“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

What Is Carbon Credit Insurance?

Carbon credit insurance is a commercial risk transfer product.

A buyer, investor, or developer pays a premium to an insurer, who agrees to compensate them if specified events occur, such as a reversal, credit invalidation, or project failure.

It works like any other insurance product: The policyholder transfers a defined risk to the insurer in exchange for a premium, and the insurer pools risk across multiple policies and projects.

It's important to distinguish carbon credits insurance from buffer pools. Buffer pools are registry-managed, collective mechanisms in which a percentage of credits from all participating projects is sent to a shared reserve. Carbon insurance is a commercial contract between an insured party and an insurer that covers complex risks for specific credits or portfolios.

The voluntary carbon market has grown from a niche mechanism into a multi-billion-dollar industry. As such, high-profile reversals, including wildfires and project failures, make credit risk more tangible, and institutional investors expect familiar risk management tools.

Plus, the growing convergence between the Paris Agreement, nationally determined contributions, and compliance frameworks like CORSIA and Article 6 raises the stakes for credit integrity. These factors contribute to the growing popularity of carbon credit insurance solutions.

What Do Carbon Credit Insurance Solutions Cover?

Carbon credit insurance products vary, but most fall into a few categories. When you know what each covers, you can evaluate whether a policy makes sense for your situation.

.png)

Reversal Risk

Reversal risk covers the loss of stored carbon due to natural catastrophes like wildfire, drought, pest outbreak, and storm. It also covers human-caused events like illegal logging, land-use change, and political instability (i.e., policy changes that impact carbon projects).

Reversal risk coverage is most relevant for nature-based solutions like REDD+, ARR, and IFM projects, where carbon storage is biologically vulnerable. If a reversal event reduces the carbon stock below a defined threshold, the insurer compensates the policyholder for the lost credit value.

Invalidation Risk

Invalidation risk covers scenarios in which credits are retroactively invalidated by a registry or regulatory body, due to methodological errors, fraud, or changes in baseline assumptions.

Invalidation risk is distinct from reversal risk: Invalidation means the credit was never valid, not that the underlying carbon was lost. As registries tighten methodology requirements and retrospective reviews increase, this risk has become more consequential for market participants.

Delivery and Performance Risk

Delivery and performance risk covers situations in which a pre-issuance offtake agreement, sometimes called a forward purchase, fails to deliver voluntary carbon credits on time.

This type of non-delivery coverage matters most to investors who commit capital to carbon project developers before they issue credits. It applies when a project underperforms, faces permitting delays, or can't complete verification on a previously agreed-upon schedule.

What Insurance Does Not Cover

Carbon credit insurance has real limitations. Clarity is important to understand what's covered.

Insurance doesn't protect against market price risk. If voluntary credit prices decline, your insurance policy won't offer relief. Most policies also exclude losses due to regulatory change.

Insurance companies don't cover reputational damage either, should your association with a failed project incur public backlash. Finally, gradual degradation, where project performance declines over time rather than through a sudden event, won't trigger a payout for most policies.

Carbon Credit Insurance vs. Buffer Pools

Carbon credit insurance and buffer pools are complementary, not interchangeable.

Carbon credit insurance is commercial, contract-based, and voluntary. Buyers pay a premium to protect specific credits or portfolios from specific risks. The advantages include tailored coverage, financial payouts, and underwriting based on project-specific data.

The limitations are cost (premiums typically range from 2-10% of credit value), coverage gaps from policy exclusions, and market immaturity with a limited track record and few providers.

Buffer pools are registry-managed, collective, and typically mandatory for nature-based projects. A percentage of credits, usually 10-20%, is reserved. If a reversal occurs, project developers cancel credits from the pool rather than reclaiming them from buyers and investors.

Unfortunately, buffer pools are often under-capitalized, cross-project risk pooling forces strong projects to subsidize weaker ones, and low-quality credits may replace buffer credits.

For projects with moderate risk profiles, standard registry-managed buffers may provide adequate protection, especially when paired with independent permanence assessments.

For large portfolios, high-value transactions, compliance-grade credits, or projects with elevated reversal risk, commercial insurance provides protection that buffer pools alone can't deliver.

When Does Carbon Credit Insurance Make Sense?

The answer depends on who you are and what you're trying to protect.

.png)

For Corporate Buyers

Insurance makes sense when credits support compliance claims, such as those under CORSIA, Article 6, or VCMI frameworks, where invalidation or reversal could create regulatory exposure.

The stakes also rise when a company's net zero goals are publicly stated and high-profile, making the reversal of already-retired credits a reputational and reporting risk.

