“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

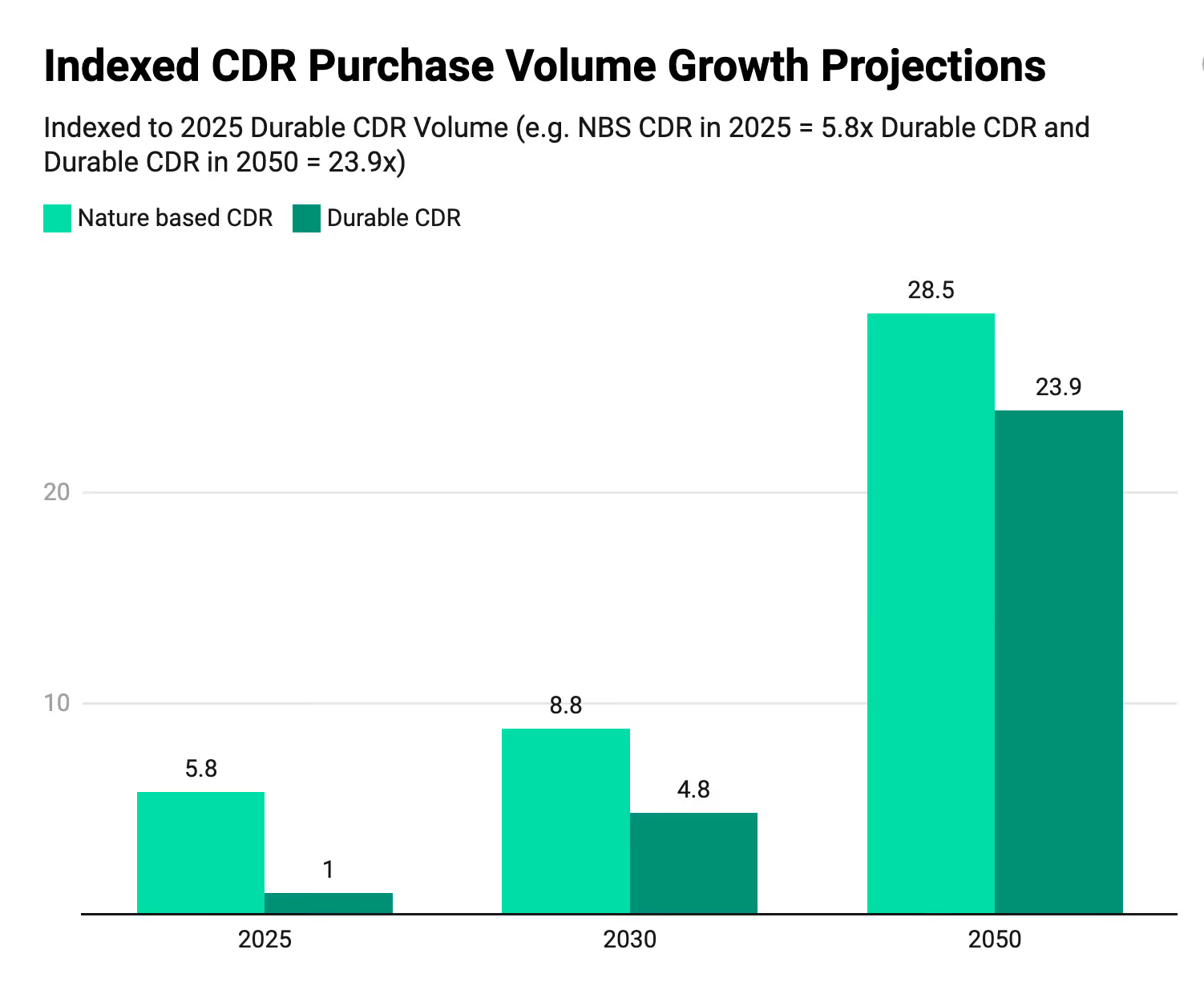

TL;DR: To scale durable CDR to the levels needed to meet corporate goals and support developer growth, action is needed. Corporate buyers need clearer standards to justify purchases; investors face a challenging landscape with 73% of suppliers yet to deliver credits; and developers must prioritize transparency and quality validation to secure financing. With nature-based solutions currently outpacing durable CDR 6:1 but projected to narrow to 1.2:1 by 2050, all stakeholders must collaborate to build the market infrastructure needed for this vital climate solution.

Earlier this year, Sylvera and CDR.fyi published our joint 2025 Market Survey, providing a comprehensive view of the durable Carbon Dioxide Removal (CDR) landscape. To dive deeper into the findings, we recently discussed the state of the market with industry experts - exploring critical challenges and opportunities in scaling durable CDR.

This discussion revealed important insights for all stakeholders - corporate buyers, investors and project developers - in the CDR ecosystem. Below, we've distilled the key takeaways for all those navigating this evolving market.

