanism where eligibility isn't confirmed, Sylvera's structured gap analysis maps every failed criterion to the specific data, documentation, or operational change needed to unlock eligibility — so producers know exactly what needs to change and what it's worth to make that change.

- Step 4: Calculate Carbon Intensity Under Each Relevant Framework: Your score will look different under CBAM versus LCFS versus a voluntary credit methodology. Understand where you stand under each one. That way, you can choose the best methodology for your needs.

- Step 5: Model the Financial Value Now and Over Time: Overlay financial models to estimate what each mechanism is worth today, and how that value shifts as compliance schemes tighten and pricing dynamics evolve. The investment decision that makes sense now may not be the best strategy in three years. By taking the time to model scenarios, you'll avoid issues in the future.

- Step 6: Decide and Prove It: Select your mechanism or combination of mechanisms, then get assurance. Depending on the mechanism, that may mean independent verification from a third party like Sylvera or preparation for a verified audit from a proven entity.

Sylvera & CURA: A case study

Sylvera's work with CURA, a developer of low-carbon cement technology, shows what this looks like in practice.

After independently benchmarking CURA's production against more than 3,600 cement facilities globally - placing it in the top 0.1% of producers for carbon intensity - Sylvera mapped that performance across the full mechanism landscape: EU ETS, CBAM, EACs, and beyond.

For each eligible mechanism, we quantified the potential financial value in concrete terms. The result was a boardroom-ready commercial case that demonstrated not just that CURA's product was lower-carbon, but precisely what that carbon advantage was worth, across which mechanisms. And how that value would grow over time.

Read the full case study here.

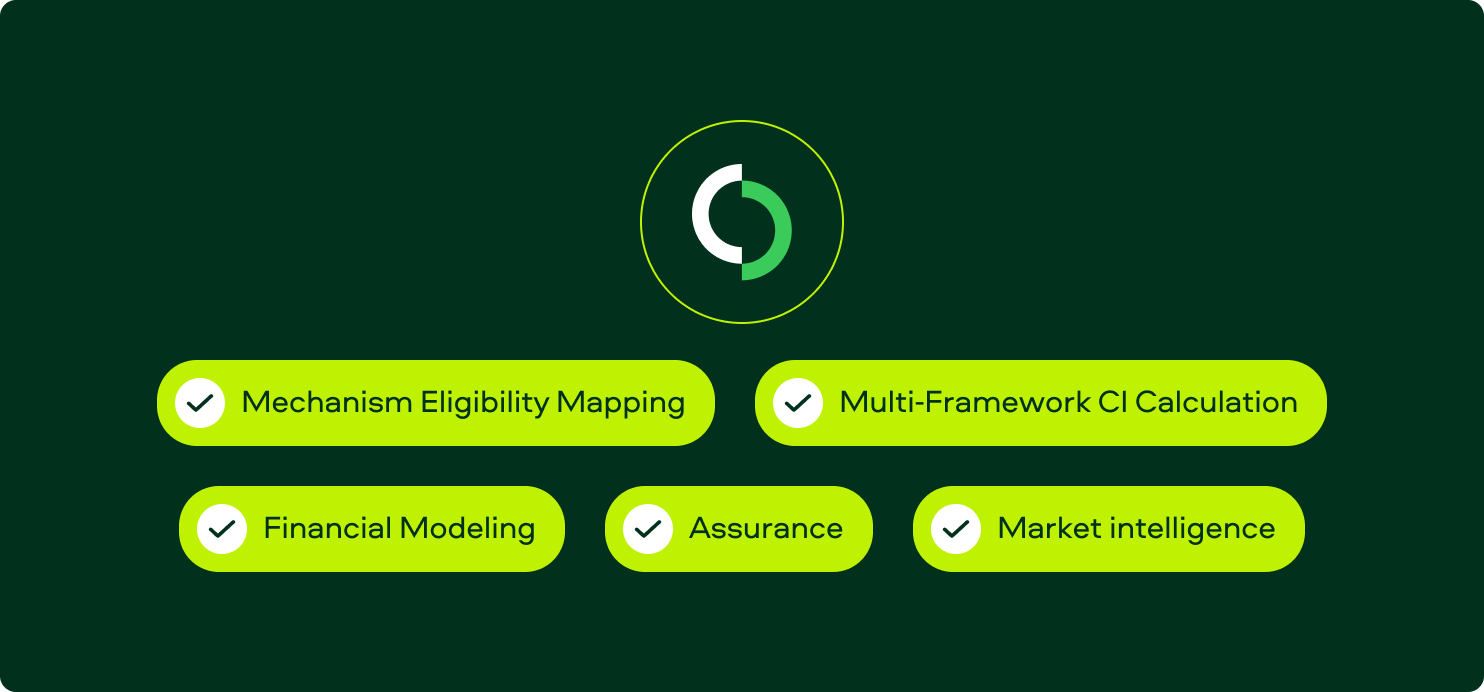

Where Sylvera Stands on Monetization in Commodities

Sylvera operates at the intersection of carbon credit markets and lower-carbon commodities.

We've spent years building assessment capabilities, data infrastructure, and market intelligence tools—all of which apply directly to the monetization problem producers face.

- Mechanism Eligibility Mapping: Sylvera maps which monetization pathways a producer qualifies for across 20+ mechanisms, identifying eligibility gaps and what it would take to close them.

- Multi-Framework CI Calculation: Sylvera calculates CI under our own standardized methodology AND mechanism-specific requirements (CBAM, EU ETS, RFNBO, LCFS, etc.) from one data input.

- Financial Modeling: Sylvera overlays pricing models to estimate monetization value per mechanism, both now and in the future, as compliance schemes evolve and profits change.

- Assurance: Sylvera provides either independent third-party verification or prepares the required mechanism-specific data package for a verified auditor.

- Market intelligence: Sylvera's Commodity Insights covers thousands of facilities, enabling producers to benchmark against peers and understand competitive positioning.

Request a demo to see how Sylvera's platform and services help producers navigate the monetization landscape, unlock the value of lower carbon intensity, and maintain competitiveness.