Insurance is less necessary for exploratory purchases, small credit volumes, and credits you'll only use for contribution claims, not for neutralization.

For Investors

Insurance is relevant when you commit substantial capital before credits exist, as is common in forward purchase and pre-issuance offtake structures. Coverage for project performance failure and non-delivery protects investors who fund carbon project developers before verification.

Insurance is particularly valuable for NBS investors with long crediting periods and elevated permanence risk. It's also useful when structuring carbon credit-backed financial products, such as carbon credit funds, where fiduciary obligations demand formal risk transfer and capital relief.

For Project Developers

Carbon project developers use insurance to de-risk their projects for potential buyers.

Insured projects command higher credit prices and attract institutional capital more easily, which supports project funding and long-term growth. Insurance also protects against catastrophic loss events, such as natural catastrophes, that could wipe out years of emission reductions.

However, insurance premiums add to project costs. Developers need to weigh premium costs against the potential revenue uplift from selling insured credits.

How Insurers Assess Carbon Credit Risk

First, underwriters evaluate project type and methodology. After all, nature-based projects and engineered carbon dioxide removal face fundamentally different risk profiles.

They pay attention to geographic and climate risks as well. Examples include fire-prone regions, political violence and related risks, and climate change projections.

Insurers also look at permanence and reversal history to determine if similar projects suffered losses and what the modeled probability of future events looks like. As such, the quality of monitoring, reporting, and verification (MRV) is critical to trust the carbon emissions accounting.

Finally, underwriters assess whether existing buffer pools provide adequate protection or whether residual risk warrants additional coverage.

Independent, third-party quality assessments play a vital role in this process. The more transparent and data-rich a project's risk profile, the cheaper it is to insure. Projects with independent ratings and robust permanence assessments consistently pay lower premiums.

This is true whether the project operates in host countries with complex legal rights dynamics, developing economies, or more established markets.

The Role of Independent Data in Carbon Credit Insurance

Insurance markets can't function without reliable risk data. Traditional insurance depends on actuarial data accumulated over decades. Carbon credit insurance is new, so we haven't built a full-fledged data infrastructure. That's where independent data providers play a vital role.

Independent carbon credit ratings, permanence scores, and project-level risk assessments fill the information gap. They give insurers the comparable, standardized data they need to price policies. They give buyers information to decide if insurance is necessary. And they give carbon project developers evidence to demonstrate project quality and negotiate lower premiums.

Sylvera is the carbon data platform that underpins this process for a growing number of market participants around the world. Our permanence scores model natural risks, including fire, drought, pest, storm, and flood, using in-house climate modeling, alongside human-caused risks like project governance, community engagement, and political and socioeconomic factors.

This is precisely the data insurers need to underwrite carbon credit policies, and buyers need to evaluate if their portfolio's risk exposure warrants insurance coverage. It also provides additional quality assurance for companies navigating complex risks in the voluntary market.

Want to see how Sylvera's independent ratings and permanence assessments support risk evaluation across your carbon credit portfolio? Book a free demo today.