Speakers:

Robert Höglund, Co-Founder at CDR.fyi

Simon Manley, Director of CDR at Sylvera

Christopher Spry, Head of Carbon Markets at NatWest Markets

Francesco Guglielmi, Chief Marketing & Sales Manager at Exomad Green

Annalise Downey, Head of Climate Consulting at Sylvera

What impacts have recent standards had?

Our CDR market survey highlighted that 65% of respondents identified clear net-zero standards as the primary factor that would increase their motivation to purchase durable removals. During the discussion, experts unpacked why standards are so crucial to market development.

Standards provide the "why" for corporate buyers - a critical tool for internal advocacy. As one panelist noted, companies need a reason to buy carbon removal, they need someone to tell them to do it. This becomes especially important when making the case to CFOs who require clear business justification for CDR investments.

While the Science Based Targets initiative (SBTi) draft was described by some participants as disappointing and weak, in its current form, it nonetheless represents a starting point. The consultation process may see it become more inclusive of CDR requirements.

At the same time, ISO standards are now developing fully-fledged frameworks that will likely take a broader approach to CDR inclusion.

How are corporations balancing portfolios across project types?

The market survey revealed a significant gap between nature-based and durable CDR, with nature-based volumes currently outpacing durable at a 6:1 ratio. However, by 2050, this gap is projected to narrow dramatically to 1.2:1. The discussion explored how buyers are approaching portfolio construction in this evolving landscape.

Corporate representatives emphasized that no company acts in isolation - their carbon strategies connect to broader national objectives and legal requirements on climate and nature. This reality means most companies will maintain a blend of credit types in their portfolios, including both nature-based solutions and engineered removals.

The concept of emissions matching was introduced as a pragmatic approach - matching different types of emissions with corresponding removal solutions based on their characteristics, such as durability.

One of the biggest dilemmas for CDR is ‘buy now’ vs ‘wait’

With durable CDR prices expected to decrease over time, an important question emerged: why should companies purchase these credits now rather than wait?

The experts offered compelling reasons for early adoption:

- Market development: Early purchases help the industry scale, allowing suppliers to secure financing and build capacity.

- Organizational learning: Companies at the forefront of the market gain valuable experience navigating procurement processes, risk assessments, and implementation challenges—preparing them for potential future compliance requirements.

- Target achievement: Organizations with 2030 targets need to begin securing supply chains now through offtake agreements and early purchases.

- Industry Signaling: Even small purchases from diverse companies signal where the market is heading, creating confidence for suppliers and investors.

As one panelist noted, early investment "isn't a financial decision, to be honest," but rather a strategic one that positions companies advantageously for the future.

How CDR developers can overcome critical financing challenges

The market survey revealed critical financing challenges: 64% of suppliers plan to raise financing in 2025, and 85% by the end of 2026. However, 55% have not sold any credits yet, and 73% have yet to deliver a single credit. The discussion explored practical strategies for CDR startups facing this difficult landscape.

Experts emphasized that while passion and innovative technology might secure early-stage funding, securing larger capital investments requires significant de-risking. Project developers need to demonstrate:

- Expertise in their specific domain

- Clear understanding of their business fundamentals

- Operational experience with similar projects

- Realistic timelines for credit delivery

The importance of transparency and data sharing emerged as a crucial theme. One supplier noted that when they entered the market, not everything was shared transparently. So they ended up sharing as much as they could to help inform the market: video content, how they work, production data - the more data they shared, the better response they had in terms of trust from the market.

This transparency becomes particularly important during the pre-issuance stage, where uncertainty is highest and specific to each project type. Investors therefore need quality signals to guide their allocation decisions.

How are CDR developers managing registry and methodology considerations?

The discussion highlighted the complex landscape of methodologies and registries facing suppliers. With many differences in project design requirements, durability assessments, and co-benefit evaluations, navigating this environment presents significant challenges.

Experts advised developers to closely monitor emerging standards from the Core Carbon Principles (CCP) and methodologies from entities like CMCF, which are likely to become industry standards for BECCS, DACS, and Biochar.

From a supplier perspective, registry selection involves multiple considerations beyond just credit quality, including:

- Credit yield potential from the process

- Registry responsiveness and efficiency

- Cost structures

- Buyer acceptance and recognition

Key Takeaways for Corporate Buyers

- Prepare Now for Future Requirements: Even if current standards are limited, use this time to build organizational capacity, gain procurement experience, and establish relationships with suppliers.

- Adopt a Portfolio Approach: Consider complementary uses of nature-based and durable removals that match your emissions profile rather than viewing them as competing alternatives.

- Support Market Development: Early purchases, even at smaller volumes, contribute significantly to market confidence and supplier ability to scale.

- Track Evolving Standards: Stay closely engaged with developments at SBTi, ISO, and VCMI to understand how requirements may evolve and affect your climate strategy.

