“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

SBTi recent context

Three years ago, SBTi was seen as a headwind facing the voluntary carbon market. Its guidance was generally unsupportive of carbon credits. As SBTi validation had become the standard of corporate climate credibility, this carried significant weight.

This contributed to a cooling of corporate demand at a time when the market needed confidence. Many companies that wanted to be seen as credible climate leaders felt they had to choose between SBTi alignment and carbon credit procurement.

The second draft of its Corporate Net-Zero Standard V2, published for public consultation in late 2025, changed this narrative. For the first time, SBTi proposed formal recognition tiers for companies that use eligible carbon credits as a component of their net-zero strategies — both in the near term and as a mandatory requirement from 2035 onwards.

The Standard introduces three optional recognition tiers under its Ongoing Emissions Responsibility (OER) framework:

- Engaged status: Mitigate at least 1% of ongoing Scope 1-3 emissions by either setting a carbon price or through eligible carbon credits.

- Advanced status: Mitigate 100% of ongoing Scope 1-2 emissions and additional Scope 3 emissions as necessary so that total coverage equals at least 10% of total ongoing Scope 1-3 emissions by either setting a carbon price of $20/ton or through eligible carbon credits.

- Leadership status: Mitigating 100% of total ongoing Scope 1-3 emissions by (1) establishing a contribution budget equal to $80/ton, (2) using the contribution budget to purchase eligible carbon credits equal to the volume of emissions covered, and (3) using any remaining contribution budget to purchase additional eligible carbon credits and/or support further eligible climate action.

Eligible carbon credits must be ex post and meet additional integrity criteria defined in the Standard. They may derive from activities that reduce emissions from emission sources outside the company's value chain; restore, protect, or enhance natural carbon sinks; and/or remove and store atmospheric carbon.

From 2035, carbon removals become mandatory for large and higher-income country mid-sized companies (Category A), with required coverage rising linearly from 1% of Scope 1–3 emissions to 100% by the net-zero target year. A distinction is drawn between long-lived and short-lived removals, with long-lived GHG emissions requiring neutralization by long-lived removals specifically.

At the net-zero target year, all residual emissions for both Category A and Category B companies — small companies from all countries and medium-sized companies from lower-income countries — must be neutralized by verified carbon removal activities within the same reporting period.

Taken together, these provisions represent a landmark elevation of carbon removal credits to a mandatory, integrity-governed pillar of corporate net-zero compliance — with significant implications for long-term demand across both the voluntary carbon market and the emerging carbon removals sector.

Where companies are and where they'd need to be

We analysed credit retirement patterns against SBTi-aligned company emissions to model what formal recognition would actually require.