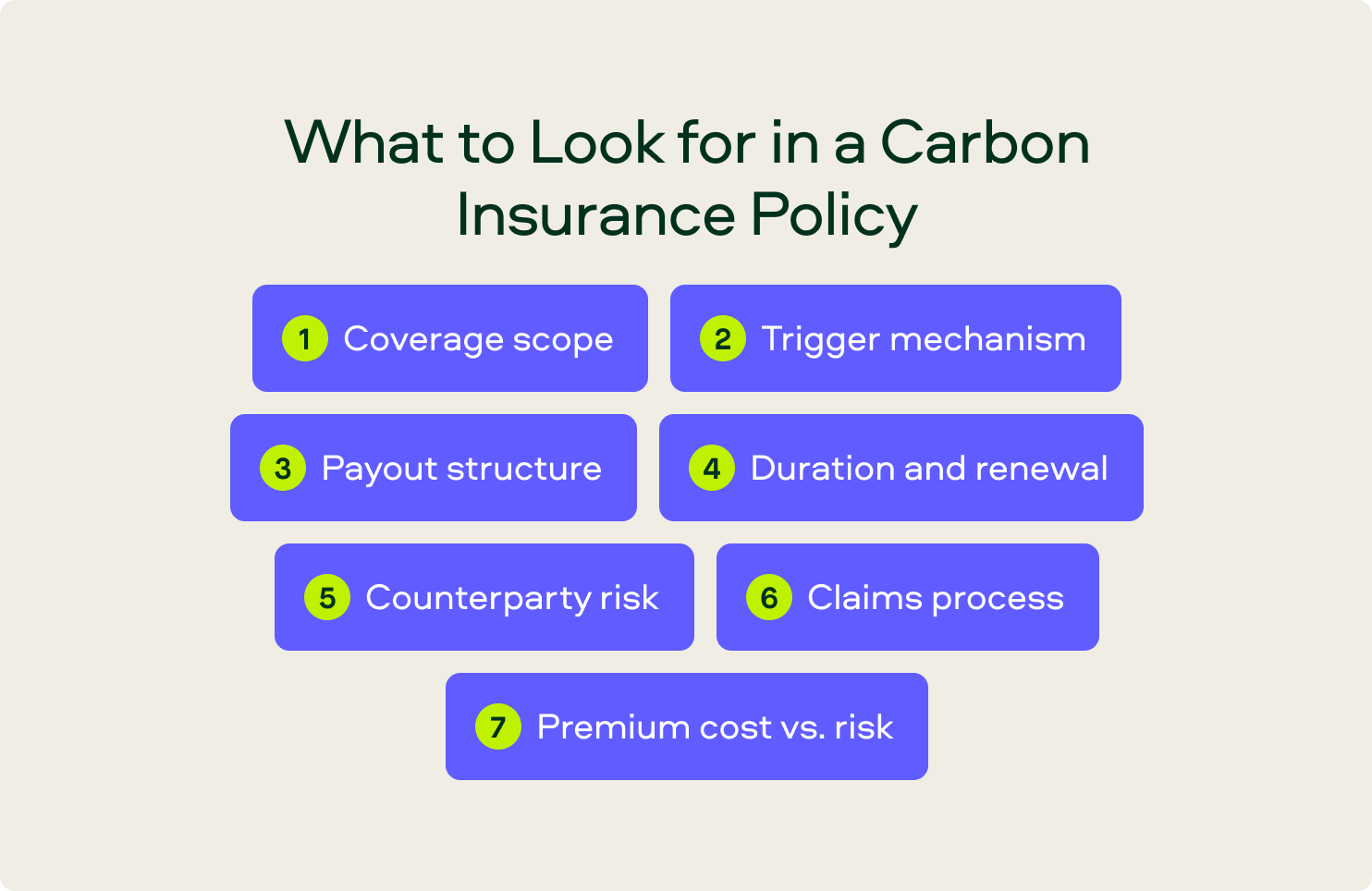

What to Look for in a Carbon Insurance Policy

If you're evaluating a policy, look for and confirm these details:

- Coverage scope: Does the policy cover reversal, invalidation, and delivery failure, or only specific events? Understand what's included and excluded before signing.

- Trigger mechanism: What constitutes a covered event? Is it triggered by a registry cancellation, a defined carbon stock loss threshold, or an independent assessment?

- Payout structure: Does the insurer pay the market value of lost credits, the purchase price, or a fixed amount? How is credit value determined at the time of loss? When it comes to carbon insurance policies, contract certainty is essential.

- Duration and renewal: Carbon projects can span 20 to 40 years. Does the insurance term reflect the crediting period? If not, consider a different policy.

- Counterparty risk: The insurer must remain financially sound for the duration of the policy. Look for rated insurers or reinsurance backing when possible.

- Claims process: How is a claim verified and paid? What evidence is required? How long does payout take? These are important factors to consider.

- Premium cost vs. risk: Use independent risk data, such as Sylvera's permanence scores, to evaluate whether the premium reflects the actual risk profile of the project.

Where Sylvera Fits In

Sylvera ratings and insurance serve different but complementary purposes.

Ratings are a pre-purchase tool. They tell you whether a credit is worth buying in the first place.

Insurance is a post-purchase tool. It protects you if something goes wrong after you've bought.

Our independent carbon credit Ratings assess project quality across additionality, permanence, and co-benefits, giving buyers the analytical foundation to make informed purchasing decisions. That same data is useful for insurers when pricing policies, and for project developers looking to evidence lower risk and negotiate better premiums.

For earlier-stage exposure, our Pre-Issuance Ratings support both investment due diligence and insurance underwriting for delivery risk — before credits have even been issued.

Better data benefits everyone in this chain. When risk is transparent and independently assessed, insurers can price more accurately, and buyers can make smarter decisions about where insurance is — and isn't — worth the premium.

Request a demo to see how Sylvera’s independent ratings and permanence assessments support risk evaluation across your carbon credit portfolio.