Key Takeaways for Investors

- Assess Technical and Business Fundamentals: Look beyond innovative technology to evaluate business expertise, local market conditions, and operational experience.

- Value Transparency: Projects that willingly share comprehensive data demonstrate confidence and decrease investment risk.

- Understand Pre-Issuance Risks: Each CDR type presents unique challenges - from proponent risk with DAC to complex LCA structures with BECCS to contract and technology risks with Biochar.

Key Takeaways for CDR Project Developers

- Reduce Friction for Buyers: Align with quality standards like ICVCM principles to simplify buyer due diligence and accelerate purchasing decisions.

- Demonstrate Long-Term Viability: Buyers investing in procurement processes need confidence in multi-year potential and sustainability.

- Focus on Cost Reduction: The next wave of buyers will be more price-sensitive; projects that can reduce costs closer to biochar pricing will have competitive advantages.

- Choose Registries Strategically: Consider not just recognition and quality standards but also efficiency, cost, and issuing potential.

Looking Ahead

The durable CDR market stands at a critical point. With the right standards framework, continued early adoption by forward-thinking buyers, and transparent, quality-focused development approaches, the industry can bridge the current gap between innovation and mainstream adoption.

And voluntary buyers are needed to bridge the gap and help sustain CDR until larger compliance markets develop. By working together across the ecosystem, stakeholders can accelerate the scaling of durable CDR, seen as a critical component of our global climate solution.

Want to learn more about the CDR market landscape? Read the 2025 CDR Market Survey report here.

How Sylvera Supports Early-Stage CDR Project Financing

As highlighted, CDR suppliers face significant financing challenges in the current market landscape. With 64% of suppliers planning to raise financing in 2025 and 85% by the end of 2026, the need for credible support mechanisms has never been greater.

Yet the survey revealed how 55% of suppliers have not yet sold any credits, 73% have yet to deliver a single credit, and more than half have raised less than $1M. This is all against a backdrop of durable CDR equity financing which dropped 30% in 2024.

Bridging the Financing Gap with Pre-Issuance Ratings

Sylvera's Pre-Issuance solution can directly address these challenges by providing early validation that builds buyer and investor confidence and accelerates project development.

For Corporate Buyers and Investors: De-Risk Early-Stage CDR Opportunities

As our webinar experts emphasized, forward-thinking companies are securing CDR supply chains now rather than waiting. For those navigating the complex CDR landscape, our Pre-Issuance Solution provides:

- Curated project discovery: Access 200+ investment opportunities spanning 15+ project types through our Early Stage Catalog, with advanced filtering for transaction terms, price, location, and issuance timelines

- Comprehensive risk assessment: Make informed decisions with our three-module Pre-Issuance Ratings covering integrity, delivery projections, and value estimations

- Ongoing performance monitoring: Track project implementation with quarterly updates and remedial action recommendations

- Direct developer engagement: Connect directly with project developers through our "Connect to Supply" feature, streamlining the sourcing process

This end-to-end solution transforms what was previously a fragmented, high-risk investment process into a streamlined, data-driven approach to CDR buying and investing.

For Project Developers: Accelerate Financing and Enhance Quality

For CDR suppliers, Sylvera's Pre-Issuance Solution for developers provides:

- Enhanced project visibility: Showcase your early-stage projects to qualified buyers and investors through our marketplace

- Credible third-party validation: Build investor confidence with our independent Pre-Issuance Ratings that validate project integrity and delivery potential

- Actionable quality guidance: Receive specific recommendations to enhance project quality and address potential risks before they impact credit issuance

- Streamlined investor engagement: Reduce due diligence timelines and accelerate financing conversations with standardized, comprehensive project assessments

This support is particularly crucial for developers of innovative CDR technologies navigating complex methodologies and technical requirements, creating transparency that substantially reduces investor uncertainty.

A Comprehensive Ecosystem of Support with Sylvera

Beyond our core Pre-Issuance offering, Sylvera platform users also gain access to a robust suite of intelligence tools to help navigate the market:

- Country Profiles: Understand regulatory landscapes and market dynamics in specific regions

- Methodology Profiles: Gain detailed evaluations of different carbon credit methodologies

- Carbon Market Data: Access up-to-date insights to navigate complex market dynamics

- Market Commentary: Stay informed on policy changes and market trends

Together, these resources create a connected ecosystem where buyers secure premium credits, investors make confident decisions, and developers accelerate financing, addressing the financing gap that currently constrains CDR market growth.

By supporting CDR developers from the earliest stages with transparent quality assessments, market insights, and remedial guidance, Sylvera is helping to unlock the financing needed to scale CDR.

Request a Demo to learn how Sylvera can support your CDR project development.

Watch the recording here

If you didn't catch the webinar, you can watch the full recording back, just head here.