The current picture

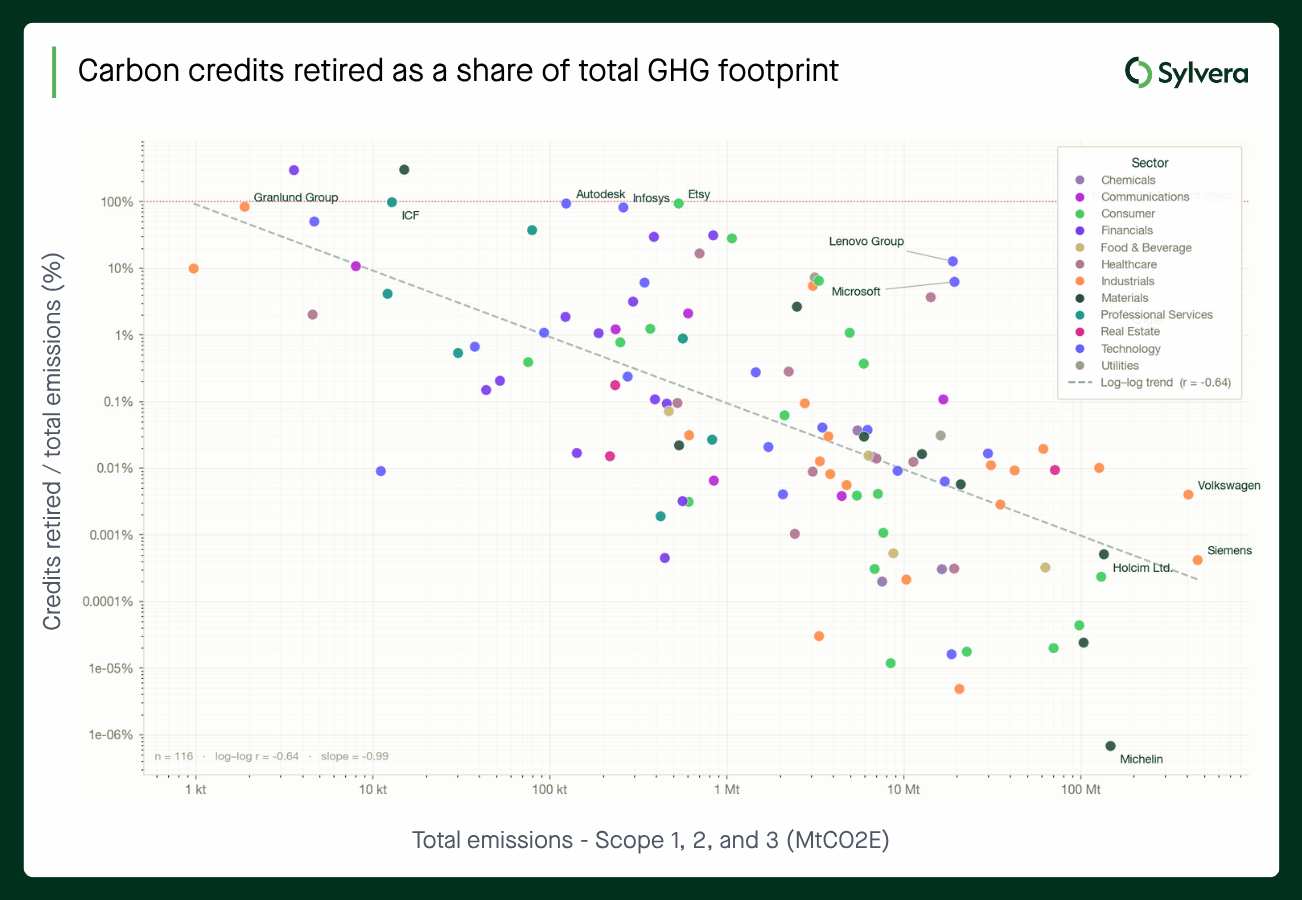

SBTi-aligned companies - roughly 11,000 globally, covering an estimated 34billion tCO₂e of total Scope 1-3 emissions - retired approximately 20 million tonnes of credits in 2026.

That's just 0.06% of their total emissions. Non-SBTi companies are even further behind, at 0.02%.

The threshold for even basic "Engaged" status under the draft framework is 1% of emissions. Companies are currently running at one-sixteenth of that level.

The current picture:

For example, as shown in the scatter plot chart above, across 116 SBTi signatories with CDP-reported data, almost no company is currently offsetting at the level the standard would require. A small number of lighter emitters offset a significant share of their footprint, but the pattern in the bottom-right of the chart shows how the heaviest emitters are offsetting the least, many at less than 0.01% of total Scope 1, 2, and 3 emissions.

What the numbers look like if companies respond

We modelled three scenarios for how the market might respond to formal SBTi recognition, assuming SBTi-covered corporate emissions remain stable.

Scenarios for SBTi companies:

*Quantified in terms of percentage of SBTi-company emissions (scope 1, 2, 3) falling under companies aligned with leadership and recognition status respectively

Resulting total credit demand from SBTi-aligned companies*:

*Assuming SBTi-covered emissions remain stable through 2030-35, potentially if the rate of emissions reductions are matched against the rate of increased SBTi participation.

To put this in context, if carbon credit demand is 20 million tonnes annually (from SBTi companies) - even a moderate adoption scenario (Scenario A) would see an almost 170% increase in SBTi-driven carbon credit demand by 2030. A more bullish scenario sees demand approaching 1.1 billion tonnes by 2035.

The Leadership tier is a different challenge entirely. At 100% offset of total Scope 1-3 emissions, the bar is extremely high. Our analysis suggests virtually no current SBTi-aligned companies would qualify. Even the Advanced level will stretch most buyers significantly.

What to watch

The numbers above show just how large the gap is between where companies currently stand and where they'll need to be. Closing it will require credible supply, quality signals the market can trust, and buyers willing to move.

We'll publish further analysis of SBTi CNZ V2.0 and what it means for the market shortly.